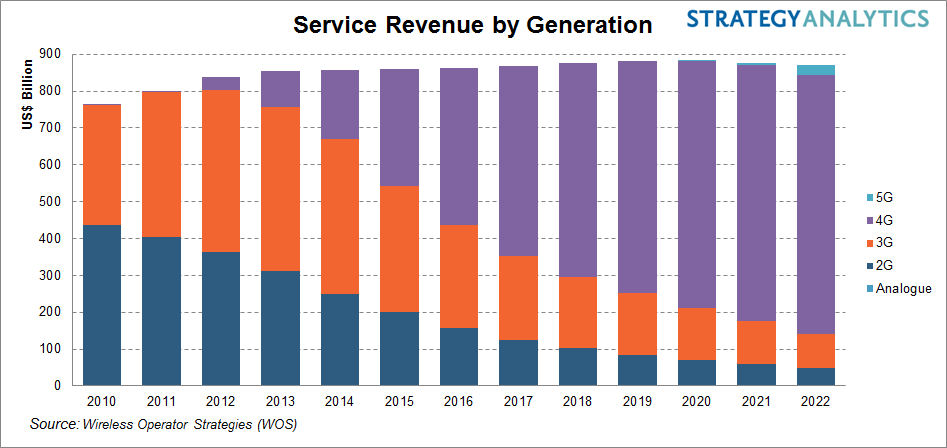

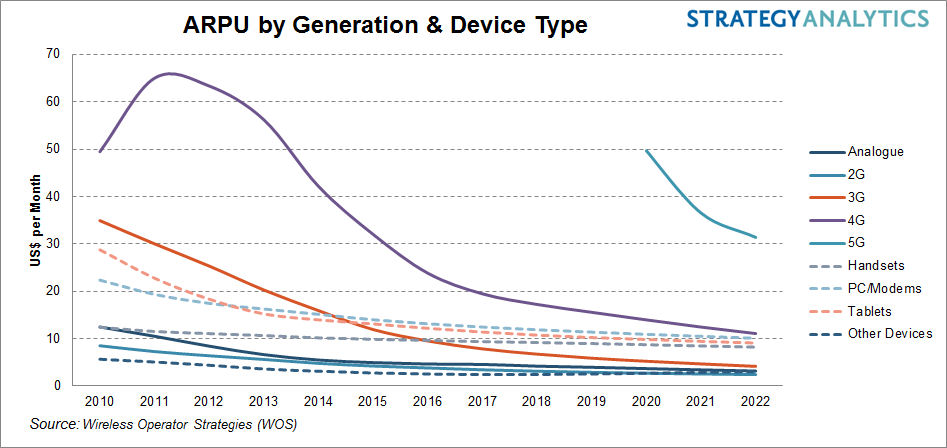

In many parts of the world, people will question why we seemingly are rushing to 5G. In one sense, we are not rushing. Mobile network generations tend to be upgraded about every decade or so, in large part because mobile operators arguably “run out of things to sell” in each generation.

When the ability to use voice on the go is the primary value, service provides eventually reach saturation. When text messaging becomes the “new thing you can do” with the 2G platform, another wave of growth happens, only to reach maturity at some point.

The third generation was the first to be based on the emergence of new apps beyond text messaging. For better or worse, it took some time for lead apps such as mobile email access, to develop.

The 4G network was the first to feature enough speed that video apps become feasible, and the first mobile generation where mobile apps and internet access actually became pleasant, in terms of user experience. Also, 4G was arguably the first mobile platform where internet or app use cases became dominant, eclipsing voice and carrier messaging.

Simply put, one might argue that, in the developed nations, mobile operators now have reached near saturation for all apps, all use cases and business models built on mobile apps and mobile internet access. Sure, 4G networks keep getting faster, but it is not so clear that revenue is keeping pace. In most markets, prices (and revenue) are falling or flat.

So 5G is seen as the way to create a revenue platform going beyond all existing major use cases. For that reason, 5G is virtually synonymous with IoT.

Faster speeds for human apps is going to be a feature of 5G, but not likely the main driver of new use cases. In fact, the conventional wisdom is that massively-faster human internet access is one of three fundamental use cases. The other two are internet of things and low-latency apps.