Network functions virtualization, which will be a foundation for coming 5G networks, also has direct implications for cloud data center costs, Intel and China Unicom and China Telecom, have found.

Virtualization has many facets, but always builds on a separation of control plane and data plane functions. In simple terms, that allows use of hardware from multiple suppliers (“commodity hardware”) to implement the control operations, a capability that should allow lower server costs.

The intermediate objective then is “virtualized software running on a standard server,” leading to lower capital and operating expense.

However, argues Intel, “many current virtualized network functions implementations are not well optimized for the new virtual environment and offer far less performance than their traditional proprietary counterparts.”

“While NFV, SDN, and orchestration can greatly reduce the operational complexity of deploying a telecommunications cloud, the infrastructure required to overcome the performance shortfall can be costly,” says Intel.

Control and User Plane Separation (CUPS), as defined by the 3rd Generation Partnership Project (3GPP), enables independent scaling of the control and data planes and is the next logical step for VNF design, Intel says.

While the control plane is easier to scale using standard off-the-shelf compute and memory resources, scaling the data planes to support complex packet processing at high rates can be challenging, says Intel.

The opportunity is to design a system where the data plane can support reconfigurable packet pipelines and complex packet processing at very high throughputs.

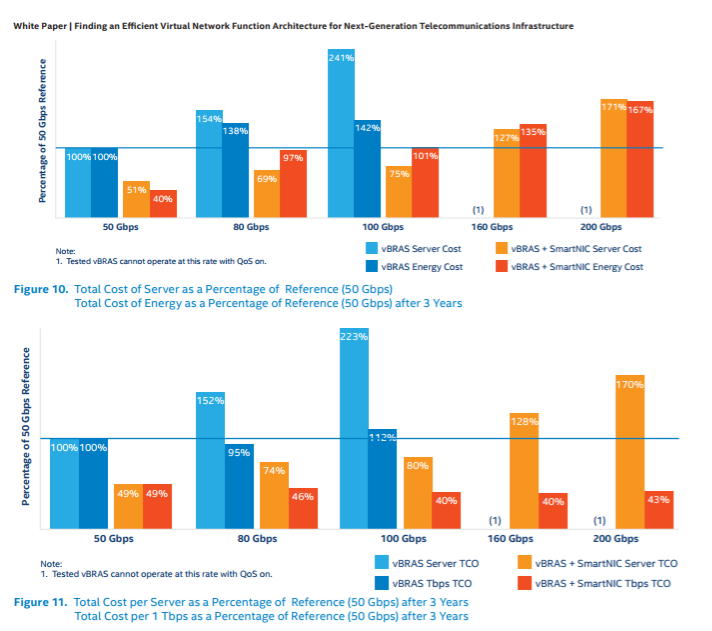

For example, in recent deployments, the Intel SmartNIC solution, deployed with HP Enterprise gear, achieved a total power reduction of about 50 percent compared to a standard NIC server.

Together, the Intel Arria 10 FPGA-based SmartNICs and commercial server central processing units optimize the data plane performance to achieve lower costs while maintaining a high degree of flexibility, as well, Intel says.

Using SmartNICs improves performance and supports higher throughputs at a marginal power and cost increase, as well, Intel says.

HPE calls this their system for virtualizing data plane resources “vBRAS” (virtual broadband remote access server) technology. VBRAS scales the control and data planes independently on physically separate, standard off-the-shelf server platforms.

The data plane is optimized for packet processing and also accelerates computationally-intensive traffic shaping and quality of service functions, which is more efficient, and allows operation at lower costs.

In a second case, Intel is enabling mobile edge computing for China Unicom. Nokia designed and developed it to run on the Intel Xeon processor.

The design allows extending data center solutions to the very edge of the network. That, in turn,

Improves mobile user experience by providing high availability of content with reduced latency.