The EU’s broadband and telecom policy is not working, according to Strand Consult. Disincentives for investment and inability for firms to merge are among the key problems, Strand Consult argues.

On the other hand, one might argue that EU public policy was intentional. By mandating affordable wholesale access to incumbent networks, EU policy has succeeded at promoting competition.

But that very competition reduces network owner incentive to invest in upgraded facilities. The issue is not so much that the EU policies are “wrong,” as that they emphasize competition at the expense of investment.

U.S. regulators faced the same problem in the first decade of the 21st century, but made different choices. Aided by the fact that at least two fixed broadband networks exist in most markets, with two national satellite broadband providers and fixed wireless networks in many rural areas, U.S. regulators decided to create a framework conducive to investment, at the expense of mandated wholesale access.

The existence of Google Fiber, which seems on the cusp of becoming a much more serious force in the U.S. ISP market, was made possible, in large part, by a framework that allows ISPs and service providers to reap the rewards of their investments, principally by not forcing them to give wholesale customers easy access to those facilities.

In that sense, EU policy is not so much “wrong” as intended to produce different outcomes.

With important caveats (it always is possible to discover “gaps” of one sort of another. Whether those “gaps” are permanent or even fundamentally significant is the issue).

Strand Consult argues that the gap between European Union and U.S. investment in next generation networks is growing, as a result of the differing policy frameworks.

“The EU approach of managing competition through open access and price controls has not created incentives for investment in next generation broadband access,” says John Strand, Strand Consult CEO. 3. While the US has certain advantages being a large country with a common language, it made a decision to support the policies that maximize investment and innovation, namely a light-touch regulatory framework that allows broadband providers to get economies of scale, consolidate, earn profits, and invest.

Also, although many U.S. observers continue to insist there is a “broadband access problem” in the United States, Strand notes that the United States is “leading the EU on broadband measures such as the availability of broadband with download speeds of 100 Mbps or higher and availability of cable broadband, LTE, and FTTH.”

“Ten years ago the EU expected to lead the world in mobile with the GSM standard and six European phone manufacturers that accounted for half of the world’s phone,” says Stran. “Today no European handset makers remain, and America has surpassed Europe with 4G/LTE.”

It isn’t fundamentally too difficult to illustrate how policy would have to change to promote more investment. EU officials would have to make investment the policy objective.

That might involve allowing further consolidation of service providers and curbing wholesale obligations for fiber networks. As cable networks have in many markets emerged as the key challenger in the broadband networks space, measures that allow cable operators to invest in new networks also might be helpful.

The foundation of U.S. policy has been “inter-modal” competition between cable, telco and satellite providers, not “intra-modal” competition between incumbent and wholesale-based competitors.

That will be tougher in the EU zone. Still, policymakers fundamentally have to choose between investment or competition as the anchors of policy.

Any measures that create incentives for investment might limit wholesale access. And there would be a danger. Investment incentives for new, not just incumbent operators, would have to part of any change.

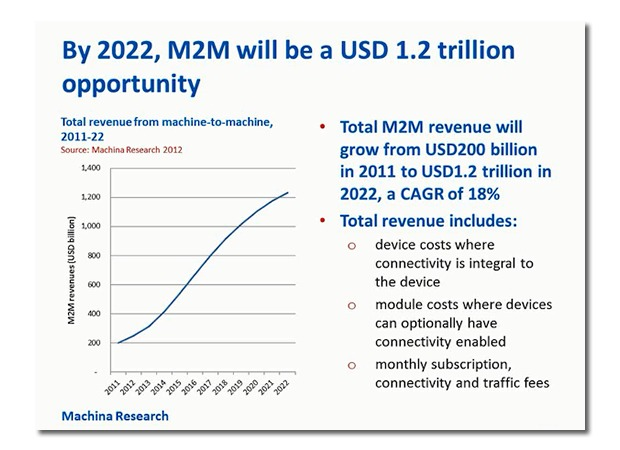

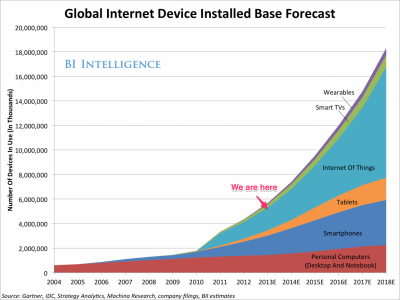

Some 1.9 billion devices already are connected to the Internet, and nine billion will be connected by 2018, making the “Internet of Things” a bigger market, in terms of devices, than smartphones, smart TVs, tablets, wearable computers, and PCs combined.

Some 1.9 billion devices already are connected to the Internet, and nine billion will be connected by 2018, making the “Internet of Things” a bigger market, in terms of devices, than smartphones, smart TVs, tablets, wearable computers, and PCs combined. Even by that measure, mobile service providers might earn $100 billion in 2022, a large enough number to warrant serious effort.

Even by that measure, mobile service providers might earn $100 billion in 2022, a large enough number to warrant serious effort.