Up to this point, Apple has shaken up device markets. Unless Apple changes tack for the first time, it is likely to approach the whole subject of payments and commerce as a feature that drives sales of more devices.

That arguably means Apple faces more challenges than PayPal, Intuit or Square, for whom transactions directly drive business models built on transaction fees, or Isis and Google, which see advertising and marketing as the revenue model.

For PayPal, Intuit and Square, the revenue upside is immediate, and tangible. When merchants use their mobile card readers in conjunction with their own smart phones or tablets, PayPal earns a fee of 2.7 percent of the purchase price for all types of credit and debit cards Square earns 2.75 percent of the transaction amount.

For Isis and Google, which eschew such fees, the revenue model has to be created on something else, hopefully advertising and promotion revenues in the form of loyalty offers, targeted advertising or other marketing services provided to third parties. Isis partners and Google sell devices, to be sure, but the revenue model is built on services or advertising enabled by the use of those devices. Mobile transactions create the opportunity for those revenue streams, but transactions, as such, are not the revenue model.

Apple always has taken a different approach, namely creating services and selling content so it can sell more devices. That indirect monetization approach is more akin to what Isis and Google hope to accomplish, and far harder to create, in some ways.

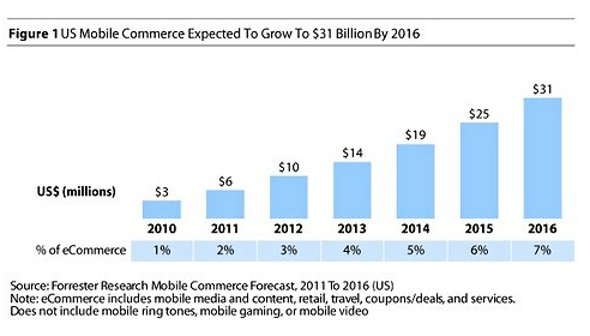

The volume of all types of mobile payments will top $200 billion by 2015, up from $16 billion in 2010, according to research and advisory firm Aite Group. So the direct, transaction fee approach is highly quantifiable.

The aggressive response by MasterCard, Visa and American Express in the mobile wallet and mobile payments businesses is is the latter case an effort to protect existing revenue from market share losses to PayPal, Intuit and Square, and in the former case an effort to build a new advertising or marketing business, an angle that tends to be overlooked.

Like many other big, established businesses, transaction processors face significant gross revenue and profit margin challenges, partly from regulatory action and partly from growing competition.

So there is a defensive angle to their mobile payments efforts, but also an offensive element to their mobile wallet gambits.

Apple has to figure out how any move into either mobile payments or mobile wallet helps it sell more devices, or create new markets for devices it can sell. As always, Apple will try to figure out how existing processes can be revolutionized, but it also has to figure out how changing the experience of “paying” for things and “buying” things also helps it create new markets for devices.

To be sure, iTunes and the App Store already have Apple involved in payment operations related to mobile devices that help it sell devices. What Apple has to do is figure out whether some broader approach to mobile payments and commerce could create a significant new product category, or allow Apple to take significant share in some existing product category.

The iPod and iPad essentially created new categories, while the iPhone and earlier Apple and Macintosh devices essentially reshaped an existing category of devices.

It isn’t yet clear whether Apple has a clear vision, yet, of what big opportunities exist, or whether the approach is to create a new category of devices, or reshape an existing category.

Sometimes Apple has created a brand new category, and at other times has reshaped an existing category. Apple’s continually-rumored interest in TVs is another example of “reshaping” an existing category, for example.

If Apple stays true to form, it will try to understand what is “broken” about e-commerce, mobile shopping and payments, and work from there on a solution. In fact, broader e-commerce might be the approach, rather than “mobile payments” in a direct sense.

No comments:

Post a Comment