Experts talk about evaluating IoT business cases, including deployment cost.

Sunday, April 2, 2017

IoT Deployment Costs and Business Cases

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Low Power Networks for IoT

Hardy Schmidbauer, CEO and co-founder of TrackNet talks about LoRaWAN deployment models and IoT monetization.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

FCC to Consider Special Access (Business Data Services) in April 2017

Among items the Federal Communications Commission will start to address at its April meeting is a potential change of course on special access (business data) regulations. The FCC is expected to begin a process of deregulating (removing price controls) in areas with competition, while maintaining price controls where there is not competition.

In all likelihood, that will mean price regulation is removed in urban areas, but often retained in rural markets. The big new change, after several decades of competition, is the emergence of cable TV companies as the primary new suppliers in markets dominated in the past by telcos.

The last FCC chairman and commission favored more regulation of special access services, though no action was taken, as the change of presidential administration also clearly meant leadership of the FCC would change.

But the FCC had seemingly been on course to institute lower prices for millions of small businesses, schools, and libraries, with an 11 percent reduction in prices phased in over three years. Critics argued the new price caps would further diminish investment, as demand already is moving away from special access and towards Ethernet access alternatives.

In principle, what is at stake is the proper regulatory stance for an important legacy service that nevertheless is in a declining state, with lots of competition in many--if not virtually all--larger markets. In fact, executives of independent business data service providers have noted for some years the fact that cable TV operators have taken leadership of the special access market away from independent providers who used to compete with the legacy telcos (primarily AT&T, CenturyLink and Verizon).

The new chairman now says he favors relaxing pricing rules where there is competition in the market. Controversy about special access markets has been a staple of the U.S. regulatory environment for decades.

The FCC has been studying the business data services (special access, primarily T1 and DS3) market for more than a decade. “The extensive record compiled by the Commission's excellent staff shows substantial and growing competition in many areas of the country, thanks to new market entrants like cable companies,” said FCC Chairman Ajit Pai. “Where this competition exists, we will relax unnecessary regulation, thereby creating greater incentives for the private sector to invest in next-generation networks. But where competition is still lacking, we'll preserve regulations necessary to prevent anti-competitive price increases.”

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

IoT Use Cases for 5G Networks

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, April 1, 2017

Investment or Competition: "Choose One"

Almost every important regulatory decision in the telecommunications industry is directly related to investment and competition, as regulators and policymakers, in principle, want more of both. The big problem always is that those goals often are mutually exclusive. In the short term, it always is possible to boost consumer welfare by policies that promote competition, using policies such as mandatory wholesale and mandatory healthy price discounts for such services.

In the longer term, those same policies tend to depress facilities investment, as profits are not attractive. The problem arguably is worse for legacy services in clear decline, as no amount of investment changes the demand curve for products consumers are abandoning.

So virtually every strategic decision made by every larger access provider these days relates to harvesting of legacy revenues and development of replacement revenues. That is especially true for legacy mobile and fixed service providers, as attackers often can add revenue simply by taking market share from incumbents, even if markets are mature.

For more than a decade, U.S. policymakers have debated whether price controls need to be maintained for special access (T1, DS3) sold to enterprises. Among the issues other than presence or absence of competition in such markets is the fact that demand is shifting away from special access and towards Ethernet replacement services, even as prices for such special access services have dropped substantially over the past few decades.

Among items the Federal Communications Commission will start to address at its April 2017 meeting is a potential change of course on special access (business data) regulations.

The last FCC chairman and commission favored more regulation of special access services, though no action was taken, as the change of presidential administration also clearly meant leadership of the FCC would change.

But the FCC had seemingly been on course to institute lower prices for millions of small businesses, schools, and libraries, with an 11 percent reduction in prices phased in over three years. Critics argued the new price caps would further diminish investment, as demand already is moving away from special access and towards Ethernet access alternatives.

In principle, what is at stake is the proper regulatory stance for an important legacy service that nevertheless is in a declining state, with lots of competition in many--if not virtually all--larger markets.

In fact, executives of independent business data service providers have noted for some years the fact that cable TV operators have taken leadership of the special access market away from independent providers who used to compete with the legacy telcos (primarily AT&T, CenturyLink and Verizon).

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Telecom is Mature; Is it Declining?

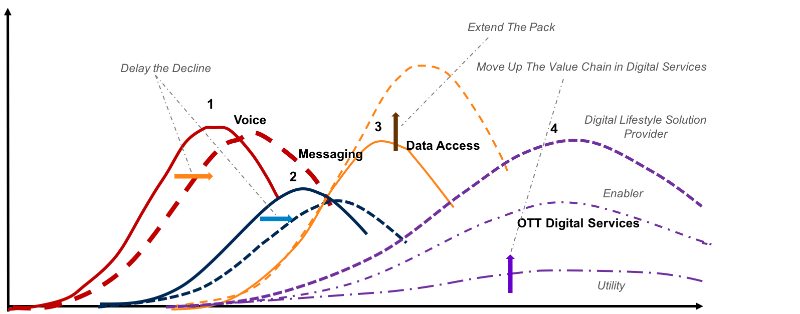

Every legacy retail access service supplied by cable TV and “telco” providers in most developed markets arguably has passed its product cycle “peak.”

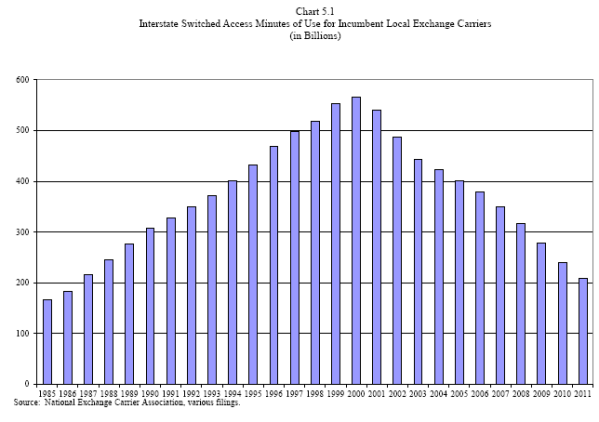

U.S. voice lines peaked in 2000 or 2001, for example, as did long distance minutes of use. Text messaging revenues also are falling. Fixed network internet access markets are reaching saturation as well (in terms of accounts). The degree to which mobility services will limit further growth, and then possibly cause fixed network internet access decline is among the next big issues.

The offsetting trend is data access to support internet of things apps and services, which will add accounts and revenue, though not with the same level of average revenue per account. On a per-device basis, IoT devices might represent monthly revenue an order of magnitude lower than services for smartphones, for example.

Still, demand for internet access connections “for humans” is reaching saturation, in either fixed or mobile realms. That trend remains latent in many emerging markets, where net growth of accounts and revenue is possible.

Eventually, though, even burgeoning mobile adoption and mobile internet access in emerging markets likewise will peak.

That is why internet of things is considered so strategic a development in the access business: it represents the single biggest new revenue driver to replace lost legacy revenues over the medium term.

At the same time, value and revenue within the communications and internet ecosystem are shifting to the application layer. That, in a nutshell, explains the key strategic problem for every tier-one access services provider, and the danger for small access providers.

Over time, tier-one providers must become significant owners of new application assets that are used by digital appliances and delivered over access networks. That will be the case even if IoT develops robustly as a new market for access connections.

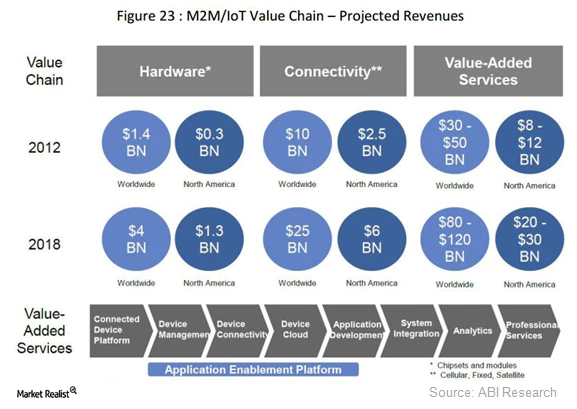

As one forecast by ABI Research suggests, as important a market as internet of things could be, more revenue will earned by app and service providers than by connectivity services (about three to five times more app/service revenue than “connectivity” revenue).

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

India Landline Accounts Fall 22% Last 5 Years

The number of landline telephone connections in India has shrunk 21.6 per cent in the last over the last five years, falling to 25.22 million in 2016, compared to 32.17 million lines in 2012, By the beginning of 2017, connections had fallen further to 24.34 million.

That “drastic” fall should come as no surprise. That trend has been in place since 2012, when analysts at Gartner predicted that, from 2012 to 2016, fixed voice revenue would decline by 25 percent. And the same trend has been seen in many other markets.

In substantial part, that is because--as happened in other markets--consumers switched to use of mobile phones for voice communications. In the U.S. market, voice lines peaked in 2000 or 2001, and the only issue now is whether a stable base eventually will be reached.

Such declines in voice are not unusual. It is easy to argue that peak messaging (the carrier text messaging market) likewise is past peak adoption. Some might warn that although mobile service provider revenue continues to grow, it now expands at less than the growth of gross national product.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

Whatever the Eventual Impact, Telecom Execs Say They are Investing in AI

With the caveat that early reported interests, tests, trials and investments in new technology such as artificial intelligence--especially t...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...