Precisely what is happening in the linear video and over the top subscription businesses is unclear, even if most observers would agree the business clearly is in slow decline.

Paradoxically, consumers might eventually find that video bundles--even mostly linear--provide more value than a la carte streaming "channels" and services.

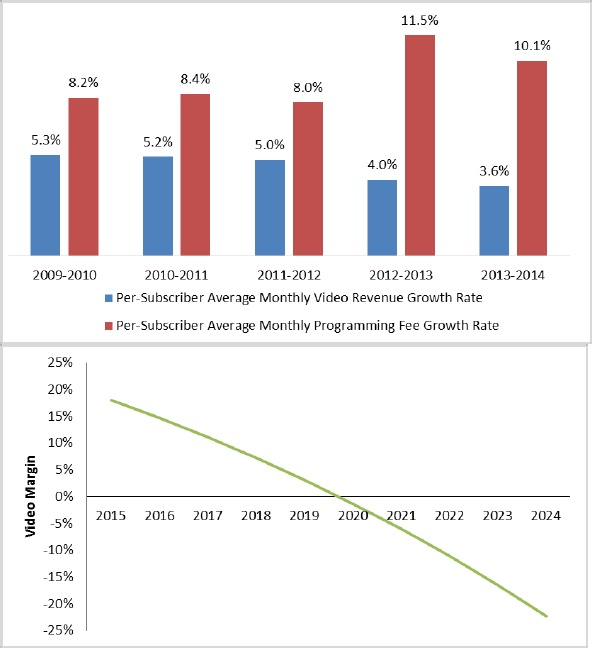

To be sure, strains in linear video are growing. In fact, by about 2020, smaller U.S. cable TV companies are going to experience zero profit margins on their linear video programming businesses, according to the American Cable Association.

Some would argue Verizon Communications likewise will have a hard time earning a profit on its own widespread investment in fiber to home networks, at least in part because revenue from new services has been less than anticipated.

Meanwhile, profit margins for linear video, in particular, have been rather low, Verizon now maintains, though in the past Verizon has claimed it earned good margins on video entertainment.

It would be going too far to argue video service providers are aggressively taking the bundle apart. It would be fair to say they are taking unprecedented steps to control costs, either by shrinking bundles or replacing expensive networks with cheaper apps.

Nor is the linear video business declining fast.

The biggest U.S. linear video subscription providers lost about 125,000 subscribers in 2014, on a net basis. Within the category, AT&T and Verizon gained about a million customers, while cable TV operators lost about 1.2 million accounts, on a net basis.

On an installed base of 95 million accounts, that barely registers, a tenth of one percent over a year’s time.

Of course, it is worth noting, the number of accounts does not speak to average revenue per account, or account profit margin, higher retention and acquisition costs, or other measures of segment health.

Presumably, those metrics are under pressure.

With the upcoming launch of HBO Now and Sling TV, we might see some indication of whether the rate of change--in terms of abandonment of linear subscriptions for over the top subscriptions--is about to increase.

But we might eventually find that cord cutting has demand more limited than many suppose. The reason is that cord cutting might not save most consumers money, and that arguably is the key attraction.

Some consumers buy a linear video subscription, plus Amazon Prime and Netflix. In other words, monthly spending is at about the $100 a month level. By switching to Sling TV and HBO Now, and keeping the other services, a consumer might replace an $80 linear subscription with an alternative $20 Sling TV subscription plus $15 a month for HBO Now, a savings of possibly $45 a month.

But that assumes the buyer is content to lose lots of channels. And the thing about linear video consumers is that each of us tends to watch only about a dozen channels, and perhaps only about seven on a regular basis.

Each consumer will evaluate how many of those "most watched" seven are sacrificed, to get lower recurring prices. If not, the consumer has to calculate the cost of obtaining them on a streaming basis. At a hypothetical cost of $10 per channel, those seven represent $70 a month in costs.

For some consumers, Sling TV represents none of the most-viewed channels. For others, Sling TV will represent a few of the most-watched channels. In other words, it isn't clear that unbundled streaming costs less than bundled linear service.

True, the ability to watch your subscription content “on any Internet-connected device” is valuable. But that probably will stop being a “unique” value at some point, when most content is available from one or more online sources, on an on-demand or subscription basis.

At that the point, the issue is going to be “cost,” compared to value. And it remains exceedingly hard to envision how a full on-demand business case will lead most consumers to pay less. In fact, they almost certainly will face higher costs for an a la carte approach.