Comcast says it will lose about 100,000 home broadband accounts in the fourth quarter of 2024, a troublesome statistic given that service’s past-decade role in fueling company revenue growth.

By most estimates, the U.S. cable operators will lose market share to other contestants to 2030. The issue is “to whom” the losses will occur. By volume, the shift to telcos is likely to be the biggest. Satellite access might gain, but the magnitude remains unclear. Share held by third-party independents might not change.

The issue is growing competition for new fixed wireless services on one end of the demand spectrum, plus fiber-to-home services on the other end. Put simply, fixed wireless seems to be taking market share from cable services among customers content to buy services offering 100 Mbps to 200 Mbps of downstream bandwidth, while FTTH is taking share among customers who want 1 Gbps or faster, and sometimes more upstream bandwidth.

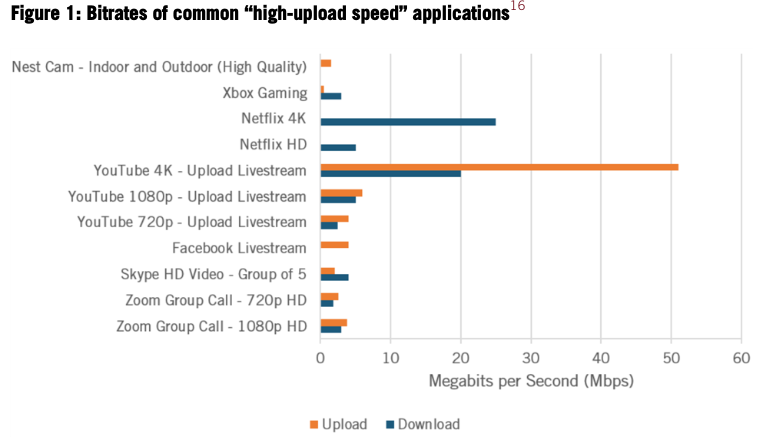

In my own case, I can get around 1 Gbps from both my hybrid fiber coax provider and a FTTH provider. That isn’t the issue. The HFC upstream runs at about 17 Mbps. The FTTH connection is reliably operating at 940 Mbps.

And the point is not that I “need” 940 Mbps upstream. I don’t. The point is that upstream performance is 55 times greater for the FTTH provider than the HFC provider, at zero cost premium.

For that matter, I don’t “need” 1 Gbps in the downstream direction, either. The point is that I wouldn’t consider buying any service operating at speeds less than 1 Gbps. It is not a matter of “need” but of preference or “want.”

Somewhat ironically, U.S. cable TV operators face almost the same issues as do telcos when pondering upgrades of their legacy networks. Traditionally, telcos have had to fund a complete replacement of their copper access networks with fiber-to-home platforms to support broadband services.

And telcos have generally tried to be rational about the capital expenditures, generally deploying FTTH in greenfield areas (new home construction, for example). But that might only represent about one percent to two percent of housing locations per year. At that rate, it will take quite some time to complete a full transition to FTTH.

Cable operators face the same dilemma.

Telcos also have justified FTTH upgrades in neighborhoods where demand is greater and willingness to pay is higher. Cable operators might make the same decisions.

And much hinges on changes in customer demand for symmetrical bandwidth and faster speeds, as there is a point where HFC cannot compete with FTTH (perhaps at about 10 Gbps). That might give cable operators about a decade of running room before a network replacement is required.

That might assume that “typical” U.S. home broadband speeds reach 1 Gbps by perhaps 2026, with upgrades beyond that to 3 Gbps to 10 Gbps over a decade.

But that also assumes the key issue is downstream bandwidth, not “symmetrical” or “more nearly symmetrical” bandwidth. Though most observers arguably do not believe upstream bandwidth symmetry is a huge issue for the near future, its importance seems likely to grow. The issue is whether demand for symmetry grows slowly or faster.

Market demand for products sometimes is not based on “need” but “want,” and some users might already make buying decisions as though symmetrical bandwidth is preferable, even if no application currently requires it, and even if multi-user demands do not require it.

So bandwidth demand beyond the capabilities of the HFC network will force a platform upgrade that telcos already have been facing with the upgrade to FTTH from copper access, even if HFC has a more-evolutionary path remaining, before a full platform shift is necessary.

Cable operators have been able to gradually and incrementally upgrade their once-copper networks to hybrid networks featuring fiber backbones and retaining copper distribution. But a disruption is coming. No matter how far cable operators extend fiber closer to end user locations, increasingly more-difficult adaptations are necessary.

Traditionally, the simple remedy was to replace coaxial cable in the backbone with fiber, which was fairly simple, as the rest of the network remained untouched. But moving in the direction of more-symmetrical bandwidth is tougher, requiring revamping all active elements of the copper network.

High-split hybrid fiber coax networks allocate up to 204 MHz for upstream traffic, compared to only 42 MHz (USA) or 65 MHz (Europe) in sub-split networks. That represents as much as five times more upstream capacity compared to 42-MHz sub-split upstreams.

But even a high-split network will not be able to support symmetrical bandwidth, as FTTH systems now do. So long as customers do not demand symmetrical bandwidth, perhaps that is not an existential issue.

But if the market shifts to a preference for symmetrical bandwidth, cable operators will, at some point, have to invest quite a bit more than they presently do in network capital investment, as they will essentially have to replace HFC with FTTH access networks.

There also is a new wrinkle, namely that some demand for lower-bandwidth connections apparently has grown for fixed wireless alternatives.

We can see that demand shift in statistics on home broadband net gains and losses.