T-Mobile says it is on track to reach seven million to eight million fixed wireless accounts in 2025, and perhaps as many as 12 million by 2030.

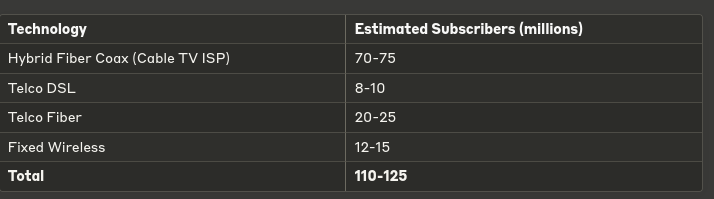

If there are about 110 million to 125 million U.S. home broadband accounts, that suggests T-Mobile alone--which had zero market share of the home broadband market until recently--already might claim five percent of the market.

we might estimate that cable TV internet service providers continue to hold the largest share, but with fixed wireless accounts growing substantially.

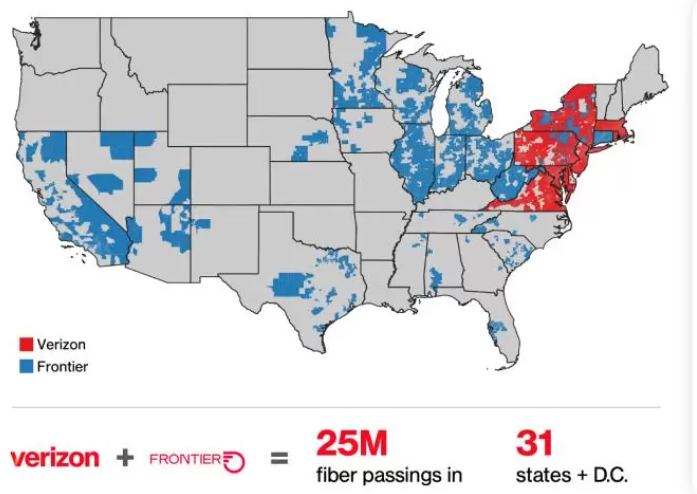

One of the odd realities of the U.S. internet access business is that--save for a recent Verizon statement, none of the big leaders of the internet access business actually ever says how many homes their networks pass. But Verizon recently noted that is passes 25 million homes.

My own past estimates have suggested, out of a total of 140 million U.S. homes (higher than figures some use), that AT&T’s landline network passed 62 million. Comcast had (can actually sell service to) about 57 million homes passed.

The Charter Communications network passed about 50 million homes, the number of potential customer locations it can sell to.

I had estimated Verizon homes passed might number 27 million, which is higher than the 25 million Verizon now says it passes.

Lumen Technologies never reports its “homes passed” figures, but likely has 20-million or so consumer locations.

Of course, if one uses the lower 110 million to 125 million figures, then T-Mobile’s share might be higher. It never is very clear whether reported “home broadband” figures include small business locations or not, but most such reports probably do include small business accounts.

My own past estimates have pegged U.S. homes in the 140 million range based on estimates by the U.S. Census Bureau. As a practical matter, at any given point in time millions of those locations are not part of the cabled home broadband market.

Some units are vacation homes are unoccupied most of the time. Other units are fully unoccupied and therefore not candidates for home broadband services. Some units are boats, trailers or other locations not easy or possible to serve using cabled networks.

Also, some units are so remote it is economically unfeasible to reach them by a cabled network at all. That might be up to two percent of all U.S. homes.

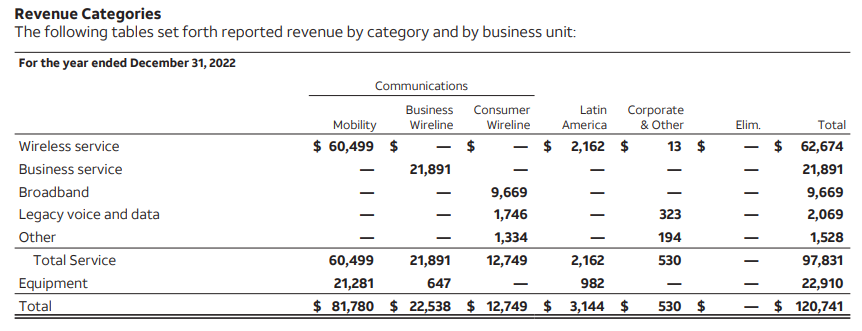

AT&T, for example, reports revenues for mobility, fixed network business revenues and consumer fixed network revenues from internet access, voice and other sources. But those are traditional financial metrics, not operating indices such as penetration or take rates, churn rates and new account gains.

Nobody seemingly believes the same effort should be made to measure the number of home broadband provider locations or dwellings reached by various networks. Better mapping, yes. Metrics on locations passed? No.

And yet “locations passed” is a basic and essential input to accurately determine take rates (percent of potential customers who actually buy). That input matters quite a lot to observers when evaluating the growth prospects of competitors, even if that figure does not matter much for policymakers, who mainly care about the total degree of home broadband take rates, on an aggregate basis.

The U.S. Census Bureau, for example, reported some 140.5 million housing units housing units as part of the 2020 census. The estimate for 2021 units is 142.2 million units. Assume 1.5 million additional units added each year, for a 2022 total of about 143.6 million dwelling units.

Assume vacancy rates of about six percent. That implies about 8.6 million unoccupied units that would not be assumed to be candidates for active home broadband subscriptions. The U.S. Census Bureau, though, estimates there are about 11 million unoccupied units when looking at full-time occupied status. That figure presumably includes vacation homes.

Deducting the unoccupied dwellings gives us a potential home broadband buyer base of about 132.6 million locations.

That has implications for the theoretical maximum market share any of the leading providers might claim. Depending on one’s choice of the base of addressable homes, and keeping in mind there is overlap between at least one of the cable and one of the telco providers in virtually every territory, Comcast and AT&T are best positioned to lead share statistics, in some future market where skill and resources are full deployed (telcos have largely built or acquired fiber-to-home facilities, for example), simply because their networks pass the most homes.

That does not speak to actual market shares; only potential share were any particular provider to take 100 percent share of the market within its cabled network footprint.

T-Mobile’s initial foray into cabled networks is important, in that regard, but the potential share stats will not be significant for quite some time, given the small number of homes T-Mobile cabled networks could reach.

For T-Mobile, fixed wireless is the key to its home broadband share gains. Fixed wireless remains important for Verizon Fixed wireless might become important for AT&T.

The point is that only AT&T has potential to take significant share in the overall home broadband market, based on its extensive homes passed footprint. Only Comcast and Charter are in the same league. Verizon and Lumen, no matter how well they do in their regions, do not pass a similar number of U.S. homes.

In principle, T-Mobile gains will be limited by its use of fixed wireless as the primary platform, as that platform appeals to the value portion of the market, for the most part (customers purchasing service at speeds no higher than 200 Mbps).

Right now, that means T-Mobile’s fixed wireless service, itself limited by T-Mobile only to regions where it has excess capacity, is not available to the up-to-20-percent of the U.S. home broadband market. The T-Mobile addressable market is “homes content with access speeds no higher than 200 Mbps” and further reduced by T-Mobile’s own unwillingness to offer fixed wireless home broadband “everywhere.”

T-Mobile and Verizon should continue to take market share for some time. Eventually, though, the market segment most attracted to fixed wireless will saturate, leaving the bulk of competition to the cable HFC and telco FTTH facilities.

In principle, fixed wireless speeds can grow over time, as more spectrum is made available or network architectures move to smaller cells, but there remain physical limits to either of those strategies, especially since the key revenue driver remains mobile device service.