The extraordinarily high cost of reaching the couple percent of most-isolated U.S. households is one reason why alternatives ranging from 5G to fixed wireless to Google Loon, Facebook Aquila, Google Wing or new constellations of low earth orbit satellites really have to be looked at, as much as existing incumbents might prefer that not be done.

It would not be uncommon in rural areas for fiber to home networks to cost $17,400 per location, according to CostQuest Associates, which produced a recent report that makes the case for federal subsidies for broadband infrastructure.

“The capital investment per customer location, for conduit and poles, is approximately 5.6 times higher in rural areas as in suburban areas,” CQA estimates. “For fiber optic cable, the capital investment is approximately 4.2 times higher in rural areas as in suburban areas.”

The issue is whether any of the newer platforms, including 5G, fixed wireless, unmanned aerial vehicles or constellations of balloons or low earth orbit satellites are commercially viable.

A recurring issue, of course, is which entities should be eligible to apply for such subsidies. In the past, and at present, legacy fixed network providers have been prioritized for federal subsidies, although in the past mobile operators have, in some cases, been eligible to apply for subsidies designed to promote investment in high-cost areas.

But subsidies have used a mix of approaches, including cross subsidies. In the past, revenues earned from urban areas were used to support service in rural areas. Revenues and profits from business users were applied to consumer communications.

High-profit long distance subsidized local service. In addition, the federal government has provided direct support for high-cost areas. The Rural Utilities Service also has provided ost grants and low interest loans, while states have run their own universal service funds.

All of that is breaking down since the traditional “high profit” sources are dwindling in the competitive era.

R

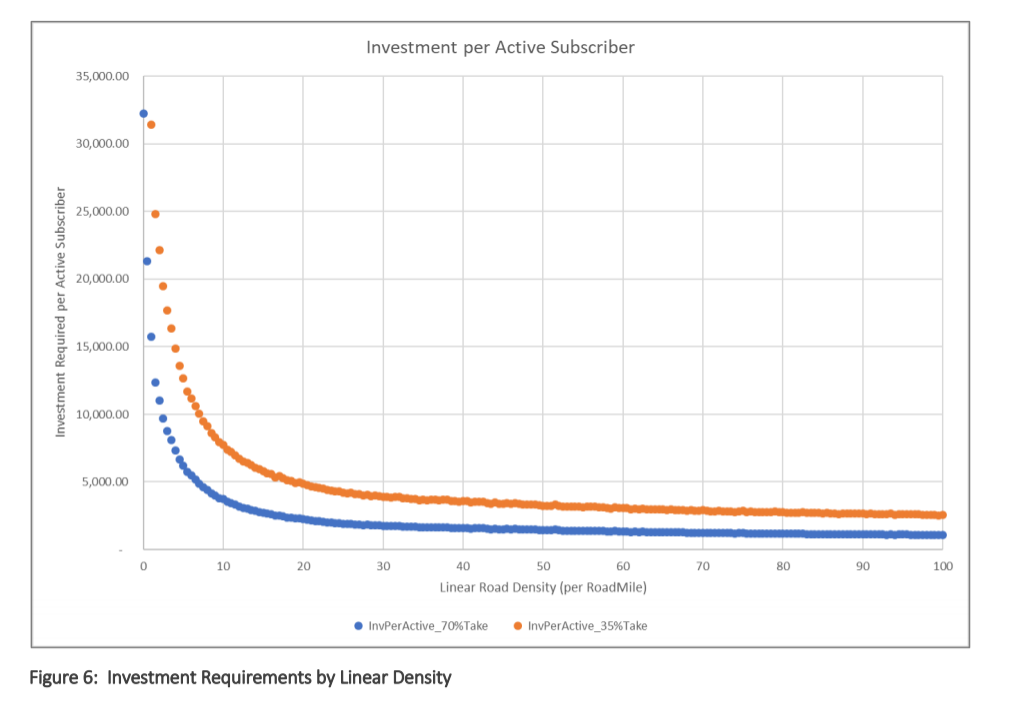

The other issue, though, is the impact of competition on the business model, no matter what network platform is chosen. Take rates, especially when customer density is lower than about 10 homes per linear mile, have a major impact on capital investment.

The point is that very-remote locations might simply be unfeasible to connect using fiber-to-home platforms, even with subsidies, and have typically been candidates only for satellite internet (geosynchronous or low-earth or medium-earth orbit).

Moderately-remote areas might be candidates for any number of existing and new platforms.