Annual global operator-billed revenues from voice and data services will fall by over $50 billion (about six percent) over the next five years, from $837 billion in 2017 to $785 billion in 2022, according to Juniper Research.

Other analysts think a global peak revenue might not be reached until perhaps 2021. Predictions for 2018 revenue range from flat to negative two percent.

On a global basis, the dollar value of operator-billed monthly average revenue per user fell by 62 percent between 2005 and 2017, to $9.20, Juniper Research estimates.

That decline is structural, and not caused by temporary issues such as economic slowdown.

That really should come as no surprise. Every telecom product has a product life cycle. Eventually, every potential prospect already has become a customer. Product substitution is happening, there is substantial new competition and mobile adoption in developing countries, which has driven global growth for more than a decade, is slowing.

In 2013, the dollar value of global operator-billed revenues fell for the first time.

In both West Europe and Central & East Europe, the dollar value of revenues peaked in 2008.

In 2017, three regions (Latin America, Central & East Europe and rest of Asia Pacific) saw year-over-year growth, but revenues were below peak levels, Juniper Research argues.

In 2017, operator-billed revenues had fallen to 86 percent of their 2013 peak levels; in West Europe, revenues are now just 58 percent of their 2008 high point.

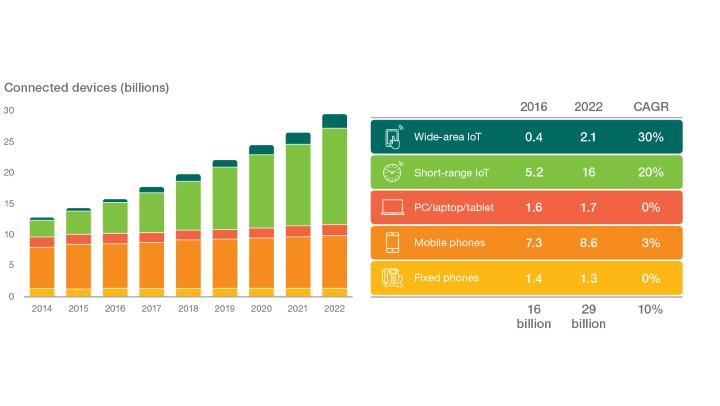

New revenue sources such as internet of things apps and connectivity will help, but will not replace the lost voice and internet access revenues. Internet of Things revenues might generate some $8 billion by 2022.