Thursday, December 5, 2013

Mobile Broadband will be 81% of Total Broadband in Emerging Markets by 2016

By 2016, mobile broadband will represent 81 percent of broadband connections in emerging markets, according to Qualcomm.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

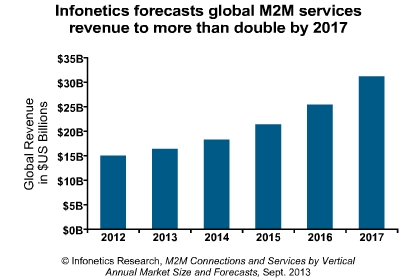

M2M Might Represent 6% of Global Mobile Connections by 2017

Virtually all observers concede that machine-to-machine mobile connections are growing.

The big question is how much growth will happen, and how much revenue M2M will contribute.

By 2017, machine-to-machine links will account for about 17 percent of global mobile data traffic, according to Deloitte analysts.

Berg Insights predicts M2M connections will grow at a compound annual growth rate of 24.4 percent to reach 489.9 million connections in 2018.

If there are 8.5 billion total mobile connections by 2017, M2M would represent perhaps six percent of global mobile connections.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

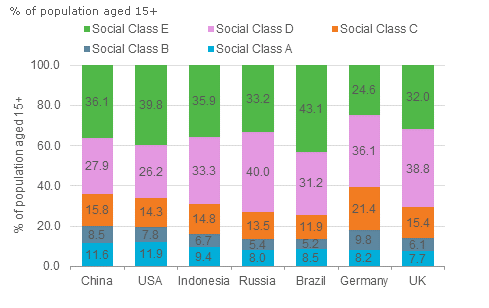

Chinese iPhone Buyers are Not "Average"

Can Apple succeed in the China market with its strategy of selling primarily in the "premium" segment of the handset market?

Though some doubt it, others think the strategy will work.

Doubters tend to point to low "average" income.

That is significant for sellers of luxury goods, of course, and are key to Apple’s hopes in China, where the Apple iPhone will be a pricey option. Some argue that most consumers will not be able to easily afford an iPhone, since Apple has not released a “low cost” iPhone.

That is not the point, others might say. Apple is pinning its hopes on a segment of the market that can afford the device, and will count on the income of potential buyers in the upper deciles of income distribution in China.

In China, income distribution, if not magnitude, is rather well correlated with income distribution in the United States, for example.

In one measure of income data, looking at the number of individuals whose incomes fall within a specified range of the average gross income of all individuals aged 15+ in that country or region, China and the United States are similar.

In China, 36 percent of people had incomes 200 percent above average, compared to 40 percent in the United States, for example.

Most significantly, the middle class in China, as elsewhere in the developing world, continues to expand in absolute terms.

Amit Daryanani of RBC Capital Markets estimates Apple will see an additional $9 billion to $10 billion in annual revenue added from a deal with China Mobile, for example.

By some measures, an iPhone could cost 10 percent of annual income in China. But that's the point: Chinese iPhone buyers will not have "average" income.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, December 4, 2013

VoLTE Will Help Mobile Service Providers Shut Down 2G and 3G Networks

The launch of Voice-over-LTE (VoLTE) services by major carriers first in South Korea and soon in the United States is part of the effort to move voice calls from the circuit switched 2G and 3G networks to the packet switched LTE networks.

That will have important implications for suppliers of VoLTE platforms, ranging from infrastructure providers to handset suppliers.

“For CDMA operators such as Verizon, aggressive LTE deployment is necessary because a VoLTE call cannot fall back to the circuit switched domain,” said Ying Kang Tan, research associate at ABI Research. “Even for WCDMA operators like AT&T, it makes sense to do likewise because LTE is much more spectral efficient than WCDMA.”

But enabling VoLTE also makes possible spectrum refarming, making it easier for mobile service providers to turn off 2G networks and use that spectrum for more 4G capacity.

As such, by the end of 2014, when VoLTE has gained more momentum, ABI Research expects more than 93 percent of the North American population to have access to LTE, for example.

“In 2014, LTE handset shipments in Asia-Pacific and North America—the two largest handset markets—will grow by 28 percent and 25 percent to reach 150 million and 81 million respectively,” said Jake Saunders, VP and practice director of the LTE Research Service.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

New FCC Chairman Distinguishes Between "No Blocking" and "Quality of Service," It Seems

One clear difference of opinion about U.S. Internet policy is whether content delivery networks are an impermissible violation of the rule that users must be able to access and use all lawful applications on the Internet.

Content delivery networks are standard on the back end of the access market, allowing application owners to pay other firms to minimize latency.

The issue has been whether it also is permissible to allow firms or end users to take similar measures to minimize latency and improve end user experience.

Blocking is not the issue. Methods of providing enhanced user experience, without any blocking, are the issues.

Anti-competitive behavior is a potential problem, as if an ISP minimized latency for its own services, but would not allow it for competing services.

But the FCC seems keenly aware of such dangers, as does the Department of Justice.

Also, business users already can buy services that support latency reduction. The issue is whether consumers can receive any similar quality of service support.

New F.C.C. Chairman Tom Wheeler seems to affirm both the "Open Internet" rules, which forbid Internet service providers from favoring their own content or paid content when allowing data to flow through their system, as well as quality assurance mechanisms, though.

Wheeler said variable pricing and service plans represented the effects of competition. “We might see a two-sided market,” where a company like Netflix might pay an Internet service provider to guarantee that Netflix customers get the best available transmission speeds.

It's more than a nuance. At the moment, it is among the key dividing lines between supporters and opponents of such latency-reducing measures.

Content delivery networks are standard on the back end of the access market, allowing application owners to pay other firms to minimize latency.

The issue has been whether it also is permissible to allow firms or end users to take similar measures to minimize latency and improve end user experience.

Blocking is not the issue. Methods of providing enhanced user experience, without any blocking, are the issues.

Anti-competitive behavior is a potential problem, as if an ISP minimized latency for its own services, but would not allow it for competing services.

But the FCC seems keenly aware of such dangers, as does the Department of Justice.

Also, business users already can buy services that support latency reduction. The issue is whether consumers can receive any similar quality of service support.

New F.C.C. Chairman Tom Wheeler seems to affirm both the "Open Internet" rules, which forbid Internet service providers from favoring their own content or paid content when allowing data to flow through their system, as well as quality assurance mechanisms, though.

Wheeler said variable pricing and service plans represented the effects of competition. “We might see a two-sided market,” where a company like Netflix might pay an Internet service provider to guarantee that Netflix customers get the best available transmission speeds.

It's more than a nuance. At the moment, it is among the key dividing lines between supporters and opponents of such latency-reducing measures.

Strand Consult has analyzed this debate and its stakeholders and presents the 30 arguments that net neutrality supporters will likely use to further their position. The 30 arguments are:

- Neutrality (or “openness”) is an original, deliberate, and essential feature of the internet.

- The end to end principle is responsible for internet innovation.

- Zero is a fair price for content delivery, and it was established early in the development of the commercial internet.

- The internet needs regulation to keep it neutral and to preserve its many fine features.

- Net neutrality is common carriage.

- Net neutrality is free speech.

- Without net neutrality there will be no innovation

- Without net neutrality there will be no democracy

- Operators' networks consist of smart edges and a dumb core. The operator's job is to deliver the bits.

- The internet is a human right.

- The internet is a public good and therefore should be regulated like a utility. Internet service should be free, meaning subsidized by the government.

- All content is equal or a bit is a bit is a bit.

- Consumers value all content the same, and more content is better.

- There should be the same internet available on every device.

- Applications don’t create traffic; users create traffic.

- The leaders of the net neutrality movement have good and right on their side.

- Consumers care about net neutrality, and the net neutrality activists are their voice.

- Net neutrality is needed because of vertical integration in the market for content and internet access.

- There is a lot of evidence proving that network management practices harm customers.

- Operators want to harm their customers, and only preventive measures will keep them in check.

- Operators want to block or throttle competing services.

- Operators want to use price discriminate to exploit their customers.

- Operators want to make agreements to preference certain content on the web.

- Operators will use pricing to create fast lanes and dirt roads for internet access.

- Operators will use deep packet inspection to exploit their customers.

- Operators only invest because of the growth in applications and content.

- Operators should just build infrastructure, and more infrastructure is better.

- Operators have always invested in infrastructure, and they always will

- All broadband providers, whether cable or telco, should be classified as common carriers and their obligations increased.

- Net neutrality is a human rights issue, not an economic issue.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Windstream Isn't the Company It Used to Be

Sometimes, a company has to enter new markets to survive the maturation of its older business. Windstream provides an example, as it is not the “rural telco” it was in 2006. Today, it is something closer to a “competitive local exchange carrier,” earning the bulk of its revenue from business customers.

Sure, Windstream now is more a “national” provider, where it used to be a “regional” service provider. But the big change is where it derives its revenue. In the past, it has made most of its money from rural consumers. Now, it makes most of its money from business segment customers, increasingly in instances where it does not own or operate full facilities-based access networks.

In fact, both Windstream and Frontier Communications, another firm whose legacy business could aptly be described as “rural consumers,” now make a majority of revenue from the business customer segment.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

More Trouble for 4G LTE Investment Models

Will fourth generation Long Term Evolution profit margins be sacrificed to speed mobile operator growth? It already is, in some instances.

You know what that means: increased difficulty for the 4G LTE investment decision, in some instances.

French mobile service provider Free Mobile has added an LTE 4G high-speed broadband service to its Free Mobile package without raising the price, in a market where its chief rivals charge a premium for using the 4G network.

Iliad says its monthly Free Mobile subscription remains unchanged at 19.99 euros a month including 4G, without a long-term contract.

Pressure on LTE profit margins is evident elsewhere as well. EE in the United Kingdom is bundling unlimited calling and texting when roaming in some European countries on 4G. Without necessarily eliminating a cost premium for using the LTE network, the “no incremental cost roaming” is another way of merchandising the LTE network without directly eliminating a cost premium on recurring service.

Hutchison Whampoa’s “3” in the United Kingdom has added an additional four countries (United States, Indonesia, Sri Lanka, and Macau) to its U.K. “Feel at home” roaming plan which allows United Kingdom-based consumers access to their respective voice and data allowances abroad. These new territories make a total of 11 countries where free roaming is available.

The obvious implication is that 3 is deliberately sacrificing potential revenue to grow its global presence, since roaming fees are a high-margin service, as Free Mobile is using the “no incremental cost” approach to take market share from other mobile operators in France.

The use of free 4G LTE roaming is part of Hutchison Whampoa’s effort to create a bigger global network. Three operates in Indonesia and Sri Lanka, but the U.S. market is the first country offering free roaming where 3 does not have a facilities-based presence.

The “Feel At Home” program now operates in 11 destinations around the world.

For mobile service providers investing in brand-new LTE networks, the fact that some competitors are willing to offer the new service at no premium over 3G will make the business case for 4G harder.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...