Over 38 million handheld gaming devices from Sony and Nintendo are expected to ship in 2013, a maximum that is significantly lower than the previous peak of 47 million units in 2008, according to ABI Research.

That is one sign that casual gaming has shifted to smart phones and now tablets, and away from dedicated mobile game consoles.

Unit shipments following 2013 are expected to decline slightly, but dedicated handheld gaming devices are a sustainable niche, ABI Research argues, with forecasts relatively flat through 2017.

Monday, June 11, 2012

Handheld Gaming Devices in Downward Spiral Because of Smart Phones, Tablets

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Do Mobile Data Plans Reflect or Shape Usage?

What is the relationship between the structure of a data plan and usage? Do people adapt behavior to the plans, or does the choice of a data plan reflect existing behavior? It’s a harder question than might first appear, as several processes likely are at work.

Over time, people tend to consume more data. Use of video-based applications is growing. But virtually all studies show that, even in instances where bandwidth usage actually is “unlimited,” or so generous that no typical user ever approaches a limit, only a small percentage of users actually push the limits.

It is an unquestioned fact that a small percentage of broadband users, on virtually any network, use vastly more data than typical users do. The top one percent of data consumers account for 20 percent of the overall consumption, for example, a fact the study by Benoît Felten, Yankee Group analyst, confirms.

But users also seem to be able to adjust their behavior and expectations. When bandwidth usage carries direct financial implications, people adjust by changing their behavior, switching their smart phones to Wi-Fi access when at home, for example.

Also, data from Ericsson suggests a bit of both processes might be at work. It appears that, over time, virtually all users consume more bandwidth.

But “typical usage” remains a far different issue from “average” usage. Even as overall usage grows, a small percentage of very-heavy users represents a disproportionate amount of usage. In that sense, choice of data plans follows behavior. Heavier users will seek the biggest plans. Lighter users will choose plans with less capacity, when available.

On the other hand, usage patterns are also related to the data plan that comes with a device. That is significant because it suggests people actually modify their behavior based on plan policies. In other words, the Ericsson study suggests, people use more when their plan allows it.

If so, service providers have a wide range of options for shaping end user demand, using price and other packaging mechanisms. Generally speaking, people use more data when they buy bigger buckets of usage.

But it is a nuanced matter. It can’t be precisely determined whether people use more data because they have bigger plans, or have bigger plans because they use more data over time.

Also, since new devices aside from phones tend to get used over time (notebooks and tablets), and since usage profiles for those other devices are different from phones, consumer usage and shaping of retail plans also will tend to change over time.

On the other hand, one might argue, given any set range of plans, users will virtually always fall into a distribution that is stable and predictable.

“Nearly all communications traffic, including Internet traffic, can be approximated with high accuracy by the log-normal distribution,” says Phoenix Center Chief Economist Dr. George S. Ford. That’s important, as it means we generally can predict overall end user behavior when we actually know only a couple of key data points.

Among the practical implications are estimates of what is likely to happen when a broadband service provider imposes a monthly usage cap of 250 gigabytes. The log-normal distribution suggests how many customers would hit the limit.

The log-normal distribution also generally allows some estimation of how consumption will vary across the entire customer base, knowing only the consumption of the top one percent, and the consumption of the top 10 percent of users, an analysis by Dr. Ford suggests.

The point is that “averages” (the arithmetic mean) don’t tell an observer very much when any service has an asymmetric distribution, as always seems to be the case for Internet consumption by consumers.

Cisco’s Visual Networking Index reports that the top one percent of users accounted for more than 20 percent of Internet traffic and that the top 10 percent of users accounted for 60 percent

of traffic.

That means a Pareto distribution, which would ideally show that 20 percent of instances account for 80 percent of the impact would also likely hold.

Ford notes that Comcast’s 250 GByte per month usage cap on its residential broadband

customers, taken with Comcast’s own statements that 99 percent of its residential customers will not approach that cap suggests that only one percent of Comcast’s residential users consume 250 GBytes per month or more.

Comcast also indicated that its median customer consumes about 8 GBytes to 10 GBytes per month.

The log-normal distribution could well inform many other sorts of policies, such as what amount of consumption a “typical” user requires.

“My approach to approximating usage patterns may be useful for variety of policy issues,” says Ford. “ For example, when addressing universal service for broadband, the level of service that qualifies as ‘broadband’ will have to be parameterized.”

Knowledge of the usage distribution may aid in establishing these service level definitions that can be described as “reasonably comparable to those services provided in urban areas, for example.

The relationship between “typical” usage and “heavy” usage seems to be internally consistent, no matter what the “heavy” consumption levels might be.

Over time, people tend to consume more data. Use of video-based applications is growing. But virtually all studies show that, even in instances where bandwidth usage actually is “unlimited,” or so generous that no typical user ever approaches a limit, only a small percentage of users actually push the limits.

It is an unquestioned fact that a small percentage of broadband users, on virtually any network, use vastly more data than typical users do. The top one percent of data consumers account for 20 percent of the overall consumption, for example, a fact the study by Benoît Felten, Yankee Group analyst, confirms.

But users also seem to be able to adjust their behavior and expectations. When bandwidth usage carries direct financial implications, people adjust by changing their behavior, switching their smart phones to Wi-Fi access when at home, for example.

Also, data from Ericsson suggests a bit of both processes might be at work. It appears that, over time, virtually all users consume more bandwidth.

But “typical usage” remains a far different issue from “average” usage. Even as overall usage grows, a small percentage of very-heavy users represents a disproportionate amount of usage. In that sense, choice of data plans follows behavior. Heavier users will seek the biggest plans. Lighter users will choose plans with less capacity, when available.

On the other hand, usage patterns are also related to the data plan that comes with a device. That is significant because it suggests people actually modify their behavior based on plan policies. In other words, the Ericsson study suggests, people use more when their plan allows it.

If so, service providers have a wide range of options for shaping end user demand, using price and other packaging mechanisms. Generally speaking, people use more data when they buy bigger buckets of usage.

But it is a nuanced matter. It can’t be precisely determined whether people use more data because they have bigger plans, or have bigger plans because they use more data over time.

Also, since new devices aside from phones tend to get used over time (notebooks and tablets), and since usage profiles for those other devices are different from phones, consumer usage and shaping of retail plans also will tend to change over time.

On the other hand, one might argue, given any set range of plans, users will virtually always fall into a distribution that is stable and predictable.

“Nearly all communications traffic, including Internet traffic, can be approximated with high accuracy by the log-normal distribution,” says Phoenix Center Chief Economist Dr. George S. Ford. That’s important, as it means we generally can predict overall end user behavior when we actually know only a couple of key data points.

Among the practical implications are estimates of what is likely to happen when a broadband service provider imposes a monthly usage cap of 250 gigabytes. The log-normal distribution suggests how many customers would hit the limit.

The log-normal distribution also generally allows some estimation of how consumption will vary across the entire customer base, knowing only the consumption of the top one percent, and the consumption of the top 10 percent of users, an analysis by Dr. Ford suggests.

The point is that “averages” (the arithmetic mean) don’t tell an observer very much when any service has an asymmetric distribution, as always seems to be the case for Internet consumption by consumers.

Cisco’s Visual Networking Index reports that the top one percent of users accounted for more than 20 percent of Internet traffic and that the top 10 percent of users accounted for 60 percent

of traffic.

That means a Pareto distribution, which would ideally show that 20 percent of instances account for 80 percent of the impact would also likely hold.

Ford notes that Comcast’s 250 GByte per month usage cap on its residential broadband

customers, taken with Comcast’s own statements that 99 percent of its residential customers will not approach that cap suggests that only one percent of Comcast’s residential users consume 250 GBytes per month or more.

Comcast also indicated that its median customer consumes about 8 GBytes to 10 GBytes per month.

The log-normal distribution could well inform many other sorts of policies, such as what amount of consumption a “typical” user requires.

“My approach to approximating usage patterns may be useful for variety of policy issues,” says Ford. “ For example, when addressing universal service for broadband, the level of service that qualifies as ‘broadband’ will have to be parameterized.”

Knowledge of the usage distribution may aid in establishing these service level definitions that can be described as “reasonably comparable to those services provided in urban areas, for example.

The relationship between “typical” usage and “heavy” usage seems to be internally consistent, no matter what the “heavy” consumption levels might be.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Answer, Send to Voicemail, Reply with Message, Remind me to Call Back Later

Apple's latest operating system roughly doubles the typical inbound call handling options most people will use, especially for those of you who, for any reason, think call waiting is not something to be used.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple has 400 Million Payment Accounts

Apple now has 400 million active payment accounts, according to Apple CEO Tim Cook. That doesn't necessarily mean Apple is interested, at the moment, in doing much beyond supporting content payments on its own devices.

Apple now has 400 million active payment accounts, according to Apple CEO Tim Cook. That doesn't necessarily mean Apple is interested, at the moment, in doing much beyond supporting content payments on its own devices.But all of those 400 million active accounts have active credit cards that can be used on iTunes and the App Store.

PayPal has 110 million active accounts and Amazon.com has 152 million customer accounts.

At least for the moment, Apple seems content to use its payment system in a closed-loop way, as does Starbucks.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple's iOS 6 Will Launch Apps on iPads

Apple's iOS 6 mobile operating system will be made available on iPads, and will include the ability to its launch apps, Apple says. Siri now also answers real-world questions about sports, movies and restaurants.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

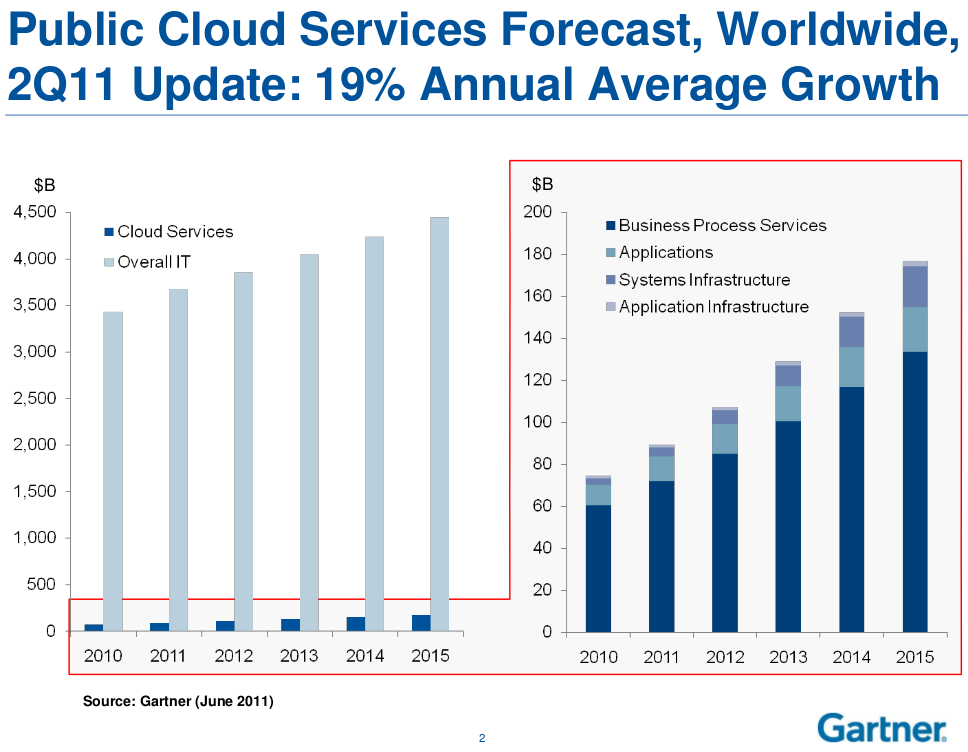

What Does it Mean that "Cloud Computing" is Growing 28% a Year?

Cloud computing was the fastest-growing category of U.S. service provider infrastructure spending in 2011, with a 28.4 percent increase, according to the Telecommunications Industry Association.

The TIA also expects cloud computing will continue to be the fastest-growing category of network and facilities investment during the next four years, averaging 20.3 percent compounded annually.

But it is end user spending that arguably drives most of the revenue, so one might argue that much of the opportunity will be reaped by firms that sell enterprise applications, not firms that sell infrastructure services more centrally related to hosting, for example.

TIA argues that end user spending on cloud apps will more than double to $12.1 billion in 2015 from $5.8 billion in 2011, according to the TIA. Separating out what that could mean for providers of cloud “data center facilities” is harder to assess.

In fact, most of the revenue upside appears likely to accrue to hardware and software suppliers, at least initially, according to a Morgan Stanley analysis.

In the infrastructure end of the business, telecom service providers might make a business out of rental of computing cycles, storage and ancillary services. But what has to be done to market and support that business, and should effort be put elsewhere?

In the telecom space, the analysts expect key winners to include Rackspace, Equinix and competitive local exchange carriers and metro bandwidth suppliers. In other words, hosting and access will be where the telecom revenue lies, possibly not in the infrastructure, platform or software as a service businesses.

The point is that assessing cloud computing revenue contributions for various ecosystem participants is complicated.

That forecast suggests why cloud computing initiatives by telcos will have to be targeted. There actually isn’t as much revenue in cloud computing as some tend to think. Nor is the space uncontested.

Companies such as Google, Amazon Web Services, Hewlett-Packard Development Co., Microsoft Corp. and Salesforce.com are themselves already leaders in the cloud infrastructure space, and already are displacing traditional infrastructure outsourcing alternatives, one might argue.

North America, specifically the U.S., currently represents the largest opportunity for SaaS, and it is the most mature of the regional markets. SaaS software revenue is forecast to total $9.1 billion in 2012, up from $7.8 billion in 2011.

But keep in mind that most of that revenue is earned providing expense management, financials, email and office suites. Though Web conferencing also is a SaaS application, few telcos are players to any major extent.

In Western Europe, SaaS revenue is forecast to surpass $3.2 billion in 2012, up from $2.7 billion in 2011, while SaaS revenue is Eastern Europe is projected to reach $169.4 million, up from $135.5 million last year.

SaaS revenue in Asia/Pacific is on pace to reach $934.1 million in 2012, up from $730.9 million in 2011.

SaaS revenue in Latin America is forecast to total $419.7 million in 2012, up from $331.1 million last year. None of those revenue streams are terribly large, by tier one service provider standards, nor are telcos the most logical providers.

In addition to the possibility that cloud-delivered enterprise apps compete most centrally with distributors of "shrink wrapped" apps, it can be argued that cloud infrastructure also competes with traditional "outsourcing" services.

Cloud infrastructure services are an alternative to traditional IT outsourcing services, often reducing the IT costs of their clients by at least 40 percent, according to livemint.com.

Likewise, you might argue that enterprise or other "app stores" might also compete with other software delivery channels.

What you will note about the enterprise app store concept is that it disintermediates nearly all of the premises networking infrastructure. There is no need for the enterprise local area network, except perhaps to switch to Wi-Fi access at times.

You can imagine this will have serious implications for firms that traditionally make a living selling gear and services for enterprise LANs. Just as easily, you can see the upside for traditional communications providers who now could have an expanded role in the information technology business.

What products would be “natural” parts of a communications and information technology bundle? How much easier would it be for traditional telco sales organizations to sell key business software?

In fact, non-technical sales forces of all types might find there are new opportunities to sell products that might have been “too technical” in the past. Firms outside “IT” might find they can create bundles almost on the fly, customized for vertical markets or businesses of various sizes and types.

A shift to some new computing architecture based on cloud resources and mobility could have huge implications for any number of businesses in the information technology and communications businesses.

Although growing interest has been observed in vertical-specific software, the most widespread use is still characterized by horizontal applications with common processes, among distributed virtual workforces and within Web 2.0 activities.

Cloud computing will have implications for most firms in the business applications, information technology support and data center businesses. Whether that impact is large or relatively small is hard to say, at the moment.

The TIA also expects cloud computing will continue to be the fastest-growing category of network and facilities investment during the next four years, averaging 20.3 percent compounded annually.

But it is end user spending that arguably drives most of the revenue, so one might argue that much of the opportunity will be reaped by firms that sell enterprise applications, not firms that sell infrastructure services more centrally related to hosting, for example.

TIA argues that end user spending on cloud apps will more than double to $12.1 billion in 2015 from $5.8 billion in 2011, according to the TIA. Separating out what that could mean for providers of cloud “data center facilities” is harder to assess.

In fact, most of the revenue upside appears likely to accrue to hardware and software suppliers, at least initially, according to a Morgan Stanley analysis.

In the infrastructure end of the business, telecom service providers might make a business out of rental of computing cycles, storage and ancillary services. But what has to be done to market and support that business, and should effort be put elsewhere?

In the telecom space, the analysts expect key winners to include Rackspace, Equinix and competitive local exchange carriers and metro bandwidth suppliers. In other words, hosting and access will be where the telecom revenue lies, possibly not in the infrastructure, platform or software as a service businesses.

The point is that assessing cloud computing revenue contributions for various ecosystem participants is complicated.

That forecast suggests why cloud computing initiatives by telcos will have to be targeted. There actually isn’t as much revenue in cloud computing as some tend to think. Nor is the space uncontested.

Companies such as Google, Amazon Web Services, Hewlett-Packard Development Co., Microsoft Corp. and Salesforce.com are themselves already leaders in the cloud infrastructure space, and already are displacing traditional infrastructure outsourcing alternatives, one might argue.

North America, specifically the U.S., currently represents the largest opportunity for SaaS, and it is the most mature of the regional markets. SaaS software revenue is forecast to total $9.1 billion in 2012, up from $7.8 billion in 2011.

But keep in mind that most of that revenue is earned providing expense management, financials, email and office suites. Though Web conferencing also is a SaaS application, few telcos are players to any major extent.

In Western Europe, SaaS revenue is forecast to surpass $3.2 billion in 2012, up from $2.7 billion in 2011, while SaaS revenue is Eastern Europe is projected to reach $169.4 million, up from $135.5 million last year.

SaaS revenue in Asia/Pacific is on pace to reach $934.1 million in 2012, up from $730.9 million in 2011.

SaaS revenue in Latin America is forecast to total $419.7 million in 2012, up from $331.1 million last year. None of those revenue streams are terribly large, by tier one service provider standards, nor are telcos the most logical providers.

In addition to the possibility that cloud-delivered enterprise apps compete most centrally with distributors of "shrink wrapped" apps, it can be argued that cloud infrastructure also competes with traditional "outsourcing" services.

Cloud infrastructure services are an alternative to traditional IT outsourcing services, often reducing the IT costs of their clients by at least 40 percent, according to livemint.com.

Likewise, you might argue that enterprise or other "app stores" might also compete with other software delivery channels.

What you will note about the enterprise app store concept is that it disintermediates nearly all of the premises networking infrastructure. There is no need for the enterprise local area network, except perhaps to switch to Wi-Fi access at times.

You can imagine this will have serious implications for firms that traditionally make a living selling gear and services for enterprise LANs. Just as easily, you can see the upside for traditional communications providers who now could have an expanded role in the information technology business.

What products would be “natural” parts of a communications and information technology bundle? How much easier would it be for traditional telco sales organizations to sell key business software?

In fact, non-technical sales forces of all types might find there are new opportunities to sell products that might have been “too technical” in the past. Firms outside “IT” might find they can create bundles almost on the fly, customized for vertical markets or businesses of various sizes and types.

A shift to some new computing architecture based on cloud resources and mobility could have huge implications for any number of businesses in the information technology and communications businesses.

Although growing interest has been observed in vertical-specific software, the most widespread use is still characterized by horizontal applications with common processes, among distributed virtual workforces and within Web 2.0 activities.

Cloud computing will have implications for most firms in the business applications, information technology support and data center businesses. Whether that impact is large or relatively small is hard to say, at the moment.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Africa Mobile Market Fastest Growing in World

If you can remember 1970s and 1980s policy discussions in the global telecom community about how to provide basic telephone service to the billion or more people who had never made a phone call, you will be astonished at how powerful mobile services have been. A problem thought too expensive to solve now is well on the way to vanishing.

Africa, for example, is the fastest-growing mobile market in the world and the largest after Asia, according to the GSM Association.

The number of subscribers on the continent has grown almost 20% each year for the past five years, according to the GSM Association GSMA report on the African mobile market. The GSMA expects there will be more than 735 million subscribers by the end of 2012.

Among the changes mobility is bringing is a new access to banking services. Africa already has 51 mobile money systems in place, serving more than 40 million African users.

Africa, for example, is the fastest-growing mobile market in the world and the largest after Asia, according to the GSM Association.

The number of subscribers on the continent has grown almost 20% each year for the past five years, according to the GSM Association GSMA report on the African mobile market. The GSMA expects there will be more than 735 million subscribers by the end of 2012.

Among the changes mobility is bringing is a new access to banking services. Africa already has 51 mobile money systems in place, serving more than 40 million African users.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...