Vodafone and Verizon Communications seem to have agreed on a $130 billion price for the sale of Vodafone's 45 percent stake in Verizon Wireless to Verizon Communications. The deal still has to be approved the boards of both companies, but there would seem to be little danger of a complication on that front.

Verizon would pay for the stake in roughly equal portions of cash and stock, so Vodafone would become a minority investor in Verizon Communications, though holding publicly tradeable stock that could be sold gradually to liquify the rest of the sale proceeds.

The deal would not change U.S. mobile market share at all, and should not trigger unusual regulator scrutiny.

The drama might follow, though. Will Vodafone itself go on a buying spree? Will another major global carrier make a bid to buy Vodafone? And what will other European service providers conclude they must do?

At the very least, executives have to make fundamental decisions about whether they are going to be buyers or sellers.

Sunday, September 1, 2013

Vodafone Agrees to Sell its Stake in Verizon Wireless for $130 Billion

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Microsoft Research Study Shows People are Rational About Internet Access Choices

A study by Microsoft Research India, while investigating one question, might also suggest an answer to other questions, among them the rationality of Internet consumers, the important role played by retail tariffs and usage caps, as well as user ability to maximize overall use of all Internet access resources available in any market, in ways that maximize end user satisfaction and value.

The specific question the researchers asked was “if you have the internet in your pocket, why do you still visit a public access venue?” They studied teenager behavior in Cape Town, South Africa.

Most grade-11 teens in low-income township schools in Cape Town have used their mobiles to access the internet since 2008, the researchers note. By 2010, South Africa had over 100 percent mobile penetration (50 million subscriptions) but only 743,000 fixed broadband subscribers, they also say.

The findings were that teenagers “who could, in theory, be ‘mobile-only’ Internet users have instead constructed a ‘mobile-centric’ repertoire.” They used their more-expensive mobile access when needed for some tasks, but shifted resource-intensive operations to public access venues, including libraries and cybercafes.

Doing so saves them money and also offers a better end user experience. Mobiles are used for quick, non-intensive apps. Libraries get used for quick-turnaround search-copy-paste-print operations, when sessions are limited to 15 minutes, for example.

Internet cafes tended to be used when video editing and visual design as well as integration with handwritten and photocopied material was required.

The larger point is that Internet users, one might argue, is that people in low-income parts of Cape Town, South Africa, or in developed nations, are rational and competent judges of ways they use access services.

They shape their own usage behavior based on accurate assessments of what forms of access save them money and best match the purposes for which they are using the Internet.

Some may use Internet cafes because of the better hardware (faster PCs, better printers and peripherals), since PC hardware is expensive in South Africa, due to import duties and

lack of domestic manufacturing.

Mobile coverage is good but data tariffs are relatively expensive. Usage caps for digital subscriber line services are frequently capped with monthly limits as low as 1GB.

Wireless data is purchased in a way similar to prepaid airtime, encouraging end user attention to “running meters.”

The implications are clear enough. “Broadband policy” consists of more than building faster networks of all types. The way tariffs are structured has a powerful impact on user behavior, leading people to consume access in logical ways.

That is why Wi-Fi offload has become such a pronounced activity in many developed markets.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, August 31, 2013

Verizon, Vodafone Making Different Bets on Market Growth?

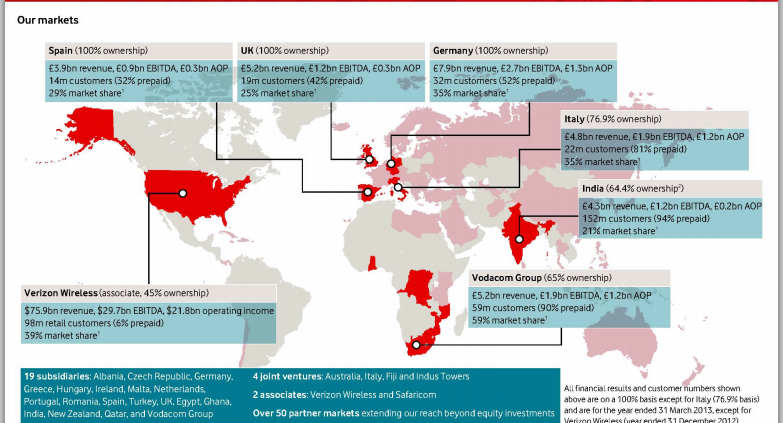

Either way you look at the strategic challenges, both Vodafone and Verizon Communications are making big bets in assessing whether the U.S. or European markets are better places to invest for growth.

You might argue Verizon Communications is betting that the U.S. market is going to remain robust, so capturing all of the returns from Verizon Wireless makes sense.

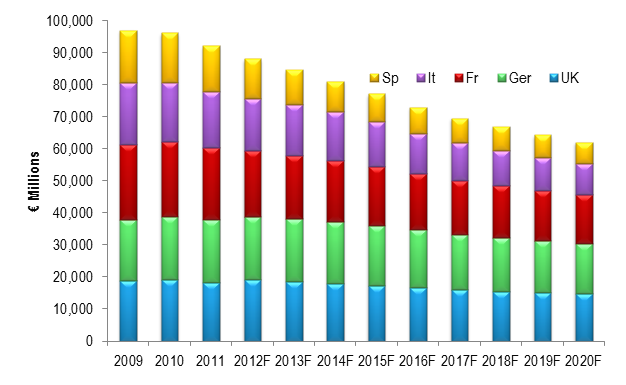

You might also argue that in selling its highest-revenue operation, Vodafone is making the opposite calculation, namely that despite a clear revenue down trend in Europe, Vodafone’s prospects actually are higher in Europe than in the U.S. market, which virtually all observers currently estimate will grow revenues .

AT&T appears to agree with Vodafone, specifically because the undeveloped state of Long Term Evolution in Europe will allow for revenue growth, once the networks are activated.

Others might argue that Verizon Communications is gambling a bit that the U.S. market has not reached a revenue peak, in terms of revenues. Some would argue that increasingly competent new attacks by a revitalized T-Mobile US and a SoftBank-driven Sprint will lead to a major price war that will depress industry revenues.

In Western Europe, for example, revenue is forecast to drop through 2020, for example. Some would attribute that weakness to competitive pressures.

By way of comparison, the U.S. market is viewed as less competitive, and Verizon is betting that it will do better by essentially increasing its U.S. mobile exposure, since mobile contributes about 86 percent of total Verizon Communications revenue. Fixed network operations contribute only about 14 percent.

Keep in mind that it was Vodafone that sold its struggling Japanese asset to SoftBank in 2006. Vodafone executives might expect that something similar will happen in the U.S. market, as a SoftBank-owned Sprint attacks U.S. mobile industry pricing structure.

NTT DoCoMo was the dominant service provider then, as Verizon Wireless is now. NTT DoCoMo still holds that position, but gross revenue and profit margins have been battered.

“If you’ve watched what happens when Softbank enters a wireless market, you might not want to watch it again,” said Craig Moffett, senior analyst at Moffett Research.

Right now, observers expect U.S. mobile revenue growth, just as they expect declines in many parts of Europe.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Happened to Free Speech in the U.S.?

Seriously, this is more than stupid. It shows imperial arrogance.

shared via http://feedly.com

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Spending Now 10% of all E-Commerce

Almost always, an important new consumer electronics product or application hits an adoption inflection point st about 10 percent adoption.

It now appears th at inflection point has been reached, for mobile commerce.

ComScore Chairman Gian Fulgoni. “One out of every ten consumer e-commerce dollars is now spent using either a smartphone or a tablet, and growth in this segment of the market is outpacing that of traditional e-commerce by a factor of 2x, which itself is growing at rates in the mid-teens.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tablets Might be Fastest-Growing Consumer Electronics Technology, Ever

Important consumer electronics innovations used to take decades to reach majority adoption.

Digital techologies get adopted much faster. Years are more typical. Tablets might be the new benchmark.

Netbiscuits reported that the tablet market had a year-on-year growth of 65 percent by 2013. It was also revealed that the market has made room for new competitors other than Apple's iPad. In 2012, 60 percent of tablet sales were attributed to Apple, but that number has fallen to just 33 percent in 2013. Android tablet sales were reported at 38 percent in 2012, and rose to 63 percent in 2013.

Tablet adoption in India rose 400 per cent in 2012 and sales in Southeast Asia have spiked 101 percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, August 30, 2013

Will Vodafone Survive Verizon Wireless Sale?

Any Vodafone sale of its stake in Verizon Wireless could trigger additional deals. AT&T might want to buy Vodafone, some theorize.

AT&T could pay about 80 billion pounds ($124 billion) for what’s left of Vodafone, according to Robin Bienenstock, an analyst at Sanford C. Bernstein, basing her estimate on a valuation of six times earnings before interest, tax, depreciation and amortization.

AT&T has examined takeover candidates including Vodafone, U.K. mobile carrier EE (a joint venture between Deutsche Telekom and Orange), as well as parts of Spain’s Telefonica.

That might strike some as odd, given the declining amount of revenue being earned by European mobile service providers. But AT&T seems to be thinking, as does SoftBank’s Sprint, about ways to boost revenue by emphasizing fourth generation Long Term Evolution services.

Compared to the United States, for example, 4G is undeveloped in much of Europe.

But it would also be fair to say that if Verizon Wireless does buy out Vodafone, then Vodafone would be in position to be a buyer itself. And subsequent deals could set off a major round of consolidation.

"Once you have companies that are after global scale, it becomes a case of eat or be eaten," said Robin Bienenstock, an analyst for Bernstein Research. "The chessboard is going to re-form really, really rapidly."

AT&T could pay about 80 billion pounds ($124 billion) for what’s left of Vodafone, according to Robin Bienenstock, an analyst at Sanford C. Bernstein, basing her estimate on a valuation of six times earnings before interest, tax, depreciation and amortization.

AT&T has examined takeover candidates including Vodafone, U.K. mobile carrier EE (a joint venture between Deutsche Telekom and Orange), as well as parts of Spain’s Telefonica.

That might strike some as odd, given the declining amount of revenue being earned by European mobile service providers. But AT&T seems to be thinking, as does SoftBank’s Sprint, about ways to boost revenue by emphasizing fourth generation Long Term Evolution services.

Compared to the United States, for example, 4G is undeveloped in much of Europe.

But it would also be fair to say that if Verizon Wireless does buy out Vodafone, then Vodafone would be in position to be a buyer itself. And subsequent deals could set off a major round of consolidation.

"Once you have companies that are after global scale, it becomes a case of eat or be eaten," said Robin Bienenstock, an analyst for Bernstein Research. "The chessboard is going to re-form really, really rapidly."

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...