In the internet era, where the expected price is "free," prices north of zero might be one reason why many people complain about linear subscription video prices. There is a big difference between $10 a month for Netflix and $80 for linear video, even if the products are not full product substitutes.

It is hard to tell whether perceived value or price anchoring are bigger drivers of dissatisfaction with linear TV services, even if the stated reasons for unhappiness tend to center on “customer service” issues, in addition to price.

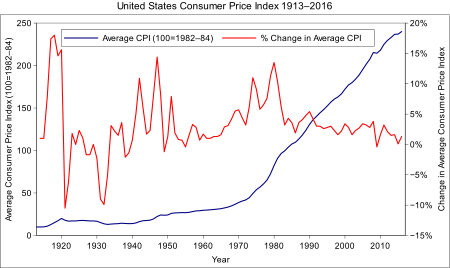

People often complain about price increases for cable TV services that go up more than the general level of inflation. Yes, that is an issue. But consumer prices have been climbing since 1970 or so.

I cannot remember a time (over three to four decades) when consumers actually reported “liking” their cable TV services. Most often, they tend to rank them very low, when compared to most other consumer products.

These days, there are differences between providers. In recent years, telco TV and satellite TV services actually have produced more satisfaction than cable TV video services.

But the service as a whole still ranks quite low, along with internet access. Perhaps price anchoring explains some of the unhappiness. Most children growing up these days experienced internet access, mobility and video as “being free,” since their parents paid for those services.

So the anchoring price is “free.”

On the other hand, many adults who have been buying internet access for decades might have distinctly-different price anchoring experiences.

I recall paying AOL perhaps $15 to $20 a month for 56 kbps dial-up access using the voice line I already was buying.

I can remember paying more than $100 a month but less than $200 a month for a 756-kbps internet access connection. Recall that about 1996 a T-1 line supporting 1.5 Mbps cost as much as $2500 to $3000 a month.

Now I expect to pay $50 or so for 100 Mbps. So my price anchoring is $150 for 756 kbps in the past and now 100 Mbps for about $50 a month.

That is a different set of expectations from many others who have moved from “free in the past” to $50 a month now.

Perhaps the same experience now anchors pricing expectations for potential customers who are moving from “free” to $80 a month.

So I suspect, “value” explains the hostility many single people seem to feel about buying any linear video product (“cable TV”). In other words, the price-per-user is far lower, in a four-person family, than in a single-person household.

In other words, an $80 a month subscription “costs” $80 per viewer in a single-family household, but only $20 per viewer in a four-person household. Though use of streaming services is growing in all age brackets, that might be one reason why families, larger households or households headed by older persons tend to buy linear video streaming services at higher rates.

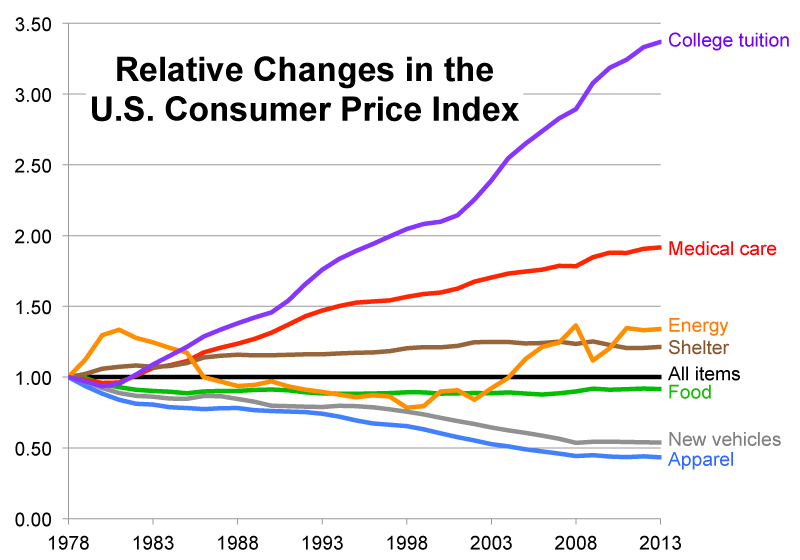

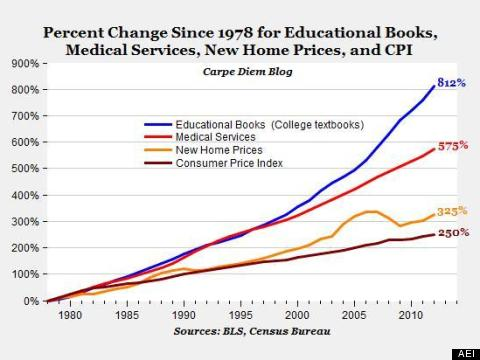

Also, despite the fact that linear video prices have risen faster than the background rate of inflation, lots of other products have risen at “above inflation rates” as well.

Consider the cost of college educations.

Medical care and housing are other products whose prices have increased more than the general level of inflation, as well.