Virtually no observers of the Western Europe connectivity business would challenge the notion that the business model is challenged. Typical complaints include consumer resistance to pay for connectivity; competition that is ruinous and government policies that incentivize competition more than investment.

Infrastructure financing was a significant theme of connectivity provider and regulator talks at MWC Barcelona, as you would expect.

The argument normally is phrased as a matter of “fairness,” a handful of hyperscale app providers “causing” more than half of all data usage by an ISP’s own customers. But that matter also can be looked at through the lens of the way access providers always have compensated each other for traffic imbalances.

Keep in mind it always has been the networks that compensate each other. Think back to the say connectivity networks used to work in the voice era. Calls necessary involved at least two parties and locations.

Resources were consumed on each end of the connection. In most cases, the charging model was “calling party pays,” with a healthy dose of “both parties earn revenue.” Though the calling party paid for long distance charges, the terminating party also was paid for use of the network.

In the era of internet content delivery, one has to ask “who is the calling party?” Is it the ISP customer who asks for delivery of content? Or is it the content owner who responds to a consumer’s or customer’s request? Is the “request” a different session from the content delivery? Or is the content delivery a response to the calling party’s request?

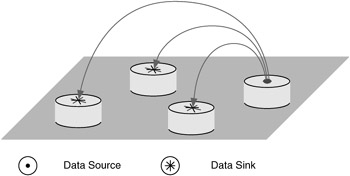

In other words, are we talking about “fairness” or “calling party pays?” And what is the traffic source and sink?

soruce: flylib

It might seem obvious that a content provider is the “source” while the requesting subscriber or user is the “sink.” But that transaction or session only happens because a customer or user of one ISP has asked for that content from an app provider on another network.

In other words, which party placed the call? And which charging method should apply? It’s complicated because there is no internet access equivalent to the call “minute of use.” There is no rating system in place we can use to track and then allocate network usage charges when sessions and data flow between ISP domains.

In an era where networks mostly are used for content delivery, asymmetrical traffic demand is assumed.

Think back to the era when network traffic was mostly voice. By definition, traffic flows were nearly symmetrical. No matter which party called, and which party was called, capacity resources were virtually identical. It did not matter which party talked, and which party listened. Network resource consumption was essentially identical on each end.

In principle, there are three ways to account for usage by customers on two different networks. The calling party can pay; both parties can be paid or the receiving party can pay. The only other pattern is that a third-party sponsor pays (toll free calling, for example).

In the fixed networks business the general pattern has been calling party pays. In the mobile business both parties have paid, in the form of usage allowances being depleted on both ends. And calling parties have paid for toll charges.

In the internet access business, the general pattern has been both parties pay, in the form of usage allowances that are paid for and consumed. Proposals to tax a few hyperscale app providers retain the “both parties pay” scheme, but also add a new layer of “some app providers also pay.”

Many analogies could apply. Placing a long distance call might be one analogy. Even when resources are used on both ends, it is the caller who pays the charge. Applied to internet content delivery, it is the ISP customer who invokes the data delivery who might be viewed as the entity that pays.

The other approach--receiving party pays--only applies for special circumstances similar to a “collect call,” where the called party agrees to pay the charges normally paid by the party placing the call.

The proposal to tax a few hyperscalers is equivalent to collect-call billing procedures, where the party initiating the call is not billed, but the party at the other end is billed instead. One might say that proposals to tax a few hyperscalers are a form of billing similar to the “collect call,” where the calling party is not billed. Instead, charges are borne by the called party.

That is not to say such practices are inherently flawed. It simply is to note that the “both parties pay” is the most-widely-used pattern for mobility networks, even when calling party pays also is used and collect calling is conceivable.

Even if we agree that calling party pays is reasonable, who is the calling party? Connectivity provider calls for payments by a few hyperscalers are more akin to “collect calling.”

That might seem workable to many. But the additional charges borne by the entity paying for the collect call still must account for such charges in their business models. And those higher costs will be borne by business partners, retail customers or users.

Gains by ISPs will be offset by losses by content or app providers. So higher costs will accrue to advertisers, sponsors, retailers and users and subscribers of such services. There is no “free lunch.”