Thursday, June 6, 2024

An 80-Year-Old Gift

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Wednesday, June 5, 2024

AI is Like the PC OS Business Model in Some Ways

In some key ways, the artificial intelligence business is developing in quite a different manner than did the internet, at least at the level of foundational models that might be likened to operating systems.

Or, to use another analogy, the large language model business stack is built on the actual LLMs. And there is a possible divergence between the internet, built largely on open source or marketplace standards including TCP/IP and Ethernet, and generative AI, built more on the model of the personal computer operating system platforms.

The internet's development--at the key application level--was largely driven by startups and entrepreneurs. GenAI is largely driven by a relatively small number of large and established firms, even if startups abound at the app layer.

Building internet apps and services often required less initial investment compared to GenAI, such as the cost to build and train an application’s generative AI capabilities and inferences.

Application user experience and scalability arguably were more important than access to capital, in part because capital was so abundant at that time and also because the ability to scale (users) was seen as key.

AI models are dependent on vast access to data; the internet apps were not. So as mechanisms develop to codify “fair use” and licensed access, more capital is going to be required for access to quality data sources.

There are other angles as well. The early internet was powered by private data centers of modest size. But AI is powered by “cloud computing” mechanisms.

By most estimates, about 65 percent of the capacity in global data centers is owned by just three companies: Amazon, Google, and Microsoft. That matters for artificial intelligence provided “as a service,” as much of the digital infrastructure required to support AI will be provided by the handful of hyperscale “computing as a service” suppliers.

And some might note that one value of investing in an AI startup are the agreements to use a particular cloud computing provider.

Startups get investment, but also agree to use the investing cloud computing giant’s infrastructure.

Also, some note that Google, Microsoft and Amazon are actively investing in hundreds of AI start-ups, as well. In 2023, Google, Microsoft and Amazon invested as much as two-thirds of the $27 billion for AI startups, a report argues.

Ignoring for the moment the matters of governance or competition in markets, there are possible systemic dangers related to firm revenue and profits. In the internet bubble at the turn of the century, for example, many firms exaggerated their revenues or capital bases using various forms of financial excess.

Internet capacity providers engaged in a practice called "capacity swapping." They bought and sold unused bandwidth from each other, artificially inflating their reported capacity and network reach. This created the illusion of high demand and fueled investor confidence. But it was an illusion. Actual end user demand was not as high as it seemed.

Many internet app startups relied heavily on vendor financing. Vendors would extend credit to these companies in exchange for stock options. This allowed startups to show reduced costs while vendors could report higher sales.

Some companies also resorted to creative accounting practices to inflate their revenue figures or provide growth metrics. Companies might record barter agreements, where they traded services or advertising space instead of receiving cash, as actual revenue. This inflated their top line without reflecting any real cash flow.

Some companies recognized revenue from multi-year contracts upfront, treating the entire value of the contract as income in the current year. This practice distorted their current financial health and overstated immediate profitability.

Companies might capitalize expenses related to marketing, website development or customer acquisition as assets instead of showing them as expenses. This artificially inflated reported profits.

Some companies recorded revenue for services even if the customer hadn't paid yet, again inflating reported revenues.

The point is that the AI business is developing in quite a different way than the internet. At least until the spigots shut off, there was plenty of investment capital available during the internet bubble. I recall being quite shocked when told by a startup’s founders not to worry about some parts of a business plan I was working on, as there was “plenty of money.”

AI is different, at the model or platform level. It is extremely capital intensive at a time when capital arguably is not plentiful or affordable. So barriers to entry are quite significant for model builders. In that sense, GenAI more nearly resembles the PC operating system model than the internet.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

The AI Business Stack

Most observers probably expect that artificial intelligence will produce some combination of new features for existing functions (image processing, speech to text, language translation, summarization, search, content creation, editing, shopping, research) as well some new use cases that could well produce entirely-new firms, industries and revenue streams.

It is logical that AI will be used to improve existing products such as Apple’s Siri or Google search, by making existing functions “smarter and faster.”

But entirely-new firms and industries are more likely to be built, one might argue, in a different way, using AI agents, which arguably are better at tasks where lots of unstructured data and relationships between data are involved.

To use an analogy, think of the difference between random access memory and sequential access memory. In the early days of the personal computer, that difference was between disk drives and tape drives.

Or think of programmed processors such as application-specific integrated circuits or field-programmable gate arrays, versus general-purpose central processing units.

In the pre-recorded music use case, think of tape drives versus compact discs or streaming delivery. While it is possible to pick a single song off a tape, there is substantial winding or rewinding time. With CD or streaming access, there is little to no navigation required, to say nothing of the “discovery of content” function.

Other similar analogies are possible. Think of live or pre-recorded linear television (broadcast or streamed) versus on-demand video, where one experience is scheduled and linear; the other built on-demand access allowing users to skip around a catalog to make choices.

The point is that AI agents might resemble general-purpose CPUS instead of ASICs; random access memory; on-demand audio or video: allowing unstructured operations using unstructured and structured data for unexpected tasks.

And since investors are so focused on AI opportunities, it might be helpful to liken various AI functions to the standard software “stack.”

Broadly speaking, investment opportunities will occur at every level of the AI stack.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, June 4, 2024

Where is the AI Edge?

Artificial intelligence processing “at the edge” most likely needs to be qualified, as most of the processing is likely to happen on devices such as smartphones and PCs. Mizuho analysts, for example, forecast one billion AI smartphones shipped from 2024 to 2027. Intel, for its part, expects to ship 40 million AI PC processors in 2024 alone.

Keep in mind that “AI capabilities” are going to be a feature of PCs and smartphones, rather than a distinct product category. Irrespective of the ultimate value of AI on such devices, we will be able to measure sales of products that are AI-capable, even if we might not easily be able to measure the incremental usefulness of AI on PCs and smartphones.

AI “as a service” revenues might be robust as well.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Use of Unstructured Data Might Give AI-Driven Financial Advice an Edge

The use of artificial intelligence to provide financial advice has far to go, at least partly for reasons of human trust in the quality of the advice. But there are some potential advantages for AI-generated algorithms that underpin the advice, when compared to current human-devised algorithms.

It is relatively hard for human algorithms to quantify and make sense of unstructured data. That should be increasingly possible for AI, which will have the advantage of many more data points. On the other hand, AI systems might not be as well-equipped as human advisors when it comes to factoring in human emotions (fear versus greed).

The same arguably holds true for unexpected events such as pandemics, wars or political upheavals. As a general rule, then, AI-generated advice might be more useful during times of relative market stability, while human decision-making might be more important at times of market turbulence.

On the other hand, since AI can process so many more sources of data, faster than the human algorithms, it is possible AI also could be better at detecting shifts of trend.

Also, to the extent that the AI algorithms can evolve organically over time, as the systems learn, AI could have an advantage over human-created algorithms that must be manually revised. For instance, “generally accepted accounting practices” and financial metrics of performance are relatively static measures.

AI can take advantage of social media sentiment, easy measurement of cars parked in company parking lots and other non-traditional indicators that are similar to “channel checks.”

The point is that we might ultimately be surprised at how much "advice" businesses and functions will eventually be displaced by AI mechanisms. Much expert advice is driven by rules of thumb; general rules and experience or precedent.

AI is going to be pretty good at summarizing and applying such knowledge or precedent for financial guidance. Algorithms already have been driving buy-sell actions in equtiy markets, for example.

In the same way, the ability to process unstructured data might give AI systems an edge over human advice, or at least become a required part of humans giving advice.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Home Broadband Prices have Fallen, But People Don't Believe It

Based on the Producer Price Index (PPI), both home broadband and mobile broadband prices

have fallen consistently since 2016, while prices for electricity, natural gas and postal services have climbed.

The opposite claim--that home broadband prices have risen sharply--often is asserted. So why does it seem as though prices have increased? Because people are buying different products than they once did.

So some might argue that the Consumer Price Index (CPI) is the better gauge of what consumers are spending, but since 2015 home broadband prices for speed tiers other than the slowest 10 Mbps downstream product have declined, with the biggest declines coming in the faster speed tiers that most consumers are buying.

All that noted, the reason the “home broadband prices have risen a lot” argument seems to resonate at times is that people are buying different products than they used to. Economists call changes in product quality “hedonic,” meaning that existing products can offer more value over time.

Hedonic change has been a major trend for electronics products for many decades.

Hedonic change refers to a shift in consumer preferences towards products with higher perceived quality, even if the core function of the product remains the same. The implication is that consumers are willing to pay more for these enhancements that bring greater satisfaction or enjoyment.

And that is why home broadband prices seem to be “rising” when they actually might be “falling.” Customers are substituting higher-value (and higher price) services for those they once purchased.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

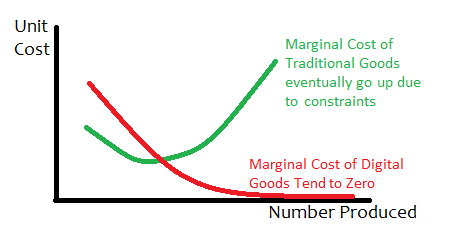

Near-Zero Marginal Cost for AI-Enabled Knowledge Goods?

Mustafa Suleyman, DeepMind cofounder and now Microsoft AI's CEO argues that, because of artificial intelligence, "the economics of ...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...