It is long, but provides more color on Lumen's strategy than there is time to present at a quarterly earnings call. Useful is what one can glean from the mix of lines of business that are being harvested, versus the lines that are getting investment.

Thursday, April 8, 2021

Lumen Analyst Day 2021

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, April 3, 2021

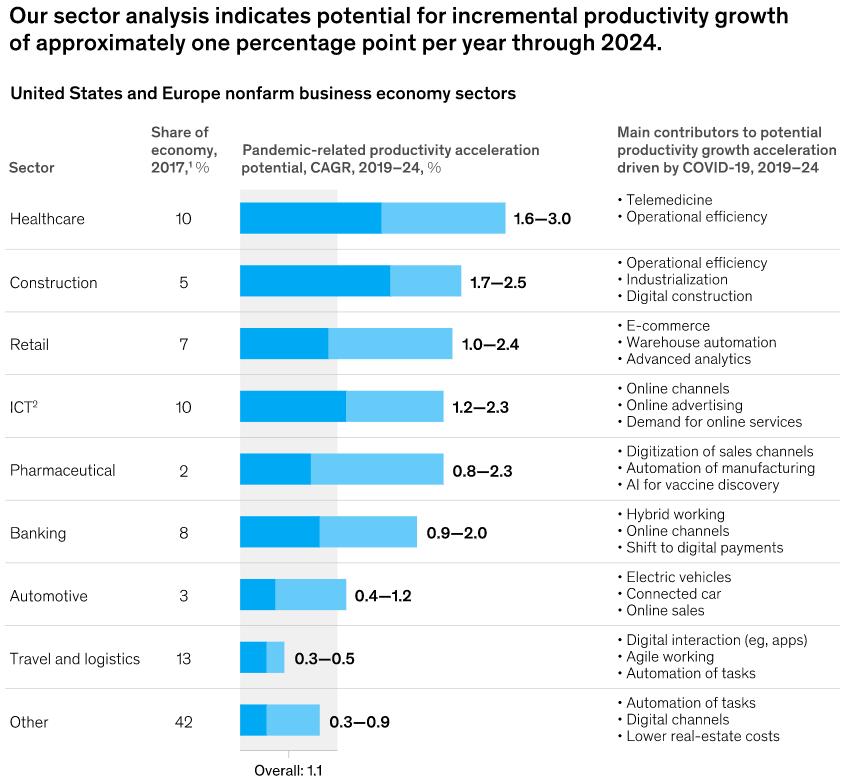

Big Firms Benefitted from Covid-19, Small Firms Did Not

The Covid-19 pandemic has battered small firms much more than hyperscalers or “large, superstar firms,” McKinsey data suggests. Between the third quarters of 2019 and 2020, “large superstar firms lost no revenue” while competitors experienced a decline of 11 percent, McKinsey says.

Looking at a range of revenue-related metrics and information technology investment, McKinsey researchers found that “advances appeared concentrated among large superstar firms, particularly in the United States.”

“This was true across many sectors, but particularly pronounced in professional, scientific, and technical services, IT, electronic manufacturing and healthcare,” McKinsey notes.

The McKinsey analysis included items such as spending on research and development, investment, mergers and acquisitions activity as short-term proxies for the range of potential drivers that could accelerate productivity.

The issue is what happens longer term as applied technology either does, or does not, positively affect revenue growth. A productivity paradox has existed in the past, where increased information technology spending does not produce a measurable increase in productivity.

“Before the pandemic, productivity growth had not always fully translated into broad-based growth in wages and consumption,” McKinsey notes.

Beyond that, the impact of “technology for labor” shifts “could, over the longer term, dampen employment and incomes, and hasten labor-market polarization and propensity to spend,” McKinsey says.

The point is that after a short-term economic rebound driven by economic reopening, longer term economic growth is not so clear. We should see growth, but how much is less clear. Many ICT investments operate on the cost side of the business model, not necessarily the revenues side of the model.

But cost for one entity always is revenue for another. Substituting machines for labor often is good for firms, but bad for employees and therefore reduces aggregate demand. Higher productivity is seen as a good thing.

Whether recent investments produce higher productivity remains to be seen. Whether such gains outweigh potential negative changes in demand is another question.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

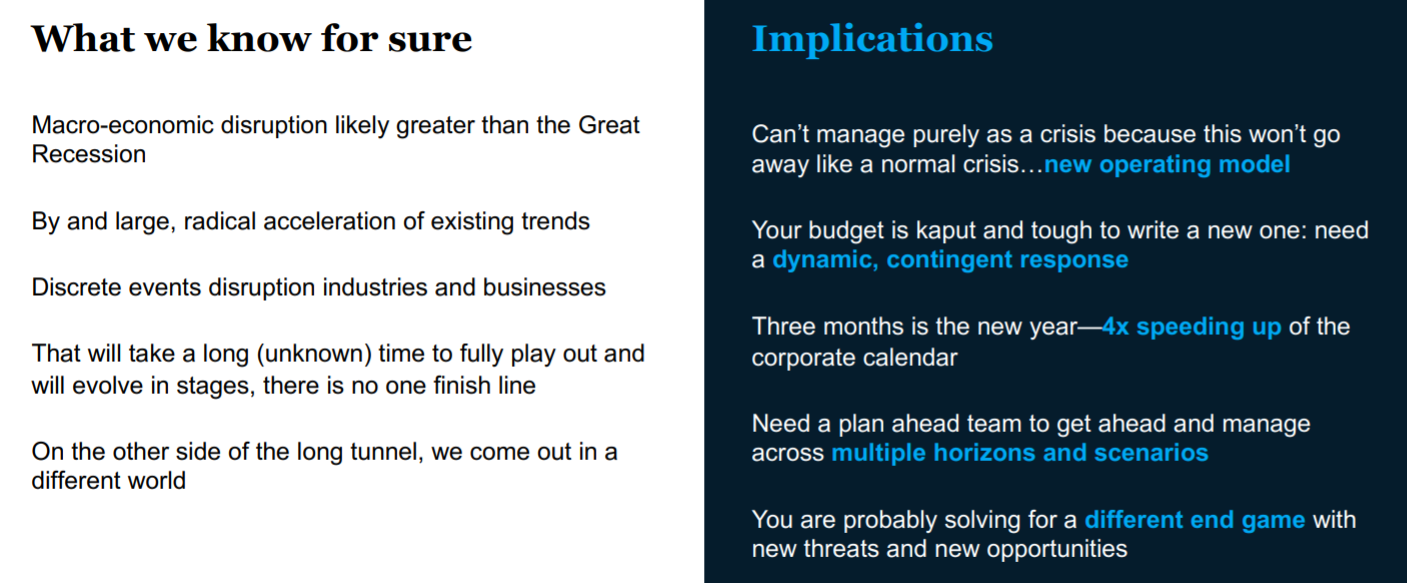

Implications of GDP Damage Worse than Great Depression, Far Worse than Internet Bubble or Great Recession

For those of you who lived through the internet bubble burst in 2001 and the Great Recession of 2008, the Covid-19 pandemic exceeds the economic damage by quite some scale, surpassing the carnage of the 1929 Great Depression.

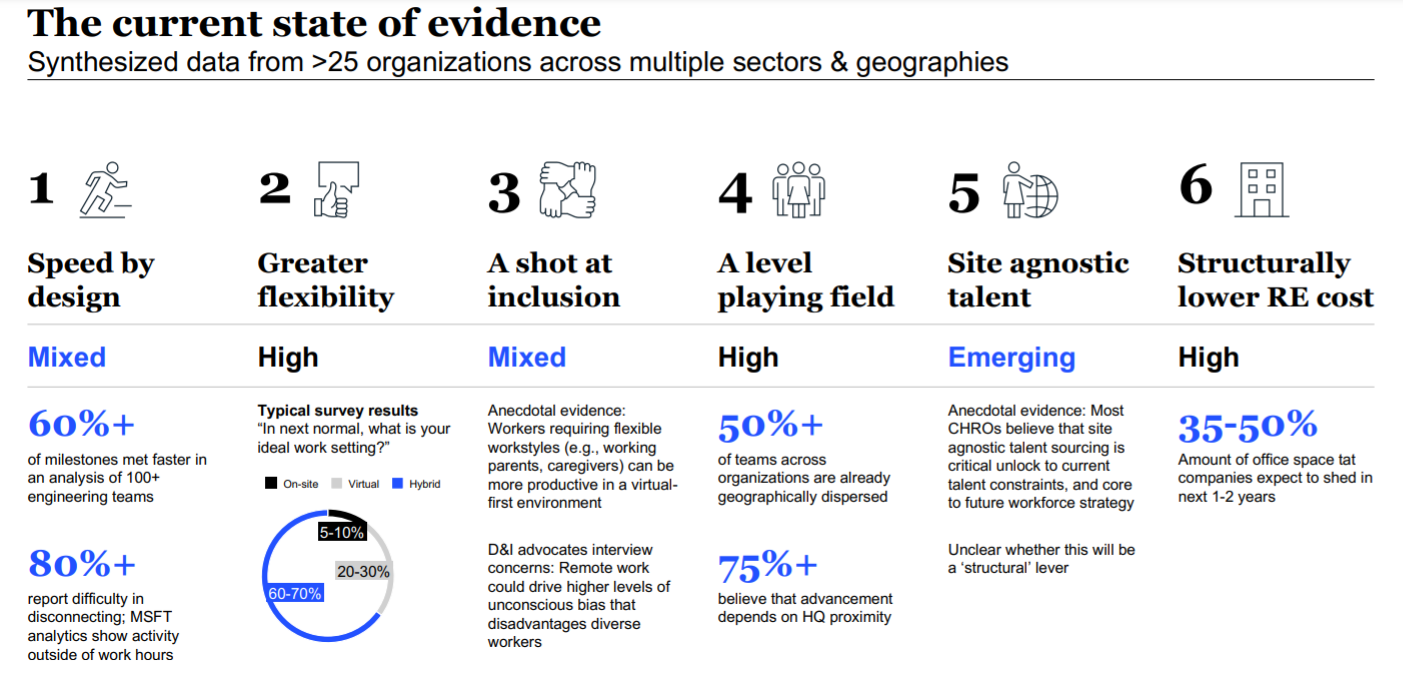

We all seem to sense that many changes in business and personal life will be permanent, post-Covid. Enterprise executives indicate big changes are coming.

Remote work environments seem to have encouraged “output oriented” work flows and may have enabled faster decision making, McKinsey reports. Hybrid work situations are expected to become permanent, while “site agnostic” employee sourcing will increase, along with possibly 35 percent to half of all existing office space to be shed over the next two years.

McKinsey argues that geographically “distributed work” produces more value than “remote work.” And those are not even the most important implications enterprises must consider. The “recovery” from the crisis will not follow patterns we have seen in prior economic downturns.

So a new operating model will be necessary. The need for agility no longer will be a nice to have organizational capability, but might be a requirement. Business will run about four times faster than in the past, making “three months the new year.”

New threats and opportunities might well be the new reality as well. That might well include a change of revenue sources and business models.

Lots of people talk about disruption. Not so many have actually had to face it. Many more might get their first chance to do so.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, April 2, 2021

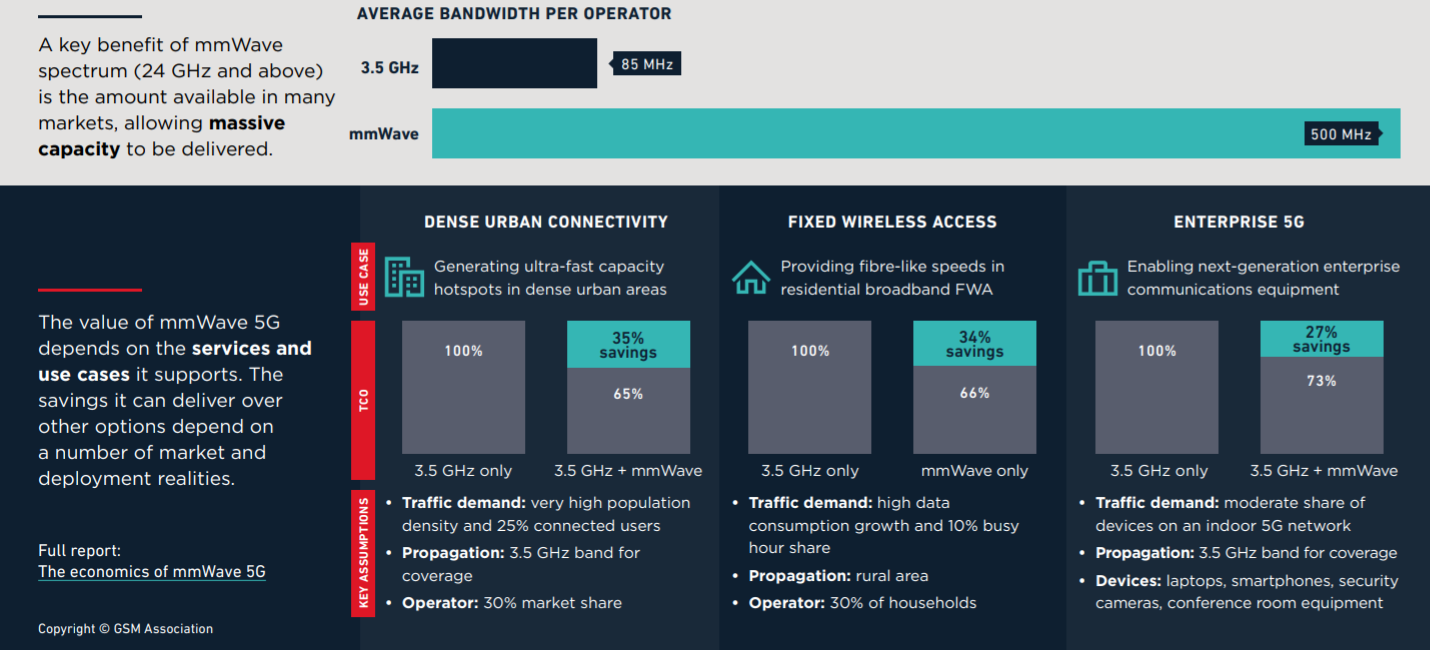

Why Millimeter Wave Matters

Propagation issues notwithstanding, millimeter wave frequencies will be vital for mobile operators. The pressure to achieve lower cost per delivered bit will not cease, forcing service providers to continually deploy new solutions for bandwidth with a lower cost per bit profile.

Millimeter wave does that. Eventually, so will teraHertz frequencies.

To be sure, 4G capacity increases will continue for a while. Eventually, though, 4G runs out of gas. Fundamentally, that is why 5G is “necessary.” Beyond all the other new use cases enabled by vaster-lower latency, core network virtualization or 5G-enabled edge computing or internet of things, 5G will supply bandwidth at lower costs than 4G networks.

Cost per bit matters because customer bandwidth demand grows as much as 40 percent a year, while consumer willingness to pay is limited, essentially remaining flat, year over year.

If access providers must supply 40 percent more bandwidth per year, while revenue grows one percent per year, bandwidth efficiency must increase significantly. That is the value of millimeter wave spectrum.

That need for efficiency would be true if access providers owned all the apps used by their customers. In the internet era, access providers own almost none of the apps used by their customers.

So connectivity providers generate relatively small amounts of revenue from applications they own, and at the same time must supply bandwidth for third party apps at prices their customers consider fair.

In that context, since most of the bandwidth consumed is video entertainment, and since video is the most bandwidth-intensive app, prices per bit must be low, and constantly get lower. Video economics are dominated by the fact that users will not pay very much for video entertainment, in relation to the bandwidth consumed to support its use.

For owned apps, revenue per bit for messaging and voice can be as much as two or more orders of magnitude higher than for full-motion video or Internet apps. By some estimates, where voice might earn 35 cents per megabyte, revenue per Internet app might generate a few cents per megabyte.

The cost of consuming a bit is infinitesimally small. Assume an internet access plan costing $50 a month, with a usage allowance of a terabyte. That, in turn, works out to a cost of about $0.000004 per byte. And even that cost will have to keep dropping.

The reason is that consumer propensity to pay is only so high. Essentially, internet service providers must continually supply more bandwidth for about the same prices.

source: GSMA Intelligence

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, April 1, 2021

Why T-Mobile has the Easier Route to Profitable 5G Revenue than AT&T or Verizon

In any market, attackers often have strategy options that incumbents do not have. In the 5G-related revenue growth areas, for example, incumbents are looking at internet of things, edge computing and private networks.

Attackers can choose to look elsewhere, as T-Mobile is doing in the areas of home broadband and business services. In the former market T-Mobile has zero market share, and only has to take a couple of share points to build a substantial new revenue stream. In the latter market, T-Mobile has been under-represented, compared to its two main rivals.

And it is almost always easier to take market share than to create brand new markets. To take share, an attacker does not have to guess about the market size, the value proposition, the distribution channels or pricing.

To create or enter a new market, a firm must make guesses about all those matters.

One of the issues for connectivity providers trying to create new revenue streams--aside from a reputation for not being good at innovation--is the challenge of finding innovations that represent enough incremental revenue to justify the cost of developing them.

It is one thing to see projections of the new revenue from private 5G networks; something else to figure out how much of that opportunity realistically can be addressed by connectivity providers.

We face the same problem when trying to estimate the value of edge computing or internet of things markets as well. How much of that opportunity realistically could be converted into revenue for connectivity providers?

Since estimates of edge computing, unified communications, IoT and private 5G always involve a mix of infrastructure sold to create the networks; management solutions of some type; design, installation and operating support and some connectivity revenues, the issue is how to estimate realistic connectivity service provider roles and therefore revenues.

History suggests connectivity providers might have a role earning up to five percent of any of those proposed new areas of business, based on past experience with local area networks in general, or business services such as enterprise voice, conferencing and collaboration.

The global unified communications and collaboration market might have reached about $47.2 billion in 2020, IDC says. But most of that revenue was earned by entities other than connectivity providers.

For example, revenue booked by Microsoft, Cisco, Zoom, Avaya and RingCentral totaled about $26 billion for the year. Those five firms represent 55 percent of total UCC revenues for the year, IDC figures suggest.

Relatively little UCC market revenue is earned by connectivity service providers.

Direct connectivity provider revenue from local area networks is almost completely related to broadband access bandwidth sold to enterprises, smaller businesses and consumers. Almost all the rest of the revenue is earned by hardware and software suppliers, third party design, installation and maintenance firms, chip and device vendors.

The point is that the traditional demarcation point between cabled public networks and private networks--wide area and local networks--happens at the side of a building or in the basement. WAN and connectivity service providers make their revenue.

The demarcation point between mobile customers and the public networks is the device. The capacity services supplier owns everything from spectrum to tower, then tower to switches and other controllers, then the core network. The consumer owns the phone.

Traditionally, the “private network” has been the province of different firms than public networks, which is why interconnect firms and system integrators or LAN specialists exist.

Even in some “core” WAN areas--including virtual private networks--third party specialists and infrastructure suppliers dominate the revenue production. Software-defined WANs, for example, can be created at the edge using gear owned by the enterprises who set up the SD-WANs.

SD-WANs can also be created by managed services firms, which includes connectivity providers. But most of the revenue is earned by infrastructure suppliers or managed services specialists, not connectivity providers.

Much the same can be said for internet of things revenue upside. Most of the revenue will be earned by LAN hardware and software suppliers, sensor and devices suppliers and app providers. WAN connectivity will be a contest between specialized WAN providers using unlicensed spectrum and mobile operators using licensed spectrum.

But all WAN connectivity collectively will be a small part of the IoT revenue opportunity.

In edge computing, most of the actual “computing” will be done by hyperscalers and others, even when mobile and fixed network operators supply real estate or access connections. It already seems clear that most telcos are not going to try and challenge hyperscalers for the actual “edge computing” function.

Private 5G is mostly going to create revenue for infrastructure sales (hardware and software), as private 5G or 4G are local area networks, like Wi-Fi. The enterprise or the consumer “owns” that network.

All of which raises an interesting question. “Everybody” seems to concur that businesses and enterprises will drive most of the incremental new revenue from 5G. What if that expectation is wrong? And it could be wrong, in the early days.

Consider private 5G or edge computing or IoT opportunities. How much enterprise or business revenue do you actually believe connectivity providers in any single country can generate, compared to any other initiative in consumer segments?

Consider fixed wireless, for example, in the U.S. market.

You can get a robust debate pretty quickly when asking “how important will 5G fixed wireless be?” in the consumer home broadband market. Will it matter?

Keep in mind that the fixed network home broadband market presently generates $195 billion worth of annual revenue. Comcast and Charter Communications alone book $150 billion annually from internet access services that largely are generated by home broadband customers.

Mobile service providers have close to zero--and in some cases actually zero--market share.

Taking just two percent means new revenues of perhaps $4 billion annually, within a couple of years. How long do you think it will take T-Mobile to earn that much money from IoT, edge computing or 5G private networks? T-Mobile’s effective answer is “too long,” as it is not pursuing those lines of businesses in an active sense.

T-Mobile is launching new initiatives for consumer home broadband and business mobility services, though.

And the growth path for T-Mobile is clear. Instead of supplying new customers, with new needs, with new products, T-Mobile in its home broadband push only has to take a few points of market share in an established market.

So it is possible that early incremental new revenue will be found by at least some mobile operators not in the sexy IoT, edge computing or private networks but in the less-sexy business of home broadband.

Not to mention profits. The cost of creating a $1 billion revenue stream in IoT, edge computing or private networks--within a few years--will be somewhat daunting. The cost of creating $4 billion in home broadband revenues in the same time frame might be a simpler matter of applying marketing effort.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, March 31, 2021

Algorithmic Bias and Algorithmic Choice

Some might agree that algorithmic choice is a reasonable way to deal with fake news or false information on social media sites. Algorithmic choice is inherent in sorting, ranking and targeting of content. To use a simple example, a search engine returning results for any user search has to rank order the items.

Algorithmic choice is essential for online and content businesses that try to tailor information for individuals based on their behavior or stated preferences. And most of us would likely agree that neutral curation, without obvious or intentional bias, is the preferred way of culling and then presenting information to users.

That is a growing issue for hyperscale social media firms, as they face mounting objections to the neutrality of their curation algorithms and practices. It is a delicate issue, to be sure. Decades ago, online sites operated with a loose "community standards" approach that relied on common courtesy and manners.

Today's hyperscale social media seems intentionally to stoke outrageous behavior and dissemination of arguably false or untrue information. Some refer to this as disinformation, the deliberate spreading of known-to-be-untrue facts, with the intention to deceive.

This is not the same thing as mere difference of opinion, the expression of “an idea I abhor” or “an idea I disagree with.” Disinformation is a matter of manipulation and deception. The latter is merely an expressed difference of opinion.

Some might argue that allowing more personalized control by users will help alleviate the problem of false or fake information. Perhaps that can help, somewhat, to the extent that people can block items and content they disagree with.

That does not address the broader problem of potential bias in the creation and application of algorithmic systems, including rules about what content infringes on community standards, is “untrue” or “misleading” or “false.”

It is akin to the odd notion of subjective "truth," as in "my truth" and "your truth." If something is objectively "true," my subjective opinion about it matters not.

In that sense, user-defined algorithms do not "solve" the problem of fake news and false information. The application of such algorithms by users only prevents them from exposure to ideas they do not prefer. It is not the same as designing search or culling mechanisms in a neutral and objective way, to the extent possible.

Less charitably, user algorithmic control is a way of evading responsibility for neutral curation by the application provider.

The bigger problem is that any algorithm has to be designed to filter out “truth” from “falsehood.” And that is a judgment call. “Ideas we all disagree with” is a form of bias that seems to be put to work deliberately by many social media.

Aside from the observation that “ideas” might best be determined to be more true or more false only when there is open and free debate about those ideas, algorithms are biased when certain ideas are deemed to be “false,” even when they clearly are matters of political, cultural, social, economic, scientific or moral and religious import where we all know people disagree.

And that means algorithm designers must make human judgments about what is “true” and what is “false.” It is an inherently biased process to the extent that algorithm designers are not aware of their own biases.

And that leads to banning the expression of ideas, not because they are forms of disinformation but simply because the ideas themselves are deemed "untrue" or "dangerous." The issue is that separating the "untrue" from the merely "different" involves choice.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Unified Communications Market Reaches $47 Billion, IDC Says

The global unified communications and collaboration market grew 29.2 percent year over year and 7.1 percent quarter over quarter to $13.1 billion in the fourth quarter of 2020, according to IDC. Revenue growth was also up 24.9 percent for the full year 2020 to $47.2 billion, IDC notes.

For the full year 2020, public cloud UCaaS revenue increased 21.2 percent to $16.4 billion.

Collaboration (including video conferencing software and cloud services) revenue increased 45 percent annually to reach $22.1 billion. In fact, for a market historically driven by business voice products (phone systems), revenue now is driven by conferencing.

Sales of IP phones declined 20.4 percent year over year, to about $1.9 billion, IDC reports.

Enterprise videoconferencing systems (such as video conference room endpoints) increased 12.4 percent to almost $2.6 billion.

The unified communications market always is difficult to explain, as it is a mix of many services and products, ranging from business phones to hosted communications services to enterprise hardware and software to access services such as SIP trunks.

For example, revenue booked by Microsoft, Cisco, Zoom, Avaya and RingCentral totaled about $26 billion for the year. Those five firms represent 55 percent of total UCC revenues for the year, IDC figures suggest.

Relatively little UCC market revenue is earned by connectivity service providers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...