Arbitrage long has been a business model issue for access services, as illustrated by one advantage facilities-based 5G fixed wireless has over use of the Openreach platform.

According to researchers at Ovum: there is no need for consumers to pay £240 (about US$308) a year on line rental charges required when they buy any fixed network service offered using Openreach facilities.

5G fixed wireless, using millimeter wave spectrum, has performance is comparable to, or better, than existing fiber-based products, Ovum researchers say.

"We expect large-scale deployment to be able to consistently support speeds of 80 Mbps to 100 Mbps,” which is better than many existing fiber-to-curb connections, say researchers at Ovum. The average U.K. fixed network speed today is 46.2 Mbps.

Also, 5G-FWA can serve 85 percent of the existing UK fixed-line market, Ovum believes, based on current speed experiences. The percentage of urban customers receiving speeds below 80 Mbps is approximately 85 percent.

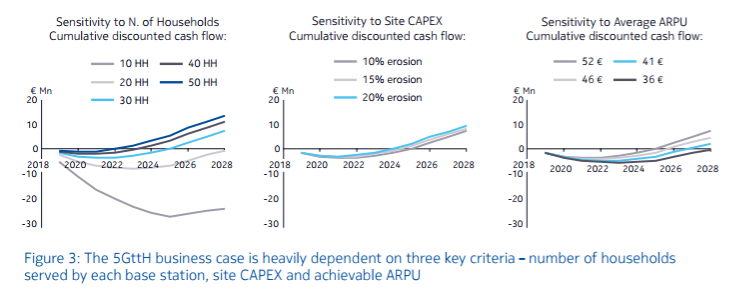

Overall, Ovum estimates 5G fixed wireless is almost 50 percent cheaper to deploy than fiber to premises, for example, based largely on construction costs. Nokia sees a positive business case when a fixed wireless network can reach 30 customers served per cell site, though obviously the model is sensitive to capital investment and average revenue per account.

The business model requires a 30-percent take rate. That is a lower threshold than generally required for a facilities-based fiber-to-home network.

Average revenue per account probably needs to be at least 40€ (US$43) per month, a target most consumer service providers should be able to hit with one service.