DirecTV Now will offer customers the ability to stream more than 100 channels of content on any device from a smartphone to a 55 inch TV starting at $35 a month with, no annual contract, no credit check, no installation charges, no set top box, and, for AT&T mobile customers, no data charges.

Margins will be super thin to non-existent, as the “cost of goods”represents as much as 97 percent of revenue. Craig Moffett, MoffettNathanson equity analyst, estimates the the cost of the channels expected to be included in DirecTV Now is likely around $34, which would leave just $1 a month before other expenses including overhead and marketing.

Under most circumstances, that sort of underlying cost, and retail profit margin, would be characteristic of a “loss leader.” And that is among the strategic principles AT&T likely is following: grab market share in a big new content distribution market. AT&T already is the leading U.S. provider of linear video entertainment, so assuming a “winner takes all” dynamic comes to characterize streaming video markets, AT&T would be compelled to aggressively take market share from the existing early leaders.

That, by the way, is characteristic of how big tier-one telcos, including AT&T, have in the past come to lead other markets. AT&T was not first to offer dial-up internet access or digital subscriber line services. Those markets were pioneered by independent third parties. AT&T was not an early leader in linear video services or mobile services (arguably).

That is not the only way AT&T has entered new markets such as connected cars, where it arguably is an early leader in the connectivity services segment of the market, but is an established growth strategy that might be called “let others pioneer; we will scale the business.”

DirecTV Now, the new AT&T streaming video service, is interesting and important for several reasons. The move illustrates a classic method by which AT&T and other tier-one service providers enter and lead big new markets.

The regulatory challenges posed by use of a single access platform (IP and internet) to support multiple business models bridging formerly-distinct industries also are key issues. In other words, as the single physical network now supports multiple logical services historically regulated in distinct and highly-disparate ways--from common carrier to unregulated content--how to regulate formerly-distinct industries becomes an issue.

Entry into the retail streaming video business also illustrates the broader strategic challenges faced by access providers, and the the growth model.

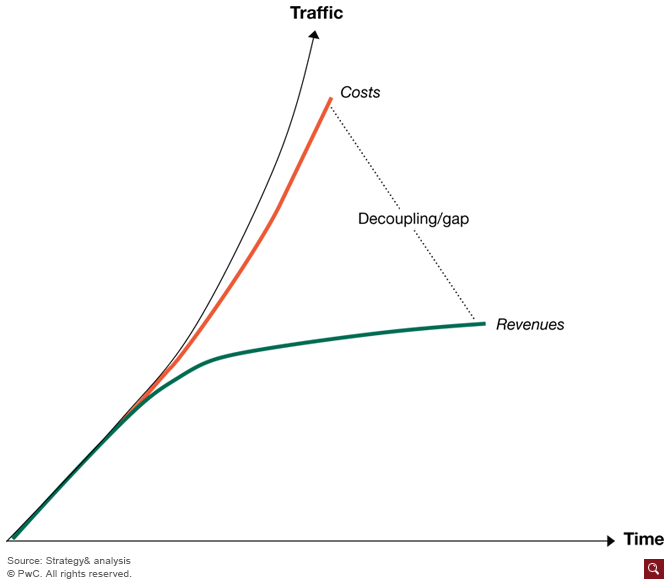

Finally, DirecTV Now also encapsulates the principle that “near-zero pricing” of both access and carrier services remains a key underlying reality--perhaps “the” underlying reality--faced by the access services industry.

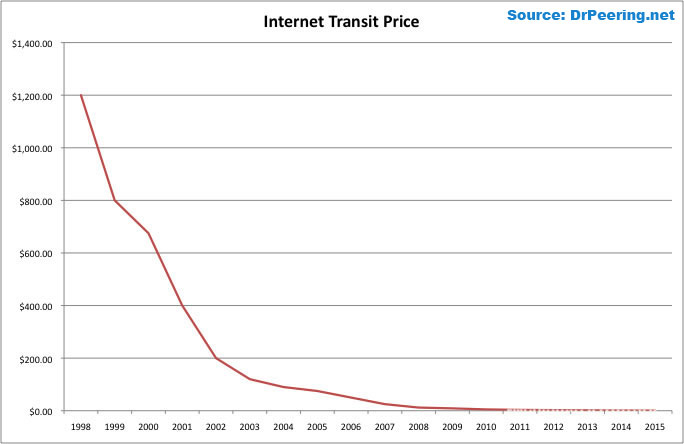

Perhaps shockingly, every carrier service is facing a long-term trend of retail pricing that moves closer to zero. That has been true of voice, messaging, internet access and entertainment video, not to mention wholesale services such as wide area network transport.

Some two decades ago, it was possible to hear top executives in the internet and computing industries argue that “bandwidth wants to be free,” with retorts that “software wants to be free.” As it turns out, both assertions captured the general movement of prices across access and software businesses.

With the caveat that “nothing is really free,” advertising-supported software is a dominant business model. Wi-Fi is the best example of “no incremental cost” internet access. But all “for fee” communications apps and services are trending ever-lower in absolute cost as well.