With the caveat that higher-income households might not face so many choices, the cost of linear video subscriptions arguably is a problem for median-income households.

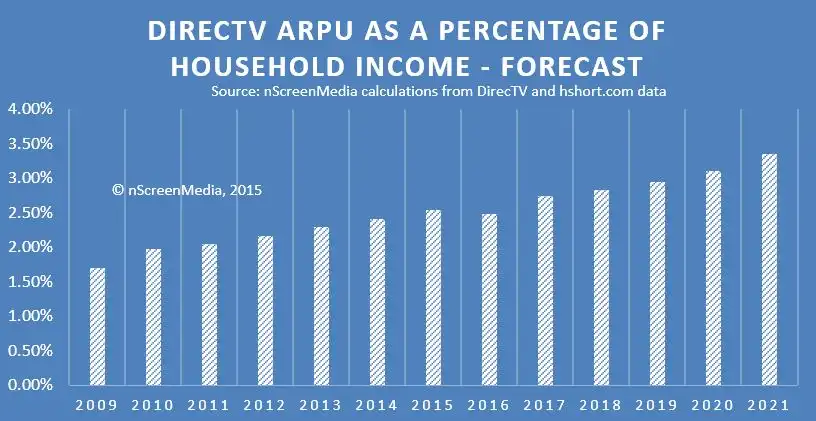

Consider the key issue of ability to pay. There is some evidence that explains why lower-cost streaming alternatives (live TV and non-real time) are growing. Researcher SNL Kagan said in 2015 that DirecTV subscriptions represented as much as 2.4 percent of median household income. That was expected to grow to perhaps three percent of median household income by about 2021.

That is unsustainable, some of us would argue. Increasingly, entertainment video is part of total household spending on mobile communications, internet access and other related services. So the issue is not just how much is spent on video subscriptions, but also how much is spent on communications of all types.

In developed countries, household spending on internet access, for example, is less than two percent, but added to just one linear video subscription could mean that as much as 5.4 percent of household spending is for one video subscription and fixed network internet access.

Then one has to add mobile service, which in a four-person household could be close to $200 a month, or perhaps another five percent of household income. So now more than 10 percent of median household income would possibly be spent on mobility, TV and internet access.

That exceeds what most median households probably could afford to spend (again, with the caveat that higher income households might spend more than that amount).

In 2016, the entire household entertainment budget in the United States was about four percent of average income before taxes in 2016, for example.

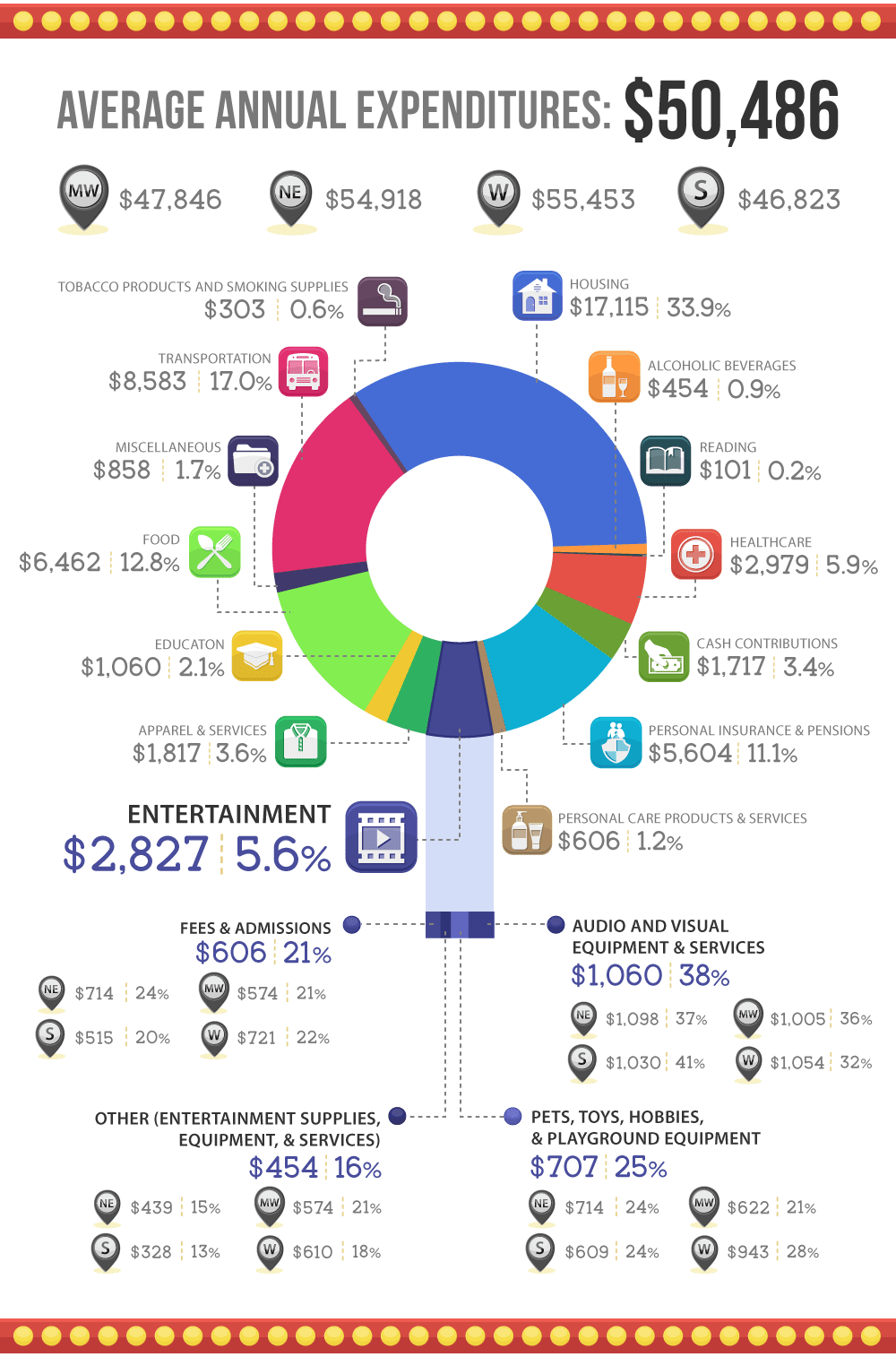

According to another estimate, U.S. households spend 5.6 percent of their household income on “entertainment,” but that includes spending on pets, tickets to events, audiovisual equipment such as TVs, hobbies and other services that include video subscriptions. Other U.S. Bureau of Labor Statistics data for 2016 suggest households spend about five percent of income on “entertainment.”

But a study by Pew Research suggested in 2016 that U.S. households spent only about 2.3 percent of income on entertainment.

The implications are clear. Whether you believe a household will spend two percent or five percent of income on entertainment, that budget does not change much. In 1996, Pew researchers say households spend about $1444 on entertainment. In 2016, that amount was $1496. That is the median spending for households with two working parents and two children.

On a per-capita basis, that is only about $374 in 2016, but s single linear video subscription at $80 a month would have represented $960, or 64 percent of the total family budget for all entertainment.

Also, keep in mind that healthcare spending in 2016 was about eight percent per household, according to the Bureau of Labor Statistics. Even spending on clothing is nearly And recall that pet expenditures also are considered “entertainment.”

If you want to know why a shift to lower-cost video subscriptions is happening, part of the reason is that traditional video subscriptions cost too much, as a percentage of total available entertainment spending.

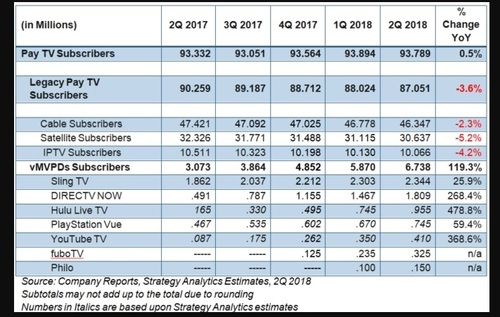

Still, some 63 percent of U.S. households have both linear TV and at least one streaming service as well, according to Leichtman Research Group. But more change is coming. In the second quarter of 2018, more live streaming accounts were added than linear accounts were lost. In fact, live streaming accounts grew as much as four times faster than linear accounts were lost.

In the second quarter, the major linear service providers lost about 417,000 accounts, while six million to seven million live streaming accounts were added.

In addition to Netflix, Amazon Prime and other streaming services that provide non-real-time content, there is a new class of “live TV” streaming providers that are certain to become more important, as they are an even more-direct replacement for linear (live TV) services.

In the second quarter of 2018, for example, such co-called “virtual multichannel video programming distributors (vMVPDs) added 868,000 net accounts.

The total number of vMVPD accounts then reached 6.73 million, an increase of 119 percent, year over year.

Linear TV accounts (cable, satellite, IPTV, vMVPD) fell to 93.78 million, according to Strategy Analytics.