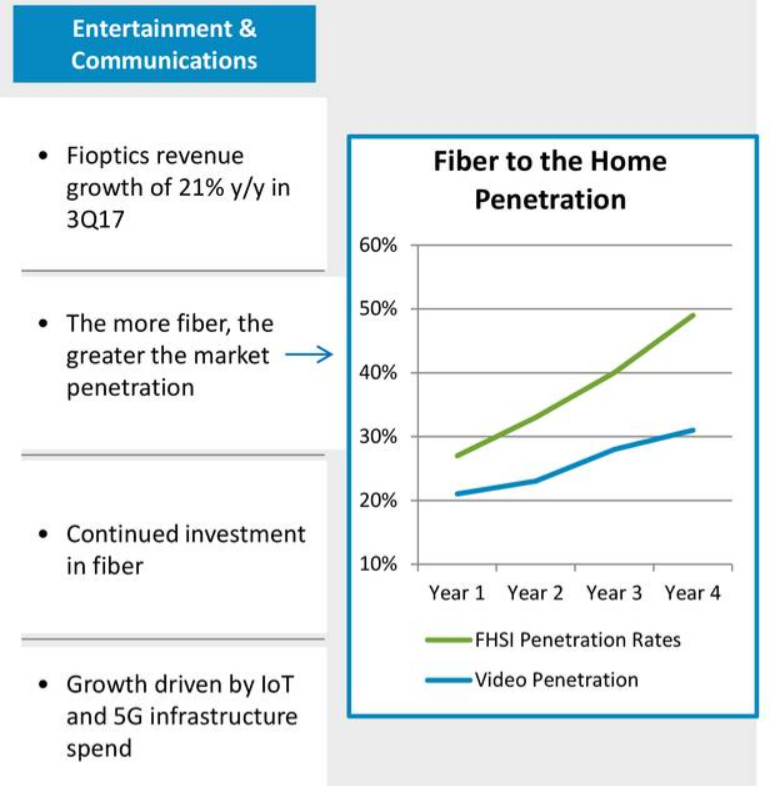

There is good and bad news in Cincinnati Bell’s latest report on its fiber to home adoption. In the first year of marketing, Cincinnati Bell gets about 30 percent of customers to buy. After about four years of marketing, the company seems to get about 50 percent adoption.

So the good news is that fiber to home internet access seems to compete well with cable modem services, after a few years, in terms of market share. In a two-provider market, the company roughly splits the internet access market with cable operators.

The bad news is that no telco yet has been able to demonstrate that its fiber to home efforts, or fiber plus other access platforms, are able to take market share leadership from cable companies.

In rough terms, the upgrade to fiber to home networks allows a telco to battle back to splitting the market with cable, instead of losing share to cable.

There appears to be additional upside in linear video revenue, though some might question the magnitude of those contributions, long term.

So though there are other ways to monetize such investments, the cautionary note is that even with high-performance FTTH networks in place, about the best any telco has been able to show so far is an ability to split the internet access market with cable.

No telco has shown an ability to dominate that market, after upgrading to FTTH. In the future, the business case could be challenged to a greater extent if new rivals emerge. Independent ISPs and mobile substitution are the prime examples.

If a new provider is able to gain 20 percent market share, that would limit telco and cable share to a theoretical maximum of 40 percent each. Some ISPs believe they will routinely do better than that, gaining perhaps 30 percent market share. Ting believes it can get as much as 50 percent share.

Calculating share can be difficult, as these days, “revenue generating units” often are the metric used to derive market share. And RGUs are different from “homes” or “locations.” EPB, the poster child for municipal networks, offers voice, video and internet, and claims 45 percent market share.

But it does so by counting RGUs and comparing that to homes in the service territory. Internet access share is likely closer to 27 percent.

Still, the point is that, in a growing number of consumer markets, there might be three sustainable suppliers, not just two. That will have important ramifications for potential market share.

The larger point is that, in a two-supplier market, FTTH seems capable of allowing a local telco to get as much as half the market for internet access services. That drops in a three-provider market.

FTTH really does help. But how much it can help depends in part on the number of contestants in the market.