New Cord Evolution research from GfK MRI shows that 71 percent of all US consumers say they have cable, satellite, or telco TV service and have no plans to drop it. This includes the majority of the crucial 18-to-34 age group (58 percent), as well as 69 percent of people ages 35 to 49, and 80 percent of those 50 and over.

Two decades ago, the thinking often was that younger consumers inevitably would start to behave as did older age cohorts. Very few now are so sure.

But there remains a big difference between demand for various forms of entertainment subscriptions and demand for entertainment. The former might change; the latter arguably does not. So the form of supply is likely to evolve.

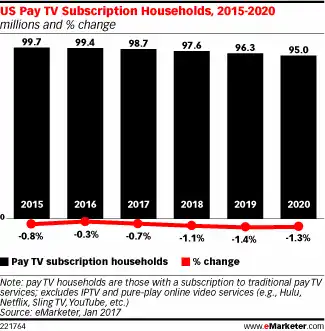

But cord cutting--the shift to internet-delivered content services--does not diminish demand for such content. And even linear forms of delivery might decline rather slowly if suppliers are able to tweak the value proposition.

Virtually nobody disputes the notion that consumers are less inclined to buy linear video services these days, or that streaming alternatives are the new choice for most consumers, either as a complement or substitute for linear subscriptions.

But entertainment video substitution might--or might not--not take the pattern of voice substitution, in terms of simple abandonment an older landline product and a shift to mobile substitutes.

And demand change was more complicated than we often suppose. In addition to the value of mobility, cellular phones personalized voice communications. Where voice was a service “to a place,” mobile telephony changed the context to “communications with a person.”

So mobility represented higher value, not just a change of cost function.

At the same time, the value of internet apps and experiences also changed the role of the devices, lead apps and volume of interactions.

In the case of landline voice, customers in developed regions simply are abandoning their landlines, as mobility provides a satisfactory or preferred use mode. People in the U.S. market also are simply calling less, as more communications take other forms.

The point is that linear video cord cutting might take more-subtle forms than we think, at least in part because content contracts make linear services the only way to get some content, or make the cost of access to much desired content too complicated or expensive any other way.

There are, in other words, many instances where a “lower price for the content you want” strategy will prevent or slow the rate of cord cutting.

In the case of entertainment video, the value of a linear subscription endures, for many consumers. It is the perception of price and value that generally leads to abandonment. That is why “skinny bundles” should work: such bundles change the value proposition.

Nor are streaming services a complete alternative to linear services. That is why so many people try to “cut the cord” and find the present alternatives not as attractive as once believed. Sports content, for example, often cannot be obtained except as part of a linear bundle.

Value also is why so many people buy both linear and over the top streaming services, or buy multiple streaming services.

In the case of text messaging, people switched to substitute apps, so that in the United Kingdom, for example, the typical user now sends fewer messages in 2017 than in 2012.

The big legacy providers of linear video will continue to reprice and repackage linear offers in ways that boost value while containing retail cost.