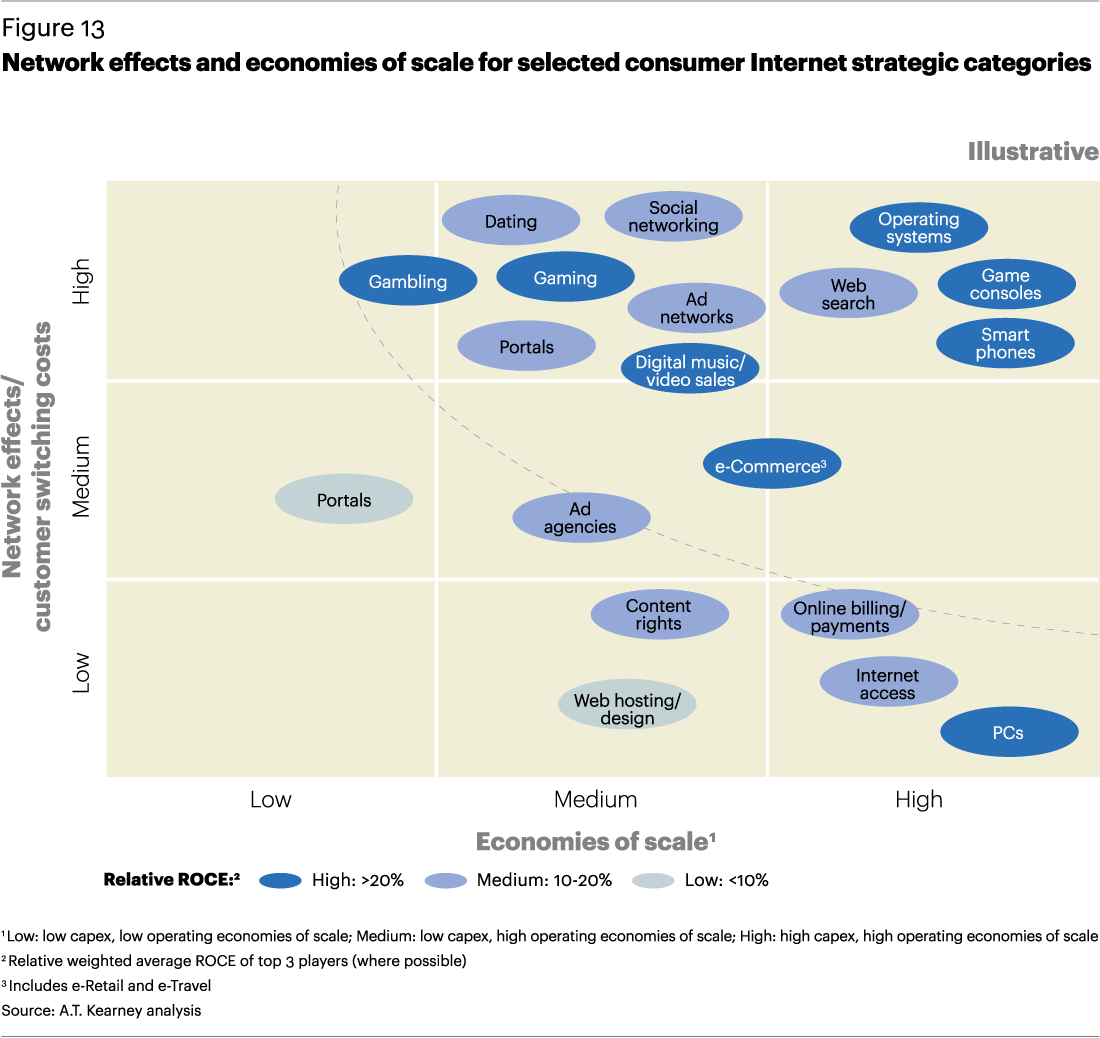

It is a truism that network effects are key to many businesses and industries, ranging from social media networks to access networks. The network effect describes a situation where the value of a product or service is dependent on the number of others using it.

But there are other “scale” effects that shape the profitability of business models, ranging from “economies of scale” (lower unit costs possible because of customer mass or volume) to “economies of scope” (efficiencies created by product variety, not single-product volume).

Ideally, if one had a choice to operate in any industry, the “best” pick would be an industry with low scale requirements and high barriers to consumer switching behavior. Such industries are hard to find, as many consumer-facing businesses require scale.

In that respect, internet access is in a difficult environment. It requires lots of capital, tends to earn lower profit margins than many other industries, requires some amount of scale and yet also has low barriers to customer switching behavior.

So scale does matter. Scale helps a supplier cope with high churn and high fixed costs.

There are other nuances. Economies of scale can be built on the producer side (firms get bigger) or the consumer side (more customers join a single network).

In the U.S. mobile service provider business, both producer and consumer network effects are important, but arguably less important than the scale advantages (scale and scope). In principle, every mobile customer, on any network, can communicate with all other customers of all other networks, meaning that the network effect for “mobility” is very high, even if, at the firm level, there is not such a network effect.

In other words, the universe of networks enjoys high network effects, even if no single small mobile service provider can gain such effects on its own.

Perhaps oddly, the network effect no longer confers mobile or fixed service providers much business advantage, since all suppliers must interconnect. On the other hand, economies of scale and scope do matter quite a lot.

Small telcos, cable operators and internet service providers now find they cannot make a profit on linear video subscriptions, for example. Likewise, service providers that offer only a single service (internet access, voice/messaging or video entertainment) will find their business models quite challenging.