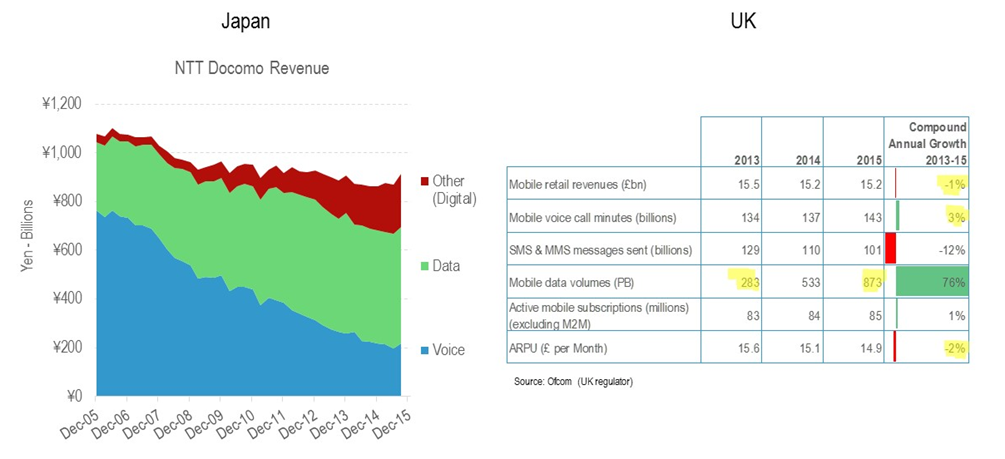

Some trends now are so well established they are a background issue, no matter how important. Revenue earned by mobile service providers, in developed markets, from mobile data, from human customers, has past its peak. In markets such as Japan and the United Kingdom, mobile data, no matter how important, is no longer driving growth.

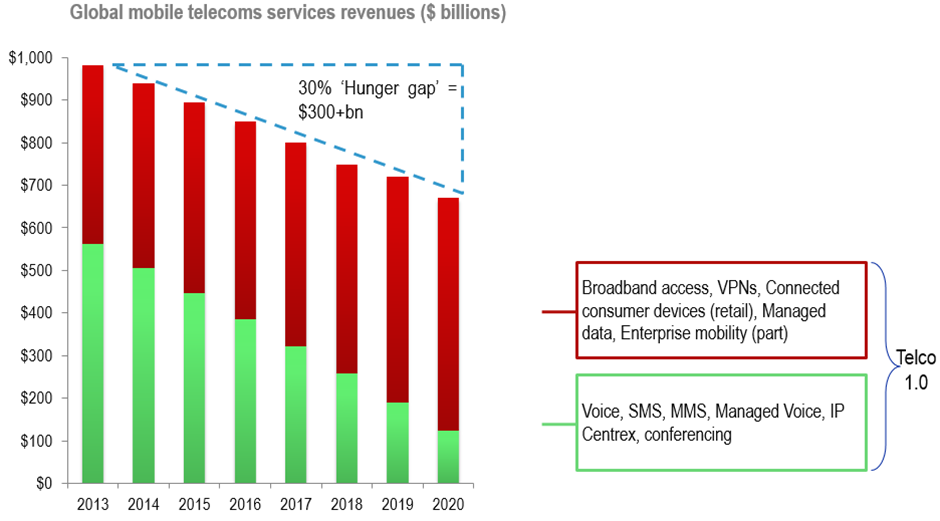

That is why hopes for internet of things are so important. Growth prospects for all human uses of mobile services--with one possible exception--are largely negative, in developed markets, even if growing in developing regions.

That possible exception is entertainment video. If some mobile operators can shift enough market share from traditional fixed network linear video services to “owned” mobile video services, that access revenue segment still could grow.

The other important shift is indirect. Or, one might say, what happens with telco diversification efforts. Put simply, the access business is declining, in mature markets. To keep growing, service providers will have to hope IoT really is as important as many believe.

Even so, IoT access revenues might only replace lost “revenues generated by services to humans.” To truly grow, access providers will have to transition to new sources of revenue based on content, platforms, transactions, advertising or other sources.

That is a very tall order for an industry that has struggled for success in most business lines outside the network services domain.

However difficult, that is what has to happen. Among the most-successful access provider transitions has been made by Comcast, which made the leap from video distributor and provider of other access services to owner of major content assets, ranging from studios to theme parks to content networks.

That’s the essence of the strategy: move to revenue sources beyond access, both consumer and enterprise. Be it connected vehicle or other services and apps, the key is to own the assets that are used by customers who need the access networks to do so.

That noted, the next wave of new sources also will come from sensor connections--or machine-to-machine apps and services--or might not come at all.