How much market share can independent internet service providers take from cable companies, telcos and mobile operators? In the market as a whole, not so much. The business remains a matter of scale, and scale is expensive.

On a local level, the impact can be quite significant, in principle. In the mobile market, about two percent share is held by all firms other than the four national leaders.

Ting Internet has a rather dramatic set of assumptions for deciding where it enters a new internet access market: it assumes it will get 20 percent market share at launch, growing to 50 percent market share within five years, in markets where a telco and a cable operator already operate.

Aggressive? Yes. Even Verizon, where it has built and marketed fiber to the home services for years, typically gets market share only in the 40-percent range.

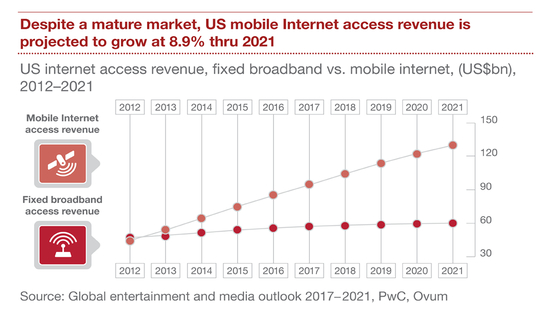

To be sure, the U.S. internet access market represents perhaps $160 billion in annual revenue, of which fixed access generates nearly $60 billion annually. But scale is hard to achieve in market so big.

Also, there is some evidence that users are switching to mobile internet access. Fixed network internet access subscriptions in the United States have declined in recent years, falling from 70 percent in 2013 to 67 percent in 2015, for example.

Some 13 percent of U.S. residents rely only on smartphones for home internet access, one study suggests. Logically, that is more common among single-person households, or households of younger, unrelated persons, than families. But it is a significant trend.

Some suggest that service providers are actively pushing mobile services as an alternative to fixed access, for example.

In fact, some studies suggest that U.S. fixed internet access peaked in 2009, and is slowly declining, though other studies suggest growth continues. Still, some studies suggest U.S. fixed network subscriptions declined in 2016, for example.

In the second quarter of 2017 alone, some 228,000 net new fixed network access accounts were added. Ting probably has about 3,650 total internet access accounts, and generates just over $4 million worth of annual revenue.

So Ting assumes it can, within five years or so, essentially relegate one or more of the two dominant providers to a barely-profitable or unprofitable status. The issue is how big a force Ting eventually could be, since capital is a huge constraint to its achieving meaningful scale in the fixed network internet access business.

Unlike some municipal or government network models, Ting does not assume it will get financial support from one or more universal service funds or a shift of existing government communications spending.

The Ting payback model also includes a fiber access network construction and then customer attachment cost of $2,500 to $3,000, with each customer expected to contribute $1,000 or so per year in gross revenue.

As others now do when building gigabit internet access networks, Ting also builds first in neighborhoods where it believes demand is highest, as demonstrated by customer deposits.

Some question the sustainability of the business model. So far, internet access arguably drives revenue growth for the company. It is fair to note that Tucows remains a small company, booking annual revenues of perhaps US$336 million.

Almost by definition, Tucows does not have the financial ability to take much total market share in the U.S. internet access market, dominated by firms with scores of billions to hundreds of billions in annual revenue.

No comments:

Post a Comment