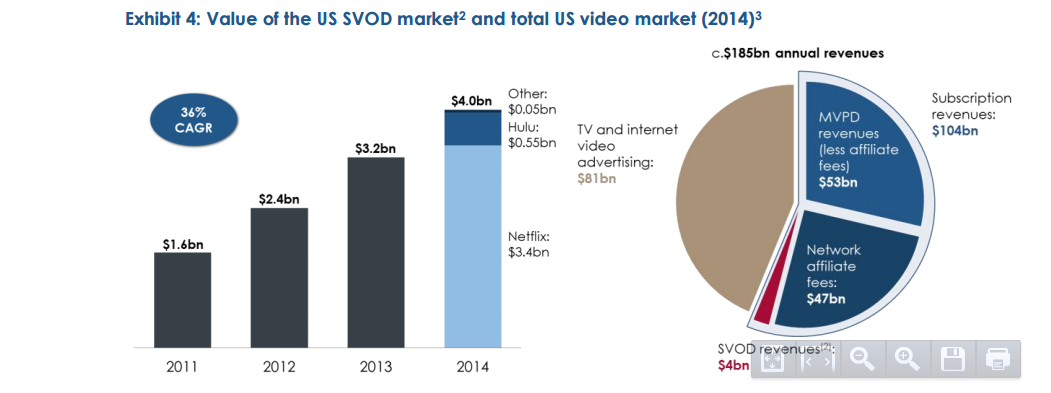

Premium over the top subscription video revenues are expected to grow from $4 billion in 2014 to between $8 billion 12 billion in 2018, a group of 45 industry entertainment industry and distributors believe.

But the eventual market is the $104 billion now spent on linear video subscriptions. But there are many uncertainties. It is unclear whether the new OTT market presents a revenue opportunity bigger, smaller or equivalent to today’s linear business.

Some would say history suggests the future market might be smaller than today’s market, while others would say logic suggests a market roughly as big as the current linear market. A few might argue for a much-bigger market over time, but that is likely the minority view.

Most likely would be happy with a near term outcome where OTT gains and linear losses result in a market that is the same size, in terms of end user buying.

The scenario where the market grows quite substantially relies on value creation and consumer perception. Since consumer budgets are limited, spending for new products tends to cannibalize current spending on other products.

So fixed network voice tends to shrink as consumers shift spending to mobile substitutes. In that instance, however, the overall market grows, in part because services “to a place” are replaced by “services for people.”

The pressure in entertainment video is that many consumers view current spending on linear products as “too high,” so OTT appeals because it costs less. Almost by definition, that tends to shrink the market, as mass adoption happens.

Netflix is expected to remain the largest single mass-market OTT provider in the United States, although participants expect its share to decline from 85 percent of the market in 2014 to around 50 percent in 2018 as other providers gain traction.

The report findings are contained in Prospects for Premium OTT in the USA and suggest executive belief that the future leaders will be found among today’s providers, though many niche providers also could flourish.

Industry participants envisage 15 to 20 specialist OTT providers acquiring 100,000 or more paying subscribers by 2018.

Opportunities for new mass-market OTT providers to challenge Netflix, Hulu and Amazon are likely limited to the leading linear video distributors Apple, Google and Facebook.

The reason is the assumed advantages of access to established subscriber bases, along with strong market share positions in an existing market (linear TV) that is expected to fuse with the emerging OTT subscription market.

In other words, if OTT is the substitute new product for linear, then linear providers are well positioned to supply OTT products as well, and have ample incentives to do so.

At the same time, OTT content providers have ample incentives to partner with big distributors to gain immediate volume, while gaining a less-expensive way to promote and bill for services. Few, if any, OTT content providers are set up to support retail billing and customer support, for example.

Industry executives believe that the underlying enablers for premium OTT services (broadband, connected devices, and payment infrastructure) are largely in place and are sufficient to support rapid growth in the next few years.

Greater availability of public WiFi, increased penetration of tablets, connected TVs and streaming media players, improved device interoperability, and standardization between heterogeneous client platforms would boost adoption.

The survey was sponsored by Vindicia and Ooyala, and conducted by MTM between May and June 2015.