Wednesday, August 22, 2012

Are Millennials Really Different?

Millennials, people between the ages 18 to 29 or so (some would include people up into the mid-30s), are "different," many would argue.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Nearly Half of US Consumers Think They Don't Need LTE

About 47 percent of consumers polled by Piper Jaffray say they "don't need 4G Long Term Evolution," and another 26 percent think all 4G network technologies are the same.

About 15 percent of those polled said that 4G LTE is the best network technology, the survey by Pipe Jaffray suggests.

The findings should not be surprising. One could have gotten similar results about third generation services for quite a long time in markets such as Western Europe, or the United States, as well.

That is hardly unusual. Even though China reached a milestone in February 2012 when the number of mobile phone users in the country surpassed one billion, representing penetration of 74 percent, the 3G penetration rate is still low at 14 percent, for example, China Daily reported.

The total number of 3G subscribers in India is just about 2% of the total number of cellphone users. India has 893.8 million cellphone users according to the Telecom Regulatory Authority of India, (TRAI).

A 2006 study of 3G adoption in Western Europe, at a time when nearly 90 percent of 3G license holders in six Western European markets had launched 3G services three years prior, 3G penetration rates were still generally low, ranging from one percent to 12 percent, with a median of about 3.5 percent adoption.

The big problem was "lack of 3G content and applications." That should be qualitatively different with 4G, as it is the Internet that generally will supply content and applications. But will it be any different in the early going?

Piper Jaffray's survey also found that consumers are ambivalent about which U.S. carrier has the best 4G LTE network. Among those polled, 51 percent indicated they don't know who has the best 4G network, or that all 4G networks are the same.

That finding should not be surprising, either. Few consumers likely have a good grasp of the differences, or have had a chance to test and use most of the services for a length of time.

About 15 percent of those polled said that 4G LTE is the best network technology, the survey by Pipe Jaffray suggests.

The findings should not be surprising. One could have gotten similar results about third generation services for quite a long time in markets such as Western Europe, or the United States, as well.

That is hardly unusual. Even though China reached a milestone in February 2012 when the number of mobile phone users in the country surpassed one billion, representing penetration of 74 percent, the 3G penetration rate is still low at 14 percent, for example, China Daily reported.

The total number of 3G subscribers in India is just about 2% of the total number of cellphone users. India has 893.8 million cellphone users according to the Telecom Regulatory Authority of India, (TRAI).

A 2006 study of 3G adoption in Western Europe, at a time when nearly 90 percent of 3G license holders in six Western European markets had launched 3G services three years prior, 3G penetration rates were still generally low, ranging from one percent to 12 percent, with a median of about 3.5 percent adoption.

The big problem was "lack of 3G content and applications." That should be qualitatively different with 4G, as it is the Internet that generally will supply content and applications. But will it be any different in the early going?

Piper Jaffray's survey also found that consumers are ambivalent about which U.S. carrier has the best 4G LTE network. Among those polled, 51 percent indicated they don't know who has the best 4G network, or that all 4G networks are the same.

That finding should not be surprising, either. Few consumers likely have a good grasp of the differences, or have had a chance to test and use most of the services for a length of time.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

As Tablet Sales Reach 400 Million Units in 2016, Will Apple iPad Keep Lead?

When one includes Android and other tablets as well as e-readers, nearly 100 million tablets were sold in 2011. But 400 million units will be sold by 2016, Business Insider predicts, 400 times the number sold in 2011.

Through the first six months of the year, tablet prices have seen a pretty steep drop off, despite the iPad's continued dominance. The average selling price of the iPad is down more than 11 percent from its 2011 price. The introduction of mini tablets, beginning with the Kindle Fire, disrupted the pricing dynamics of the market and will drive the huge drop in ASP over the next few years, BI says.

Tablets are poor substitute for PCs if you are trying to run data intensive spreadsheets, but they vastly improve upon the media consumption experience, BI says. That is one reason some argue that tablets are a new product category of computing device, not a "replacement" for PCs, as such. As it turns out, what people want to do on computing appliances has changed over the last couple of decades. They work less, they consume media more.

Through the first six months of the year, tablet prices have seen a pretty steep drop off, despite the iPad's continued dominance. The average selling price of the iPad is down more than 11 percent from its 2011 price. The introduction of mini tablets, beginning with the Kindle Fire, disrupted the pricing dynamics of the market and will drive the huge drop in ASP over the next few years, BI says.

Tablets are poor substitute for PCs if you are trying to run data intensive spreadsheets, but they vastly improve upon the media consumption experience, BI says. That is one reason some argue that tablets are a new product category of computing device, not a "replacement" for PCs, as such. As it turns out, what people want to do on computing appliances has changed over the last couple of decades. They work less, they consume media more.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

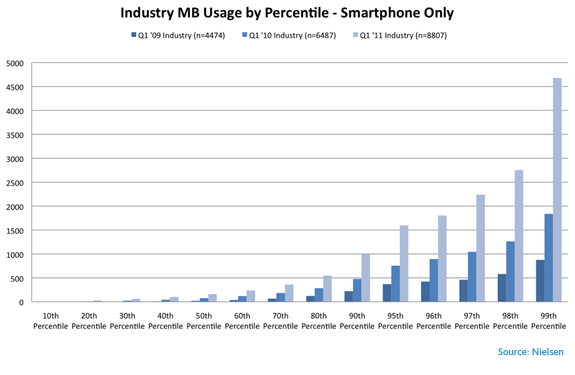

How Big is the Difference Between “Unlimited” and “Enough?”

Withim a single day on Aug. 21, 2012, MetroPCS and T-Mobile USA did what underdog firms often do, namely shake up retail pricing in an attempt to reverse flagging sales or market share.

Withim a single day on Aug. 21, 2012, MetroPCS and T-Mobile USA did what underdog firms often do, namely shake up retail pricing in an attempt to reverse flagging sales or market share. In this case, both firms announced “unlimited” data plans for smart phones.Those moves come against an industry backdrop of movement away from unlimited, flat rate data plans that threaten to erode profit margins as well as limit gross revenue opportunities.

There are a few fundamental questions one might ask. First, are such plans sustainable, by these two contestants (which is a different question than whether unlimited plans are sustainable by other competitors).

Also, related to that question, is the issue of whether the new offers will change the cost structure of T-Mobile USA and MetroPCS in some qualitative way, for better or worse.

Granted, usage tends to grow, over time. But a June 2011 Nielsen monthly analysis of cell phone bills for 65,000 lines, though showing smart phone owners, especially those with iPhones and Android devices, are consuming more data than ever before on a per-user basis, the amounts are not so huge.

The amount of data the average smart phone user consumes per month has grown by 89 percent from 230 megabytes in the first quartrer of 2010 to 435 MBytes in the first quarter of 2011.

Separately, T-Mobile USA executives have noted 2012 consumption of 1.3 Mbytes a month by 4G network users. More typical users, not the “power” users, consume something on the order of 760 Mbytes a month.

In the United Kingdom, U.K. service provider Three has reported that its users have more than doubled how much mobile data they consume every month in less than a year.

The “average user” now consumes 1.1 Gbytes,, compared to 450 Mbytes in the summer of 2011.

As always “average” in the sense of “arithmetic mean” is misleading. According to U.K. service provider O2, though average consumption is 200 Mbytes a month, 0.1 percent of users consume more than 800 Mbytes a month, while 97 percent of users consume less than 500 Mbytes a month.

The point is that, for most consumers, the difference between an “unlimited” plan and a plan offering 2 Mbytes to 5 Mbytes is virtually zero, in terms of potential value. Most people just won’t use all that much data, no matter what plan they are on.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

The point is that, for most consumers, the difference between an “unlimited” plan and a plan offering 2 Mbytes to 5 Mbytes is virtually zero, in terms of potential value. Most people just won’t use all that much data, no matter what plan they are on.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple FaceTime Does Raise Issues, Just not "Net Neutrality"

Apple's FaceTime, and the charges some AT&T users might incur to use it, raises issues, but not of "network neutrality." AT&T has offered a "narrow" defense based on technical rules related to network neutrality.

Others might raise broader issues. Network neutrality rules, you will recall, codify the Federal Communications Commission's Internet freedom principles that dictate users have the right to use all lawful Internet apps, among other assurances.

Keep in mind that Apple's FaceTime app has generally been restricted to Wi-Fi use, in large part because of the amount of mobile network bandwidth the app consumes. As with the matter of "freedom of speech," the existence of some time, place and manner of use restrictions do not infringe the freedom being protected.

AT&T defends its new policy granting unlimited use of FaceTime on some of its mobile data plans, and not others, on the narrow grounds of compliance with the language of the FCC's network neutrality rules, namely that service providers may not lawfully block apps that compete with existing service provider offerings.

You might argue that a good lawyer will use the narrowest possible argument that clearly advances a particular line of legal reasoning, rather than a larger, more philosophical argument that embraces more aspects. AT&T logically uses a narrow construction based on the language of the FCC rules

Some of us would argue AT&T also has a larger argument. There have been, and can be, time, place and manner restrictions of several sorts on bandwidth-intensive apps that could degrade user experience for all other users. In the voice world, we are accustomed to outright blocking. That's what happens when a caller gets a "please try your call again later, all circuits are busy" recording when trying to place a phone call.

That's what happens when Twitter servers become overloaded. You see the "fail whale" and you can't use Twitter. In principle, the FCC bars deliberate blocking of lawful apps. The FCC does not prohibit or punish "over capacity" blockages that occur when servers get overloaded.

Nor do the FCC rules prescribe the business logic contestants might employ when selling various device features. Personal hotspot features are "blocked" on most networks unless a user pays a separate fee to enable such use.

In other words, network neutrality rules exist primarily to prohibit anti-competitive behavior, and not to prescribe the ways service providers decide to package and price features and capabilities. By definition, every service provider marketing policy can affect competition, in an open and transparent way. That is not something "network neutrality" even tries to prevent.

Any AT&T user can use Apple FaceTime on any Wi-Fi connection without incurring any additional charges. On some mobile data plans, the mobile network can be used. On some plans FaceTime cannot be used on the mobile network. The use of FaceTime is not "blocked."

But the manner of use is differential. Other suppliers can make different choices. None of the choices, except a complete inability to use FaceTime ("blocking" as a policy) are a net neutrality infraction, in a broad sense.

Others might raise broader issues. Network neutrality rules, you will recall, codify the Federal Communications Commission's Internet freedom principles that dictate users have the right to use all lawful Internet apps, among other assurances.

Keep in mind that Apple's FaceTime app has generally been restricted to Wi-Fi use, in large part because of the amount of mobile network bandwidth the app consumes. As with the matter of "freedom of speech," the existence of some time, place and manner of use restrictions do not infringe the freedom being protected.

AT&T defends its new policy granting unlimited use of FaceTime on some of its mobile data plans, and not others, on the narrow grounds of compliance with the language of the FCC's network neutrality rules, namely that service providers may not lawfully block apps that compete with existing service provider offerings.

You might argue that a good lawyer will use the narrowest possible argument that clearly advances a particular line of legal reasoning, rather than a larger, more philosophical argument that embraces more aspects. AT&T logically uses a narrow construction based on the language of the FCC rules

Some of us would argue AT&T also has a larger argument. There have been, and can be, time, place and manner restrictions of several sorts on bandwidth-intensive apps that could degrade user experience for all other users. In the voice world, we are accustomed to outright blocking. That's what happens when a caller gets a "please try your call again later, all circuits are busy" recording when trying to place a phone call.

That's what happens when Twitter servers become overloaded. You see the "fail whale" and you can't use Twitter. In principle, the FCC bars deliberate blocking of lawful apps. The FCC does not prohibit or punish "over capacity" blockages that occur when servers get overloaded.

Nor do the FCC rules prescribe the business logic contestants might employ when selling various device features. Personal hotspot features are "blocked" on most networks unless a user pays a separate fee to enable such use.

In other words, network neutrality rules exist primarily to prohibit anti-competitive behavior, and not to prescribe the ways service providers decide to package and price features and capabilities. By definition, every service provider marketing policy can affect competition, in an open and transparent way. That is not something "network neutrality" even tries to prevent.

Any AT&T user can use Apple FaceTime on any Wi-Fi connection without incurring any additional charges. On some mobile data plans, the mobile network can be used. On some plans FaceTime cannot be used on the mobile network. The use of FaceTime is not "blocked."

But the manner of use is differential. Other suppliers can make different choices. None of the choices, except a complete inability to use FaceTime ("blocking" as a policy) are a net neutrality infraction, in a broad sense.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Orange “Sosh” Illustrates Competitive Challenge, and Range of Responses

Mobile and fixed network service providers are, by now, used to competition. And, by now, there are some standard competitive responses to new competition, in either the mobile or fixed services realm.

Typically, incumbent service providers are attacked on the pricing front, the reason being that the simplest of all value propositions for a customer is “same product, lower price.” So the easiest marketing position for a challenger to take is “same product, lower price.”

Typically, mobile service providers respond by creating new “value” brands that attempt to protect pricing for the mainstay brands, while allowing the new value brand to compete head to head with lower-cost competitors.

Sometimes it works better than others, though. In France, Orange has found that its initial assumptions about what is required to compete with Illiad’s “Free” service have been inadequate. That seems to be the case right now.

Sosh, sold only online as a way of creating differentiation and controlling sales cost, has boosted account data buckets for its top offer to 3 GBytes, to match Free’s offer, and also creating new price plans that better align with Free’s offers.

The Orange packaging changes come as Sosh adapts to a pricing attack that has been more vigorous than anticipated. The other French mobile leaders, including Bouygues Telecom and SFR, also have had to adjust to Free’s attacks by crafting their own value brands or changing retail packaging.

In this case, the leaders are trying to contain the pricing damage by creating value brands that compete with Free on price, while generally protecting the existing prices of the original brands. The longer term issue is whether that strategy is sustainable over the longer term.

The danger is that, at some point, the pricing expectations change so much that the original brands have to lower prices as well. So far, Orange appears to have been quite surprised by the vigorous Free pricing.

Compared to the initial offers unveiled in September 2011 by Sosh, the latest price drops at Sosh are significant. Sosh initially offered 1 GByte buckets of usage for 39.90 euros. Sosh now offers is now three times more data for less than 37 percent of the original retail pricing.

So far, the pricing umbrella has dropped only for the major mobile carrier “value” brands. The bigger issue is how long it might be before general end user expectations about value and price change enough that even the original brands must respond to the price pressure.

In the fixed network realm, the choices generally have been more limited. Mobile service providers can choose to offer different devices, can sell postpaid or prepaid and can change service features about as easily as they change devices. That's one advantage of running a business where so much of the feature set is "at the edge."

Mobile service providers also have found it easier to create wholly new value brands around customer segments.

In the realm of voice services, for example, most telcos seem to have concluded that it was not feasible to create some sort of "value" voice service directly competitive to over the top VoIP. So the decision generally has been to allow some loss of market share, in order to maintain pricing and margin for the remaining units sold.

In the case of high speed access, telcos in the U.S. market, for example, did not respond until it was clear that a new product category had been created, that legacy special access services really would not be damaged by substitution and that the telcos would lose huge amounts of that market to cable and other competitors if they did not jump in.

Typically, incumbent service providers are attacked on the pricing front, the reason being that the simplest of all value propositions for a customer is “same product, lower price.” So the easiest marketing position for a challenger to take is “same product, lower price.”

Typically, mobile service providers respond by creating new “value” brands that attempt to protect pricing for the mainstay brands, while allowing the new value brand to compete head to head with lower-cost competitors.

Sometimes it works better than others, though. In France, Orange has found that its initial assumptions about what is required to compete with Illiad’s “Free” service have been inadequate. That seems to be the case right now.

Sosh, sold only online as a way of creating differentiation and controlling sales cost, has boosted account data buckets for its top offer to 3 GBytes, to match Free’s offer, and also creating new price plans that better align with Free’s offers.

The Orange packaging changes come as Sosh adapts to a pricing attack that has been more vigorous than anticipated. The other French mobile leaders, including Bouygues Telecom and SFR, also have had to adjust to Free’s attacks by crafting their own value brands or changing retail packaging.

In this case, the leaders are trying to contain the pricing damage by creating value brands that compete with Free on price, while generally protecting the existing prices of the original brands. The longer term issue is whether that strategy is sustainable over the longer term.

The danger is that, at some point, the pricing expectations change so much that the original brands have to lower prices as well. So far, Orange appears to have been quite surprised by the vigorous Free pricing.

Compared to the initial offers unveiled in September 2011 by Sosh, the latest price drops at Sosh are significant. Sosh initially offered 1 GByte buckets of usage for 39.90 euros. Sosh now offers is now three times more data for less than 37 percent of the original retail pricing.

So far, the pricing umbrella has dropped only for the major mobile carrier “value” brands. The bigger issue is how long it might be before general end user expectations about value and price change enough that even the original brands must respond to the price pressure.

In the fixed network realm, the choices generally have been more limited. Mobile service providers can choose to offer different devices, can sell postpaid or prepaid and can change service features about as easily as they change devices. That's one advantage of running a business where so much of the feature set is "at the edge."

Mobile service providers also have found it easier to create wholly new value brands around customer segments.

In the realm of voice services, for example, most telcos seem to have concluded that it was not feasible to create some sort of "value" voice service directly competitive to over the top VoIP. So the decision generally has been to allow some loss of market share, in order to maintain pricing and margin for the remaining units sold.

In the case of high speed access, telcos in the U.S. market, for example, did not respond until it was clear that a new product category had been created, that legacy special access services really would not be damaged by substitution and that the telcos would lose huge amounts of that market to cable and other competitors if they did not jump in.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, August 21, 2012

T-Mobile Will Introduce New “Unlimited” Data Plan?

T-Mobile USA might be preparing launch of a new unlimited plan without caps or rate limiting. The rumored plan is said to be priced at $30 for "Classic Plan" customers and $20 for "Value Plan" customers. If you want to use your device for personal hotspot service, though you will have to buy another plan, such as the 5GB and 10GB rate plan options, instead.

But the T-Mobile USA and new MetroPCS unlimited plans show that competition in the high-speed access space is not as limited as many would argue it is.

But the T-Mobile USA and new MetroPCS unlimited plans show that competition in the high-speed access space is not as limited as many would argue it is.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...