Android 4.3 might boost battery life as much as 500 percent, if results experienced by tester Joe Levi are repeatable.

"On Android 4.2 I can typically expect four to six hours of use before I need to recharge," Levi says. "On Android 4.3, without changing my usage habits, I was surprised to see the phone last all day, all evening, and still had charge enough to get me to work the next morning. I was able to eek out 25 hours."

Wednesday, July 24, 2013

Android 4.3 Apparently Will Dramatically Boost Battery Life 500%

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Europe Telco Revenue Decline is Momentarily Unstoppable

Global telecom revenue growth has been slowing for some time, in most markets other than emerging countries, it is safe to say.

It also is safe to say the worst-hit region globally is Europe, where service providers with significant exposure to Europe reported worse results in 2012 than they did in 2011, according to Ovum analyst Adaora Okeleke.

In fact, “the primary goal of Europe’s telcos is to stabilize their performance,” said Steven Hartley, Ovum telco strategy analyst. As is the case for other service providers facing maturing legacy revenue streams, European service providers face the challenge of growing new revenues in emerging markets faster than revenues decline in their core European markets.

And the problem there is that average revenue per user will be lower in the new markets. So European carriers are losing high gross revenue and higher margin customers while trying to gain lower gross revenue, lower margin customers.

“The overall revenues of European telcos were substantially lower, and growth in their emerging market operations was not enough to offset the losses in their domestic markets,” says Okeleke.

Even efforts to gain greater scale could backfire, though. European regulators and service provider executives also favor consolidation in Europe as one way of boosting performance. That’s logical.

Telecom is a scale business, so additional scale should help. The emphasis, Ovum might say, has to be placed on the word “should.”

Scale strongly correlates with net debt, number of employees, revenues, capital employed, and EBITDA, says Emeka Obiodu, Ovum principal analyst. That’s just another way of saying that bigger operators are larger, quantitatively, on every financial or operating dimension other than profit margin, return on capital or earnings per share, for example.

But that’s the problem. Ovum analysis suggests scale is not directly correlated to better financial performance on the profit margin, return on capital, earnings per share or

net debt as a percentage of EBITDA.

Ovum forecasts that telco revenue growth will slow to a compound annual growth rate of two percent between 2012 and 2018. Most of the actual growth will happen in emerging markets, while revenue is likely to stay stuck in a declining mode in Europe.

The growth that does occur will largely come from emerging markets, with China playing a major role, Ovum says. Mobile services, and especially mobile data, are key as well.

Telcos in the Asia-Pacific region and emerging markets experienced some growth but at a slower rate than in 2011, Ovum says. The exceptions were China Telecom and China Mobile, which both reported significant revenue uplifts in 2012.

Service providers in Japan, North America, and South Korea also fared better than their counterparts in Europe, though the revenue growth rates are expected to slow until at least 2018.

The conventional wisdom for most telcos is that they must develop new revenues while becoming much more operationally lean. It’s hard to disagree. But it also is hard to envision that telcos can do what some suggest, namely becoming as efficient as application providers.

“Telcos could feasibly play a role as service enablers, but they first need to adopt the leaner structures of over-the-top players such as Google.” says Okeleke.

One might say that is virtually impossible. A more reasonable goal would be to operate a high-bandwidth access network as efficiently as a cable operator does.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, July 23, 2013

Government Policy Uncertainty Slows China Cable Industry

Public communications businesses, whether of the mobile, fixed network telco, cable TV, satellite, fixed wireless or Wi-Fi and TV white spaces varieties, always require the approval, and sometimes the support, of government regulators and legislators.

Public communications businesses, whether of the mobile, fixed network telco, cable TV, satellite, fixed wireless or Wi-Fi and TV white spaces varieties, always require the approval, and sometimes the support, of government regulators and legislators.

The reason is the need for spectrum, rights of way and a legal framework to enable those businesses.

“The biggest challenge facing cable operators in China has nothing to do with technology or competition. Instead, it’s politics that will make or break Ethernet over Coax rollouts,” says Jeff Heynen, principal analyst for broadband access and pay TV at Infonetics Research.

“After last year’s turnover among Communist Party leadership, as well as in key positions within SARFT, the emphasis on China’s NGB (next-generation broadband) network project has been called into question, and it’s adversely impacting infrastructure build-outs and subscriber additions,” Heynen says.

Despite aggressive pricing and service bundling, Chinese cable operators are having a difficult time adding new subscribers, Infonetics Research says.

As of June 2013, nearly 25 million homes had been passed with EoC services, with only 4.9 million subscribers, a take rate of less than 20 percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Broadband Strategy Has Worked for AT&T, Verizon

For more than a decade, one big question about new service efforts conducted by telcos has been the basic issue of whether revenues from new services would be earned at magnitudes big enough to offset losses in the legacy voice business.

For more than a decade, one big question about new service efforts conducted by telcos has been the basic issue of whether revenues from new services would be earned at magnitudes big enough to offset losses in the legacy voice business.

You might argue results have been mixed. AT&T and Verizon have made the strategy work, shifting revenue generation in the fixed network business to broadband services, at least in the consumer lines of business

Overall, both AT&T and Verizon have been powerfully assisted by the advantage of growth driven by mobile services. But that should not distract from the important fact that both have replaced lost fixed network revenues with new sources.

Smaller providers, unable to leverage the benefits of scale that seem essential for video entertainment services, arguably have not been so lucky.

In large part, the AT&T and Verizon successes have been driven by market share shifts.

For some time, cable TV providers and telcos have been trading market share; cable ceding video customers to telcos while telcos shed voice customers to cable operators. Both industries have relied upon those market share gains to offset legacy product revenue declines.

In the high-speed access market, telcos mostly have been losing the market share battle to cable. On the other hand, high speed access is a key part of the broadband services revenue story.

U-verse revenue growth contributed to a two percent year-over-year increase in

AT&T’s consumer wireline revenues during the first quarter of 2013. Consumer U-verse revenues grew 30.8 percent over 2012 and now represent 48 percent of wireline consumer revenues.

Verizon’s consumer wireline revenue growth of 4.3 percent was driven by FiOS revenues, which grew 15 percent in the first quarter of 2013 and generated 69 percent of consumer revenues.

The importance of video revenues can be contrasted with first quarter results at CenturyLink, which has not in the past provided video entertainment services across its legacy Qwest Communications network footprint.

CenturyLink reported a 3.4 percent year-over-year revenue decline for its Consumer Group during the first quarter.

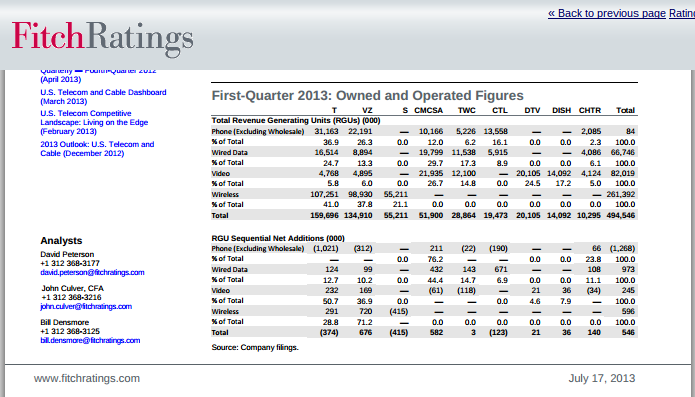

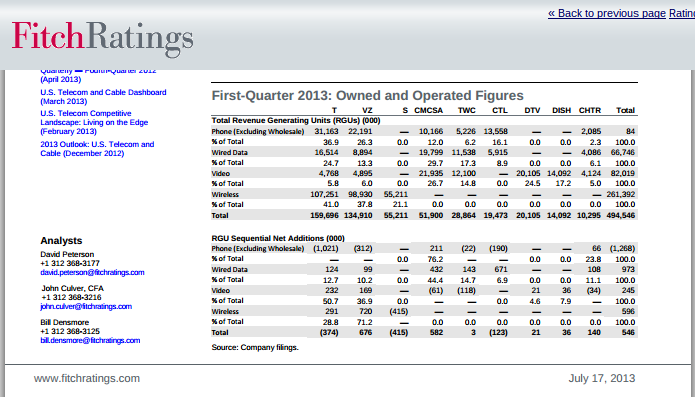

Those broadband revenues, especially television revenues, will continue to be important, as U.S. telcos lost 0.966 million wireline voice connections during the first quarter of 2012, compared to a net loss of 1.105 million for the same quarter of 2012.

Verizon’s residential voice connections declined by 5.6 percent on a year-over-year basis, while AT&T’s consumer voice connections dropped 12.5 percent. CenturyLInk’s overall access line loss was 5.7 percent.

And though telcos generally lag cable in net new high speed account gains, the largest telcos collectively added 290,000 broadband customers during the first quarter, about 98 percent of their same quarter 2012 net additions.

AT&T and Verizon continue to take video-service subscriber share from the cable companies. AT&T video service penetration now is 19.4 percent of eligible homes, while Verizon video penetration is 34.1 percent of eligible homes.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

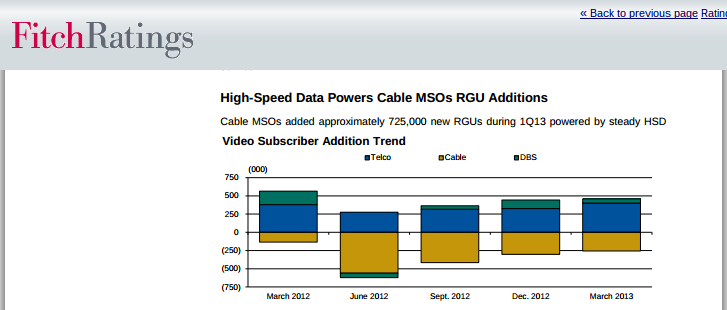

Operating Results "Stable" for Leading U.S. Telcos, Cable

Despite all the challenges, ranging from mature markets to limited sources of new revenue to heightened competitive pressure, U.S. telecom and cable companies still are expected by Fitch Ratings to turn in stable operating results that are resilient to changes in the economy.

But Fitch also believes the service providers have a bit of wind in their sails, as Improvements in economic conditions, particularly stronger employment and housing trends, will lead to a healthier overall operating environment.

That stability is perhaps surprising given recent trends. Overall, wireless net additions among the three largest mobile service providers dropped 77 percent to 596,000 units during first-quarter 2013, year over year.

To the extent there were gains, Fitch Ratings points to tablet accounts as the driver, creating a more stable and predictable revenue stream for mobile operators. But subscriber gains are not seen as the way mobile service providers will make revenue gains. Instead, it is more spending on usage plans that will be key.

Big slowdowns also occurred in the video services segment. Fitch estimates that the largest video service providers gained 201,000 net video subscribers in the first quarter of 2013, representing a 53 percent decline year over year.

The slower growth reflects the high penetration of video subscription households in the U.S., the mature video service product, tepid economic and housing recovery and, to a lesser extent, competition from alternative distribution platforms.

Fitch points out that the largest incumbent local exchange carriers “continue to transform their consumer businesses into broadband- and video-focused models.” In fact, at Verizon and AT&T, those gains are “sufficiently mitigating the ongoing secular and competitive pressures of their respective consumer landline businesses.”

That is not so much the case for much-smaller telcos, as video entertainment is a scale business. Under those conditions, lack of scale also means lack of margins.

Such prospects are one reason the AT&T Project Velocity IP initiative will extend IP-based wireline broadband service to approximately 57 million customer locations (both consumer and small business) representing 75 percent of the customer locations within the company’s 22-state service area by year-end 2015.

In the remaining 25 percent of customer locations where it will not be economically feasible to upgrade the wireline network to faster broadband speeds, the company will offer a 4G Long Term Evolution solution instead.

AT&T intends to expand its U-verse platform to a potential market of 33 million

customer locations as part of the initiative, adding 8.5 million customer locations to the 24.5 million locations already able to buy U-verse service.

About 90 percent of U-verse customers will have the capability to receive speeds up to 75 Mbps and 75 percent will be able to buy 100 Mbps service.

In other cases, where AT&T has concluded it cannot afford to build full U-verse connections, and DSL has to be used (about 24 million locations), speeds up to 45 Mbps will be available to 80 percent of DSL-served locations, while half will be able to receive 75 Mbps service.

AT&T estimates that 75 percent of its U-verse TV subscribers have triple- or quad-play service with the company, pointing out the strong reliance on video and broadband services in driving AT&T revenues. U-verse triple-play subscribers generate $170 of average revenue per user a month.

Verizon likewise reports that 66 percent of its FiOS subscriber base buy a triple play package and generate $150 a month ARPU. The need for broadband and video revenues is obvious.

In aggregate the ILECs lost approximately 0.966 million wireline voice connections during the first quarter of 2012, compared to a net loss of 1.105 million for the same quarter of 2012.

Verizon’s residential voice connections declined by 5.6 percent on a year-over-year basis, while AT&T’s consumer voice connections dropped 12.5 percent. CenturyLInk’s overall access line loss was 5.7 percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

LTE is Going to be a Fixed Network Alternative

You always can get an argument about whether broadband Internet access provided by Long Term Evolution networks is a reasonable substitute for fixed network high speed access. But it already seems clear that the substitution of LTE for fixed network fiber access is going to become a reality for quite a substantial number of potential customers.

AT&T's Project Velocity will extend IP-based wireline broadband service to approximately 57 million customer locations (both consumer and small business) representing 75 percent of the customer locations within the company’s 22-state service area by year-end 2015.

In the remaining 25 percent of customer locations where it will not be economically feasible to upgrade the wireline network to faster broadband speeds, the company will offer a 4G Long Term Evolution solution instead.

That is one way of saying that up to 25 percent of households located within AT&T's fixed network footprint ultimately will only be able to buy LTE for higher-speed access, and will not have access to a hybrid fiber-copper network.

As always, different network solutions make sense in higher-density areas, such as cities and suburbs, compared to what is feasible in rural areas. One size never fits all. That mixed network approach virtually assures that LTE will be used as a substitute for fixed network high speed access.

The debate is over, for practical purposes. In at least some cases, LTE will be a functional substitute for fixed network access.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Growth, not Liquidity is Issue for U.S. Telcos, Cable

A review of U.S. cable and telco firms suggests liquidity is not a problem for most, according to Fitch Ratings. But mature markets, limited opportunities for revenue growth and heightened competition are issues.

In the first quarter of 2013, liquidity in both telecom and cable TV segments overall remained strong, with 89 percent of committed facilities available for borrowing and total liquidity exceeding aggregate 2013, 2014 and 2015 maturities, Fitch Ratings said.

In other words, most of the firms have sufficient cash to operate their businesses. But the report also points out the key concerns contestants face.

For AT&T, the concerns are competitive pressures, particularly associated with switched access lines. Also, the weak economy is affecting business revenues. AT&T also faces long-term spectrum requirements, which will cause it to spend money to catch up. Meanwhile, AT&T also is stepping up its spending on share repurchases.

At Comcast, limited revenue growth opportunities outside of its core triple-play service offering and its aggressive policy of returning capital to shareholders are seen as issues.

At DirecTV, an aggressive policy of returning capital to shareholders and lack of revenue diversity, plus a narrow product offering are issues. As with the cable providers, a mature U.S. video entertainment business also is an issue.

Time Warner Cable faces a weak economy and competitive pressure negatively affecting its free cash flow margin, subscriber growth and revenue. Financial leverage is another issue.

For CenturyLink, the issue is limited ability to drive new revenue growth.

At Charter Communications, elevated financial leverage is an issue, especially if Charter succeeds with its plans to grow by acquisition. Also, Charter has relatively weaker service penetration than most of its peers. Competition is an issue, as it new revenue growth outside of its core triple-play offerings.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...