What might happen with linear subscription video depends on the popularity of product substitutes and the degree of competition in the market, as was the case for U.S. long distance calling after the breakup of the Bell system in 1985.

Also, much depends on which the market positions of various providers. The history of long distance calling provides an instructive example. Though competition shifted shares of market for two decades, the arguably bigger change came in 2000, when demand for “long distance” was cannibalized sharply by mobile phone service.

For two decades, though average prices continued to decline, the big change was market share shift. Then, for two decades, the big change was product substitution.

The application to linear video is that competition has been shifting market share for a few decades (first from fixed to satellite; then cable to telco). What we should anticipate in the coming decade is a change of dynamic from market share shifts to product decline and substitution (decline of linear and replacement by streaming alternatives).

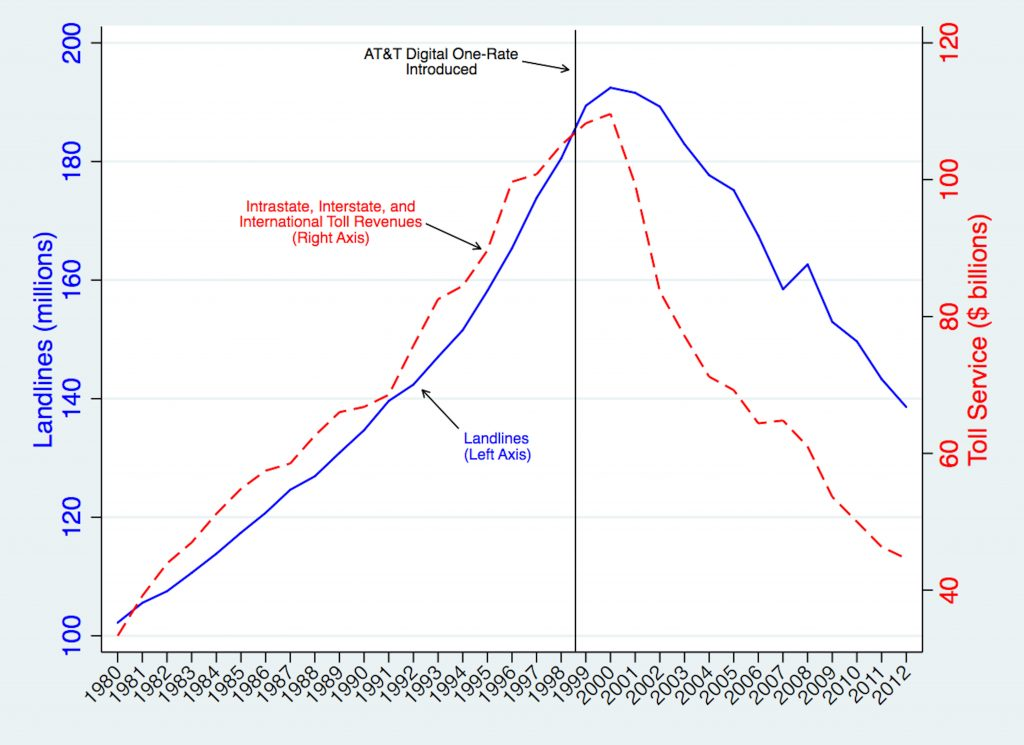

The whole point of deregulation is to shift market share from incumbents to challengers. In the U.S. market, regulatory support meant that attackers (the Baby Bells) steadily gained share, while AT&T lost share, from 1985 to about 2000.

Sometimes, though, unforeseen consequences are encountered. Virtually nobody thought long distance would almost disappear, to be replaced by mobility as the industry profit driver.

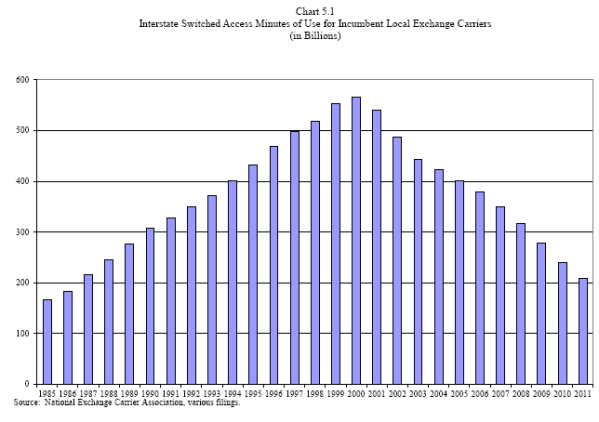

The long slow decline, when incumbents such as AT&T simply sought to control the pace of decline while trying to create a different business model, held for quite some time. But then a quantum change happened, and the whole market virtually collapsed.

After 2000, all fixed network providers lost share, as demand shifted to mobility, largely because AT&T introduced its Digital One Rate plan, which made domestic long distance calling as affordable as local calling.

The point is that the speed of such changes depend on the degree of regulatory support for challengers; technology shifts and shifts of end user demand.

As applied to the video subscription business, we have reached the equivalent of the 2000 peak of long distance revenues, which implies a long process of declining revenues. Where efforts to gain or protect market share were paramount for a few decades, the new challenge is to create alternative products.

As mobile calling became the substitute for both long distance and local calling, so over-the-top streaming services are destined to replace linear subscription products. There is one crucial difference, however.

It was, relatively speaking, easy to create free and low-cost communication alternatives. Video entertainment has substantial “cost of goods” issues, however, in the form of expensive content rights. It might be true that “bits are bits” where it comes to communication services or apps.

It is never true in the video entertainment business, as content is highly differentiated, as well as expensive.

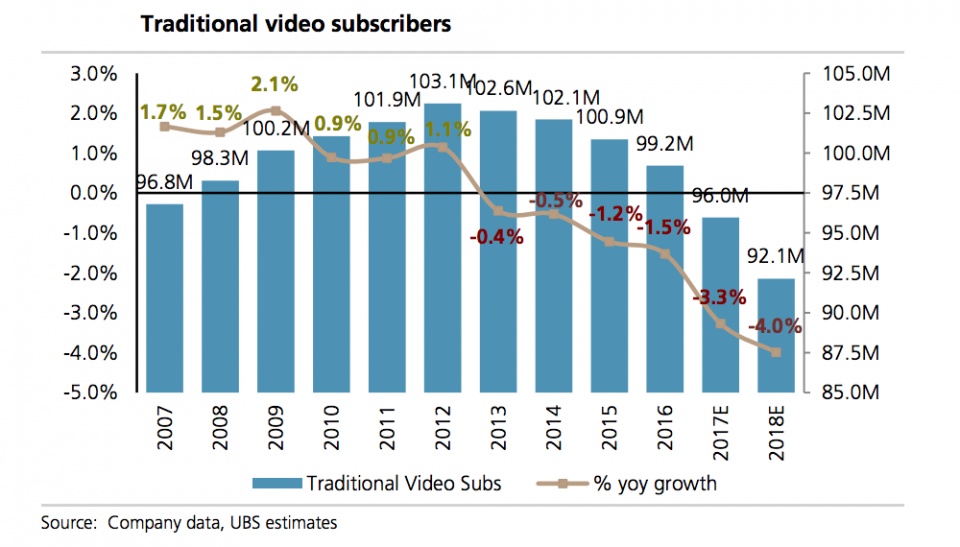

In the first nine months of 2018, some 23 percent of broadband households served by fixed network providers did not subscribe to a linear video service, according to S&P Global Kagan.

Over the first nine months of 2018, 2.8 million fewer linear video subscriptions were sold, with the biggest drops coming in the satellite segment of the distribution business.

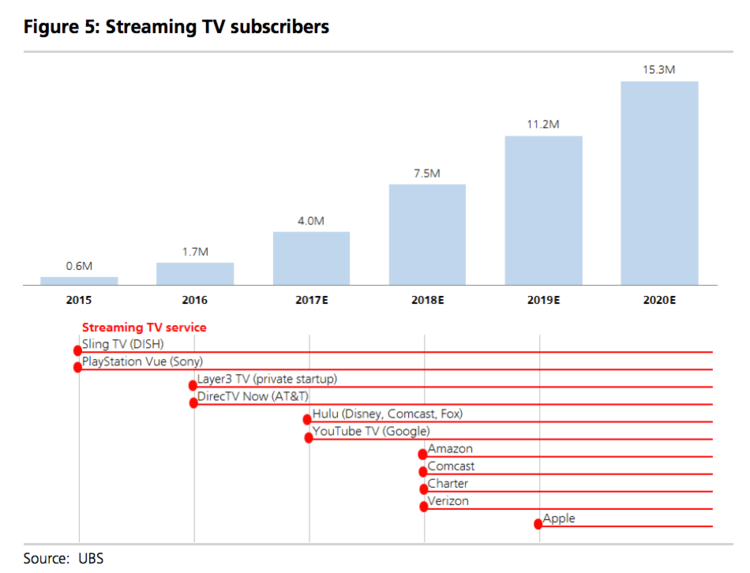

By 2022, analysts at UBS predict, such streaming alternatives will represent 25 percent of all video subscriptions.

UBS projects there will be 9.2 million video streaming subscribers by the end of 2018. UBS predicts there will be 24 million accounts by the end of 2022.

The new issue is what products will emerge to replace linear video, including streaming services that are optimized for mobile delivery as well as fixed network versions.