The TIA also expects cloud computing will continue to be the fastest-growing category of network and facilities investment during the next four years, averaging 20.3 percent compounded annually.

But it is end user spending that arguably drives most of the revenue, so one might argue that much of the opportunity will be reaped by firms that sell enterprise applications, not firms that sell infrastructure services more centrally related to hosting, for example.

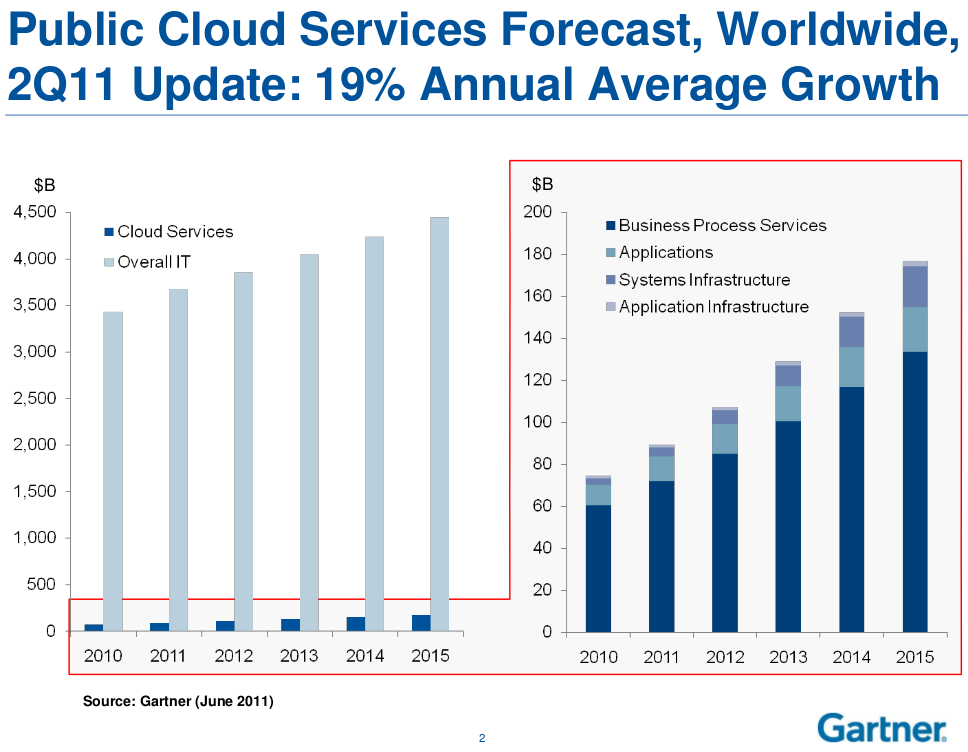

TIA argues that end user spending on cloud apps will more than double to $12.1 billion in 2015 from $5.8 billion in 2011, according to the TIA. Separating out what that could mean for providers of cloud “data center facilities” is harder to assess.

In fact, most of the revenue upside appears likely to accrue to hardware and software suppliers, at least initially, according to a Morgan Stanley analysis.

In the infrastructure end of the business, telecom service providers might make a business out of rental of computing cycles, storage and ancillary services. But what has to be done to market and support that business, and should effort be put elsewhere?

In the telecom space, the analysts expect key winners to include Rackspace, Equinix and competitive local exchange carriers and metro bandwidth suppliers. In other words, hosting and access will be where the telecom revenue lies, possibly not in the infrastructure, platform or software as a service businesses.

The point is that assessing cloud computing revenue contributions for various ecosystem participants is complicated.

That forecast suggests why cloud computing initiatives by telcos will have to be targeted. There actually isn’t as much revenue in cloud computing as some tend to think. Nor is the space uncontested.

Companies such as Google, Amazon Web Services, Hewlett-Packard Development Co., Microsoft Corp. and Salesforce.com are themselves already leaders in the cloud infrastructure space, and already are displacing traditional infrastructure outsourcing alternatives, one might argue.

North America, specifically the U.S., currently represents the largest opportunity for SaaS, and it is the most mature of the regional markets. SaaS software revenue is forecast to total $9.1 billion in 2012, up from $7.8 billion in 2011.

But keep in mind that most of that revenue is earned providing expense management, financials, email and office suites. Though Web conferencing also is a SaaS application, few telcos are players to any major extent.

In Western Europe, SaaS revenue is forecast to surpass $3.2 billion in 2012, up from $2.7 billion in 2011, while SaaS revenue is Eastern Europe is projected to reach $169.4 million, up from $135.5 million last year.

SaaS revenue in Asia/Pacific is on pace to reach $934.1 million in 2012, up from $730.9 million in 2011.

SaaS revenue in Latin America is forecast to total $419.7 million in 2012, up from $331.1 million last year. None of those revenue streams are terribly large, by tier one service provider standards, nor are telcos the most logical providers.

In addition to the possibility that cloud-delivered enterprise apps compete most centrally with distributors of "shrink wrapped" apps, it can be argued that cloud infrastructure also competes with traditional "outsourcing" services.

Cloud infrastructure services are an alternative to traditional IT outsourcing services, often reducing the IT costs of their clients by at least 40 percent, according to livemint.com.

Likewise, you might argue that enterprise or other "app stores" might also compete with other software delivery channels.

What you will note about the enterprise app store concept is that it disintermediates nearly all of the premises networking infrastructure. There is no need for the enterprise local area network, except perhaps to switch to Wi-Fi access at times.

You can imagine this will have serious implications for firms that traditionally make a living selling gear and services for enterprise LANs. Just as easily, you can see the upside for traditional communications providers who now could have an expanded role in the information technology business.

What products would be “natural” parts of a communications and information technology bundle? How much easier would it be for traditional telco sales organizations to sell key business software?

In fact, non-technical sales forces of all types might find there are new opportunities to sell products that might have been “too technical” in the past. Firms outside “IT” might find they can create bundles almost on the fly, customized for vertical markets or businesses of various sizes and types.

A shift to some new computing architecture based on cloud resources and mobility could have huge implications for any number of businesses in the information technology and communications businesses.

Although growing interest has been observed in vertical-specific software, the most widespread use is still characterized by horizontal applications with common processes, among distributed virtual workforces and within Web 2.0 activities.

Cloud computing will have implications for most firms in the business applications, information technology support and data center businesses. Whether that impact is large or relatively small is hard to say, at the moment.

No comments:

Post a Comment