Something new is happening in the global mobile business. Facing financial distress, entities tend to sell themselves. But what happens if potential buyers simply see such dire circumstances that a purchase does not make sense?

That appears to be a danger for Oi, the bankrupt Brazilian former incumbent. Inability to merge or sell has been an issue for Reliance Communications in India, as well.

So the new trend that bears watching is whether business conditions might get so severe that a struggling service provider cannot sell itself, because there are not willing buyers.

In other cases, such as the proposed T-Mobile US acquisition of Sprint, no acquisition premium has been proposed, as normally would happen. In other words, the buyer sees little reason to pay any premium.

All those situations--no takeover premium; no ability to entice a buyer or no ability to arrange a merger--suggest that the value of telecom assets is in some growing number of cases in danger of falling.

Whether that value can fall so far that complete shut down (liquidation) is the only available option is among the questions that must now be asked.

If that starts to appear in numerous markets, the logical consequence will be that equity values of most telcos will start to fall. That is a significant new business problem, in addition to revenue growth, profit margins, falling average revenue per account, competition and growing capital investment or operating cost issues.

A half century ago, the idea that a country’s national telecom provider could go bankrupt likely was seen as highly unlikely. Since all telecom companies were “sole provider” government-owned entities or monopolies, a bankruptcy, one would have argued, would imperil the national economy and therefore would be prevented by government intervention.

In the competitive era, we have become accustomed to the idea that smaller and competitive service providers indeed can go out of business. But there have been few examples of tier-one, former-incumbent service provider bankruptcies.

That now has happened, as Oi, the former incumbent in Brazil, has entered bankruptcy, albeit the more-familiar “restructure to stay in business” variety, not the “going completely out of business” version of bankruptcy.

Under the best of circumstances, a firm attempting such a gambit would wipe out its equity holders, restructure its debt and try again. In other cases, a buyer might be sought. It is not clear whether any buyers exist for Oi, some would argue.

The problem is the seemingly-unstoppable decline in the legacy fixed network business, which obliterates the contribution made by Oi’s mobile business.

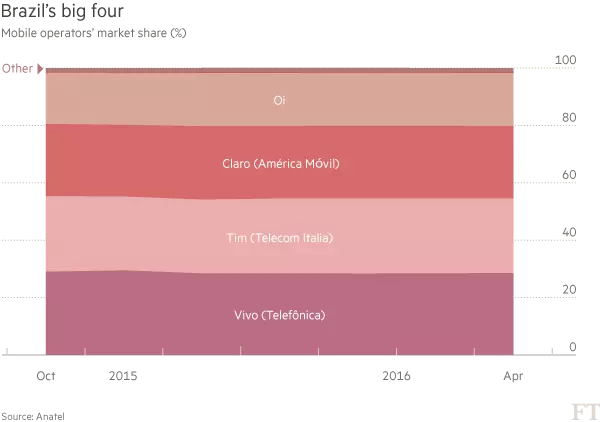

Like many other markets, Brazil’s mobile market features four strong contenders, a situation many would say leads to depressed profits, as beneficial as that level of competition might be for consumers.

Though it is possible to envision a stable oligopoly, a mobile market with four roughly equally-matched suppliers is not sustainable, many would argue. Eventually, consolidation that creates a clear leader, with at least one strong follower, is probably necessary to sustain long-term profitability in the market, as that situation discourages uncontrollable price competition.

In principle, oligopolies are the likely “normal” market structure in the capital-intensive telecom business. In the mobile business, the key question now is whether “three” contestants is stable and sustainable, or whether even that is too many, in some markets.

Oi has nearly 19 percent share. Vivo, the market leader, has nearly 29 percent market share. TIM has 26 percent share, while Claro has 25 percent share. The “perfectly stable” market structure might have something approaching a 50-25-13 market share structure (plus or minus five share points for each contestant).

With such a structure, no provider has huge incentive to launch destructive pricing wars to gain share, as the other contestants can be expected to simply respond, depressing prices and profits across the board, without changing market structure.

source: Anatel