It is a given that Apple is different, post Steve Jobs. Equity prices aren't everything, but Apple's stock price suggests investors are uncertain about the company's prospects, with Tim Cook as CEO. The comparison is unfair, in many ways.

Some of us would argue that although it largely is true "nobody is indispensable," it is not always true. Steve Jobs was an extremely unusual CEO. So would there be a regression to the mean, in terms of CEO "potential impact?" Almost certainly.

The issue is how well Apple can manage its future without Steve Jobs. In that regard, Cook argues that Apple will in the future have to rely on many contributions, with teams--and teamwork--more important than in the past.

That likely would be the only logical answer no matter who was running Apple.

Monday, June 3, 2013

How Tim Cook Sees Apple's Values

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Mobile PCs are Driving Mobile Data Consumption

During 2013, overall mobile data traffic is expected to continue the trend of doubling each year, Ericsson predicts, driven in most regions except North America by mobile-connected PCs.

On average, a mobile PC generates approximately five times more traffic than a smart phone.

By the end of 2012, an average mobile PC generated approximately 2.5 GB per month, versus 450 MB per month produced by the average smartphone.

By the end of 2018, an average a mobile PC will generate around 11 GB per month and a smart phone around 2 GB.

Video traffic on mobile networks and is expected to grow by around 60 percent annually up until the end of 2018, by which point it is forecast to account for around half of total global traffic, according to the latest Ericsson estimates.

About 50 percent of all mobile phones sold in the first quarter of 2013 were smartphones, resulting in a doubling of mobile data traffic between 2012 and 2013, also says.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

EU Digital Commissioner wants 2014 Single Telecoms Market

Neelie Kroes, Europe’s digital commissioner, wants to unify the EU telecom market by the spring of 2014, including provisions that would end all roaming charges across national borders within the EU. But there are two distinct potential revenue implications.

Ending roaming charges will put pressure on mobile service provider top line revenue. But a single telecom market also should help clear the way for continent-wide consolidation of service providers, moves that should strengthen revenue and also allow operating cost economies.

The issue is whether a faster end to roaming charges is balanced with greater freedom to consolidate assets.

The European Commission has already restricted how much operators in Europe can charge for roaming, and the EC also has made clear its intention to seek further changes. In that sense, the end of roaming charges will be a negative for mobile service provider top line revenue.

| Current and proposed retail price caps (excluding VAT) | ||||

|---|---|---|---|---|

| 1st July 2012 | 1st July 2013 | 1st July 2014 | ||

| Data (per MB) | 70 cents | 45 cents | 20 cents | |

| Voice calls made (per minute) | 29 cents | 24 cents | 19 cents | |

| Voice calls received (per minute) | 8 cents | 7 cents | 5 cents | |

| SMS (per SMS) | 9 cents | 8 cents | 6 cents | |

As an example, the existing price caps, in place since July 2012, allow a maximum of

70 cents per Megabyte when using the Internet whilst travelling abroad.

In July 2009, use of a megabyte worth of data would have cost more than € 4. So the cost of roaming use of the Internet was cut about 600 percent or more, in some cases.

Charges will continue to fall down to 19 cents per minute for calls and 20 cents per MB for internet access by 2014.

Given the financial pain lower wholesale roaming rates have been causing for European service providers, and the certainty that revenue will continue to fall further, an end to all roaming charges might not seem a welcome change.

Vodafone, for example, says international roaming in Europe accounts for around three percent of group revenue. And you can assume profit margins are very high, as there is almost no cost to generate the roaming revenue.

Vodafone furthermore generates around 11 percent of group earnings before interest, taxes, depreciation and amortization from European roaming, according to Bernstein Research.

But there is another potential change if the EU really can move to a single telecom market framework, namely that cross-border operations, and presumably cross-border mergers and acquisitions, will allow carriers to gain the scale they believe they need to make investments and slice operating costs.

On the other hand, European service providers have broadly called for relaxation of antitrust rules, to allow for much more consolidation in the market.

With more than 1,200 fixed network operators and almost 100 mobile networks, most operating with less than optimal economies of scale, operators argue it is not possible to create viable long-term businesses unless cross-border acquisitions and mergers are permitted and even encouraged.

Part of the impetus for reform is a perceived need to create a more-encouraging climate for investment in next generation networks. That is more controversial than might first seem to be the case.

One of the problems with the wholesale framework used in Europe is that network owners do not have high incentives to upgrade their networks. At least, that is the underlying carrier argument.

Where service providers leasing wholesale capacity often have profit margins in the 20-percent range, few network operators who provide that access have profit margins much exceeding 10 percent, if they make money at all.

As was the case in the United States, European service providers have complained that mandatory wholesale provisions with high discounts for wholesale customers make high-risk investments in next generation networks unappetizing.

So the call for an expedited move to a single telecom market conceivably would allow service providers more freedom to acquire assets and create fewer, but larger, suppliers.

Somewhat ironically, restricting mobile service provider revenues (lowering and then ending roaming charges) to gain a consumer advantage also creates a greater need for service providers to consolidate, which might create more market power, which some would argue necessarily means consumers lose advantage.

But consolidation now seems inevitable, as the underlying economics of the fixed network business worsen, while the mobile business also faces more challenging economics.

"Bulking up" to remove overhead costs and gain customer and revenue scale is a proven way for contestants to increase operating results and obtain growth in mature or declining markets.

Under those conditions, regulators have to pay as much attention to spurring investment as to ensuring robust competition.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, June 1, 2013

Dish Really Doesn't Want to Buy Sprint, Grubman Argues

Jack Grubman, the once-influential telecom equity analyst who now is banned from the business, remains an astute observer of the U.S. telecom business. Count Grubman among those who believes Dish Network really does not want to own Sprint or Clearwire.

"[Ergen] wants to agitate … to get a network access deal from Sprint," the founder of consultancy firm Magee Group said.

In effect, the Dish Network bids for Clearwire and Sprint really are bargaining chips intended to convince Sprint and Softbank to work with Dish Network as it creates a new national Long Term Evolution network.

Grubman does not seem to believe the Dish Network gamble will ultimately result in the upstart taking significant share from the market leaders, or even continuing to exist as a going concern.

"For someone who made his name covering the 1990s explosion in the telecommunications sector, the "strategic logic" behind Dish Network's bid for Sprint Nextel brings back bad memories," Grubman said.

"A newly formed, highly leveraged company promising to take market share from more established competitors with stronger, less leveraged balance sheets is a movie I have seen before. Trust me, it ends badly," Grubman said.

Veterans of all the various disruptions within the U.S. telecommunications business might tend to agree that there is very little precedent, at least so far, for a true upstart to take market leadership, on a sustained basis, from the leaders.

Equity value will not be created. But at least so far, no challenger has managed to upset the ranks of leading service providers. That is not to say it "cannot be done." It just hasn't happened yet.

In effect, the Dish Network bids for Clearwire and Sprint really are bargaining chips intended to convince Sprint and Softbank to work with Dish Network as it creates a new national Long Term Evolution network.

Grubman does not seem to believe the Dish Network gamble will ultimately result in the upstart taking significant share from the market leaders, or even continuing to exist as a going concern.

"For someone who made his name covering the 1990s explosion in the telecommunications sector, the "strategic logic" behind Dish Network's bid for Sprint Nextel brings back bad memories," Grubman said.

"A newly formed, highly leveraged company promising to take market share from more established competitors with stronger, less leveraged balance sheets is a movie I have seen before. Trust me, it ends badly," Grubman said.

Veterans of all the various disruptions within the U.S. telecommunications business might tend to agree that there is very little precedent, at least so far, for a true upstart to take market leadership, on a sustained basis, from the leaders.

Equity value will not be created. But at least so far, no challenger has managed to upset the ranks of leading service providers. That is not to say it "cannot be done." It just hasn't happened yet.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, May 30, 2013

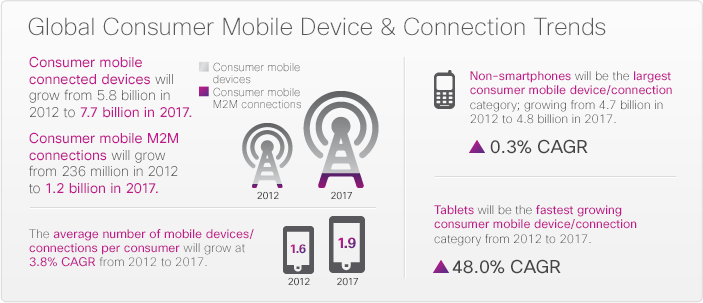

Global IP Traffic Will Grow 23% Annually to 2017

Global IP traffic has increased more than fourfold in the past five years, and will increase three fold over the next five years, according to the Cisco Visual Networking Index. Growth would surprise absolutely nobody. But the relatively restrained rate of annual growth might.

Global IP traffic has increased more than fourfold in the past five years, and will increase three fold over the next five years, according to the Cisco Visual Networking Index. Growth would surprise absolutely nobody. But the relatively restrained rate of annual growth might.Overall, IP traffic will grow at a compound annual growth rate (CAGR) of 23 percent from 2012 to 2017. Given rates of growth that had been higher in the past, that relative slowdown in growth rates is noteworthy.

Among other notable changes, metro traffic will surpass long-haul traffic in 2014, and will account for 58 percent of total IP traffic by 2017.

Metro traffic will grow nearly twice as fast as long-haul traffic from 2012 to 2017 in large part because of the increasingly significant role of content delivery networks, which bypass long-haul links and deliver traffic to metro and regional backbones.

Content Delivery Networks (CDNs) also will carry 51 percent of all Internet traffic in 2017 globally, up from 34 percent in 2012.

Also, nearly half of all IP traffic will originate with non-PC devices by 2017.

In 2012, only 26 percent of consumer IP traffic originated with non-PC devices, but by 2017 the non-PC share of consumer IP traffic will grow to 49 percent.

PC-originated traffic will grow at a CAGR of 14 percent, while TVs, tablets, mobile phones, and machine-to-machine (M2M) modules will have traffic growth rates of 24 percent, 104 percent, 79 percent, and 82 percent, respectively.

Traffic from wireless and mobile devices will exceed traffic from wired devices by 2016. By 2017, wired devices will account for 45 percent of IP traffic, while Wi-Fi and mobile devices will account for 55 percent of IP traffic. In 2012, wired devices accounted for the majority of IP traffic at 59 percent.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tablets Replace PCs in Dakar Cybercafe

The Equinox cybercafe, located in Dakar’s Medina neighborhood, has replaced PCs with 15 tablets. Available at the same price as a regular cybercafe computer session at about $0.60 an hour, the move illustrates the potential role tablets will play in getting computing devices into the hands of users in many developing regions, according to the Google Europe Blog.

The Equinox cybercafe, located in Dakar’s Medina neighborhood, has replaced PCs with 15 tablets. Available at the same price as a regular cybercafe computer session at about $0.60 an hour, the move illustrates the potential role tablets will play in getting computing devices into the hands of users in many developing regions, according to the Google Europe Blog.Aside from lower capital and probably operating costs for the cybercafe, use of tablets also consumes less electricity. Smart phones will play much the same role.

Now if we can just get the cost of infrastructure down, in a disruptive way.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Will Mobile and Fixed Internet Access Business See Substitution?

In 2012, perhaps one percent of U.S. households stopped paying for home Internet subscriptions and relied on wireless access instead, according to Leichtman Research Group.

That small amount of wireless substitution in the Internet access market will not bother providers of mobile broadband service.

That small amount of wireless substitution in the Internet access market will not bother providers of mobile broadband service.

Video cord cutting, though more prevalent, still amounts to only about a few percent of households.

Zero TV households number about five million, or about three percent of U.S. households.

Arguably, most "mobile broadband substitution" takes the form of users dropping their fixed wireless subscriptions and relying on free Wi-Fi and their mobile broadband plans.

Some lighter users, who mostly use social networking apps and sites, might find the approach works. People who don't mind moving to places where there is public Wi-Fi might add some amount of watching video. But multi-user households and frequent video watchers will find mobile broadband substitution a difficult proposition.

That small amount of wireless substitution in the Internet access market will not bother providers of mobile broadband service. Video cord cutting, though more prevalent, still amounts to only about a few percent of households.

Zero TV households number about five million, or about three percent of U.S. households.

Arguably, most "mobile broadband substitution" takes the form of users dropping their fixed wireless subscriptions and relying on free Wi-Fi and their mobile broadband plans.

Some lighter users, who mostly use social networking apps and sites, might find the approach works. People who don't mind moving to places where there is public Wi-Fi might add some amount of watching video. But multi-user households and frequent video watchers will find mobile broadband substitution a difficult proposition.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...

{kind=link}