Access networks are expensive; rural access networks more so, which explains why human beings so often complain about the quality of their communication services And with the qualification that there always are tensions within any business ecosystem between rival providers and roles, a wider range of options now are conceivable.

To use one example, tier one service provider business models and networks might not be the best way to provider internet access and mobile communications in many rural areas around the world.

Even some tier one organizations behave in ways that illustrate the truth of the statement. Verizon, for example, has been selling off its rural properties, and focusing on its urban networks. Former rural telcos including CenturyLink, Windstream and Frontier Communications have become firms deriving most of their revenues and actual profits from business customers, not consumers at all.

Mobile networks everywhere earn most of their revenue, and virtually all their profits, from a fraction of total cell sites in urban areas.

So many have a bottoms-up solution: stop trying to cram unworkable business models down and out, when only lower-cost “bottoms up” approaches make sense. That does not mean there is no role for tier-one providers, only that local access is not the optimal role in many rural and isolated locations.

Perhaps matters are more contentious for communities of larger size, where conflict over the propriety of municipal broadband always is heated. There arguably is much less room for debate where it comes to isolated and rural areas. In such areas the tier-one business model might not actually work.

It might well make more sense to use a local, bottoms up approach where a village or cooperative actually operates access facilities, in cooperation with other entities that provide backhaul and transport, and perhaps other services.

Time and again, in the effort to provide communications (internet and other services) to everyone, we keep returning to a core problem: the business model often does not work. Historically, the model breaks because networks cost too much and people cannot afford to buy services.

There are, of course, other issues ranging from technological proficiency to language and literacy, lack of backhaul or electrical power, plus other compelling problems such as sanitation and clean water access.

But the problems within some level of supplier control are retail cost of service, beginning with the cost to create the access networks.

A recent example is the estimate by Europe’s tier-one service provider organization ETNO that it will cost €660 billion to create ubiquitous gigabit internet access networks using fiber to the home, and might take as long as 30 years to achieve, at current rates of investment.

In many other regions and markets, the feasibility of any fixed network solution is questionable. One reason people now have voice and text communications is because suppliers largely shifted to mobile networks.

A key sensitivity even in the ETNO forecast is the assumption that fiber to the home is the platform. Increasingly, that is too narrow a view. In a few markets, it is entirely rational to argue that hybrid fiber cable TV networks can supply gigabit levels of speed for internet access on a timetable and at a retail cost fiber to home networks cannot match.

In a growing range of scenarios, urban, suburban and rural, it is becoming rational to think fixed wireless access will succeed where fixed networks or standard mobile networks cannot. Also, in rural and isolated areas, even more novel approaches might be necessary, such as village-level networks owned or operated by the community, or joint ventures between villages and tier-one service providers and transport providers.

Also, huge new efforts are being made to create and deploy new technology that should help change business models. Open source telecom technology is one approach. The CORD Project and Telecom Infra Project provide examples.

Allowing use of huge amounts of new spectrum is another way technologists and policymakers are working to eliminate scarcity. The U.S. Federal Communications Commission, for example, is getting ready to release 39 GHz of new communications spectrum, including between 7 Ghz and 14 GHz of unlicensed spectrum.

The only issue is real-world deployment, as signals in the millimeter wave region have propagation issues, compared to radio signals below 1 GHz, for example.

In a recent test, millimeter wave signals at 73 GHz traveled more than 10 kilometers in a rural setting, even when a hill or knot of trees was blocking their most direct route to the receiver, using radios drawing less than one watt of power.

Keep in mind that, until recently, frequencies in such ranges could not be deployed commercially, as signal propagation was too limited. But advances in Moore’s Law mean we can use sophisticated signal processing to create much-better radios, receivers and modulation techniques, allowing us to commercially use such millimeter wave frequencies for the first time.

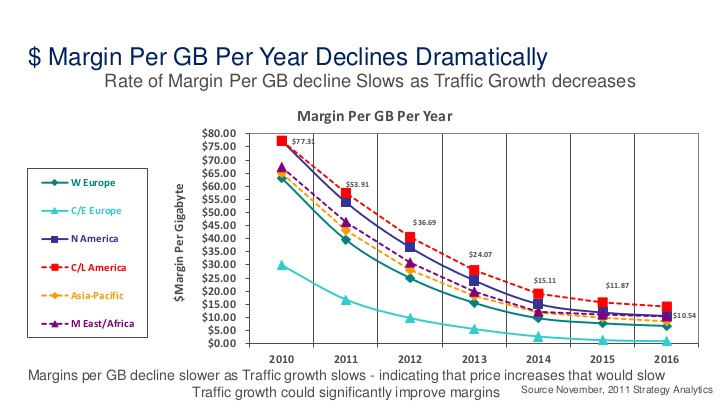

![Figure 2: Revenue per gigabyte of mobile broadband traffic, worldwide, 2011–2016 [Source: Analysys Mason, 2011]](https://lh4.googleusercontent.com/lqWQtnD67pxiXbmGP0nUnk9mLe9QlgiD-1yxOVDvsncYChctSzUST4DtkKA4OxcA_U2CRINrS6wWL-VcPfeEuZDupeNK5j0vd3R283Ig12QPi8qkGM2E9Gptf5Z0NarOu9Af4I6C)