We might agree that defining “artificial intelligence” is difficult. But lots of common and foundational concepts likewise are very-difficult to impossible to define in ways that most of us would accept. We are simply going to learn to use the tools without being able to define it with rigor and high degrees of shared meaning, in all likelihood.

Wednesday, January 8, 2025

Even if We Can't Define "AI," We Can Use It

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, January 7, 2025

Linear TV Enters Early Stages of "Harvesting"

Since all observers agree the linear TV (“live TV”) subscription business is dwindling, we should expect consolidation of service providers, as that happens in virtually all declining industries. The objective for such moves is to reduce cost and harvest profits for as long as possible.

The most-recent example is the new joint venture combining live TV assets owned by Disney (Hulu+Live TV) with Fubo, where Disney will own 70 percent of the asset, but Fubo leaders will manage the business.

Both the Fubo and Hulu+Live TV brands will continue to exist and be marketed.

But that will not be the end of the consolidation, as other assets eventually are combined. The logical combinations (assuming antitrust issues are addressed) are cable assets merging or satellite assets being combined. The other logical move are combinations of streaming assets.

Just as discussions about future mergers of linear video programming assets (“cable channels”) now are happening, so too will distributor mergers have to happen, as the market continues to shrink.

Like it or not, linear video content and distribution assets now are cash cows to be milked as the category inevitably declines.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Wipro Survey Suggests Business Leaders are Moving to Cloud-Based AI Operations

A Wipro report on cloud computing finds enterprise leaders are moving towards cloud-based platforms for artificial intelligence use cases. That probably makes sense to many as projects move from pilot stage to full implementation, which requires scaling the compute infrastructure.

While not absolutely confirming the magnitude of hyperscale cloud computing leader investments in AI infrastructure, the survey of some 500 U.S. and European business leaders tends to confirm the need for additional infrastructure investment to support AI operations.

Microsoft, for example, has announced it will spend about $80 billion on AI infrastructure in its 2025 fiscal year (ending in June 2025) after spending about $53 billion on data center infrastructure in 2023 and 2024.

It has been estimated that Microsoft, Meta, Amazon, Alphabet and Apple alone invested up to $210 billion in infrastructure (including AI infra) in 2024 alone.

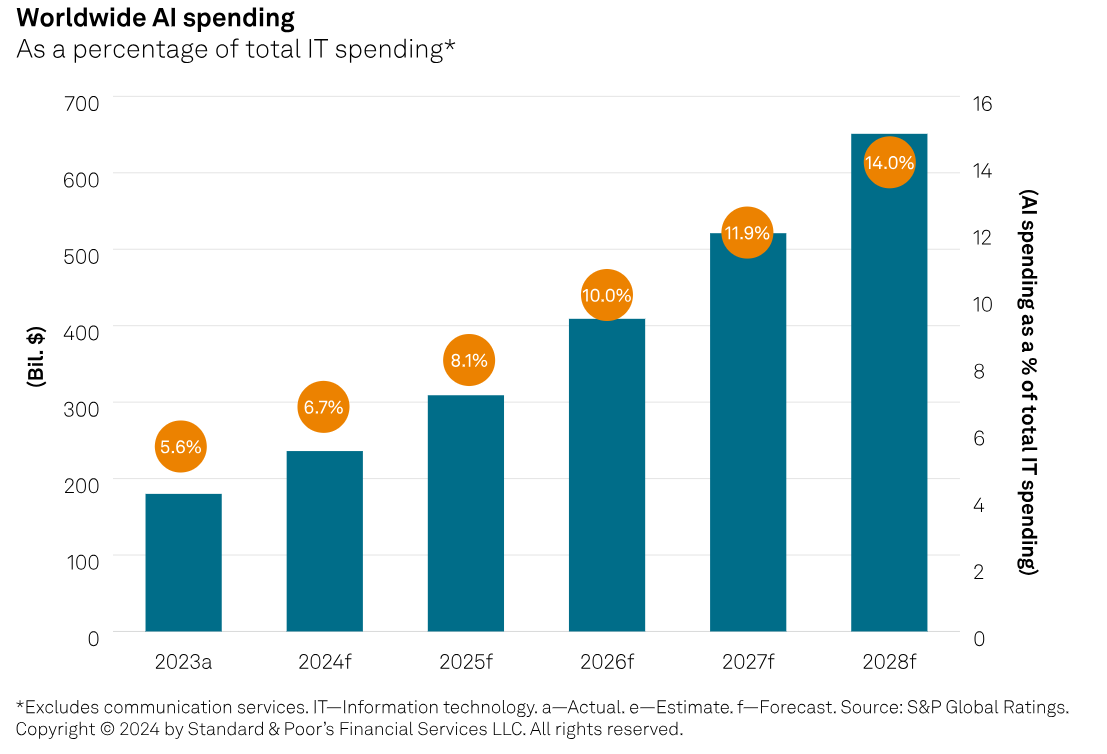

S&P Global Ratings expects market annual spending for artificial intelligence, including traditional AI (machine learning) and generative AI, will expand to nearly $650 billion by 2028 from less than $200 billion in 2023, a compound average growth rate in the high-20 percent area.

The agency projects the AI market will account for nearly 15 percent of total global IT spending by 2028, including semiconductors, hardware, software, and IT services.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, January 6, 2025

AI Capex by Hyperscalers is a Reasonable Bet on Market Growth

While there is no guarantee that the huge capital investments by hyperscale cloud computing providers will pay off, most of us might agree that enterprises are going to be spending more on generative artificial intelligence in coming years, as seen in facilities and servers.

Global spending on data center construction is forecast to reach at least $49 billion by 2030.Capital spending on procurement and installation of mechanical and electrical systems for data centers is likely to exceed $250 billion by 2030.

On the demand side, cloud computing sales are expected to rise to $2 trillion by 2030, with generative AI accounting for $200-300 billion (10-15 percent) of that spending by enterprises.

The total addressable market for cloud services (including AI "as a service") is projected to grow at a 22 percent compound annual growth rate from 2024 to 2030.

S&P Global Ratings expects market annual spending for AI, including traditional and generative AI, to expand to nearly $650 billion by 2028 from less than $200 billion in 2023.

So, in principle, assuming much of the actual server hosting for those applications can be captured by the hyperscalers, the investments will prove financially rewarding.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sunday, January 5, 2025

If Time is Money, and IT Saves Time, is that ROI?

A survey by IDC commissioned by Microsoft focusing on ways Copilot saves time and therefore increases productivity. It’s a good example of the familiar information technology “return on investment” exercise where we assume “time is money” and that new “technology saves time.”

By definition, such methods cannot capture benefits such as

Improved accuracy and quality of work

Increased employee morale and satisfaction

Enhanced customer service

Better decision-making.

But those metrics are likewise hard to quantify for knowledge or office work. But advocates keep trying.

Lumen Technologies estimates Copilot saves sellers an average of four hours a week, equating to $50 million annually. In healthcare, Chi Mei Medical Center doctors now spend 15 minutes instead of an hour writing medical reports, and nurses can document patient information in under five minutes.

Pharmacists are now able to double the number of patients they see per day. In retail, AI models help Coles predict the flow of 20,000 stock-keeping units to 850 stores with remarkable accuracy, generating 1.6 billion predictions daily. Microsoft provides 200 such examples.

If you have been around such productivity estimates before, you know that the estimates are produced fairly simply: estimate time saved by workers, then multiply by the salaries of those workers.

If you have worked in sales of information technology products to business customers, and have made such arguments yourself, you also know that buyers discount such claims.

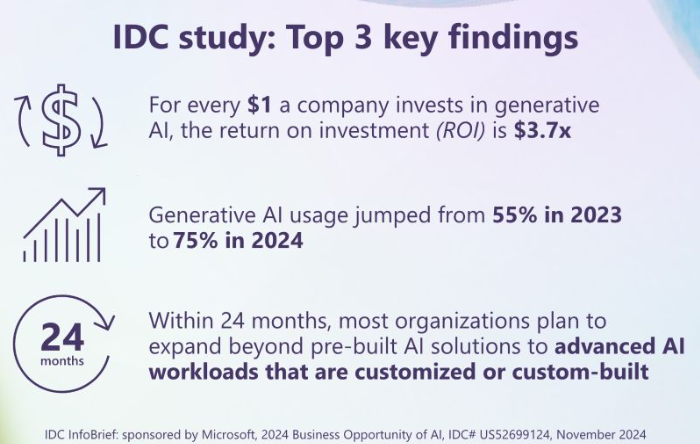

IDC says generative AI usage jumped from 55 percent of entities using it in 2023 to 75 percent in 2024.

For every $1 a company invests in generative AI, the ROI is $3.7 times, while some leaders using generative AI claim a returns as high as 10 times.

On average, AI deployments are taking less than eight months and organizations are realizing value within 13 months, IDC reports.

The ROI of generative AI is highest in financial services, followed by media and telecommunications (including mobility), retail and consumer packaged goods, energy, manufacturing, healthcare and education.

The primary way that organizations are monetizing AI today is through productivity use cases.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, January 4, 2025

Will Non-Fossil-Fuel-Produced Electricity Rates Fall?

Many studies argue that the cost of electricity for consumers will fall as the transition to non-fossil fuels gains traction, but since 2000, consumer electricity rates in the U.S. have generally increased. In fact,electricity rates in the United States have increased significantly since 1950, despite some periods of relatively low or stable rates.

Despite that track record, advocates continue to argue that a switch to non-fossil fuels will lead to lower prices.

Wholesale electricity prices are projected to decrease by 20 percent to 80 percent in the medium term (by 2040) in the United States, depending on the region, according to Brookings researchers.

Other advocates argue that U.S. households could save an average of $500 a year on energy costs from non-fossil-fuel sources. And some advocates say cheaper energy is possible in the G7 countries by 2025. I doubt that can be claimed to be realistic at this point.

In fact, there is no clear evidence that G7 country energy costs have declined since 2000, or even since 1950. In fact, the information suggests that energy costs have generally increased:

Electricity investments within the G7 are projected to triple in the coming decade, indicating rising costs rather than declining ones 1.

Household spending on electricity is expected to increase, although this increase is projected to be offset by declines in spending on coal, natural gas, and oil products 1.

The share of GDP spent on energy in G7 countries is expected to decline from around 7% today to just over 4% in 2050, but this is due to economic growth rather than falling energy costs 1.

While total household energy spending in the G7 has not declined since 2000 1.

The data shows that coal power capacity in G7 countries peaked in 2010 and has since fallen, but this doesn't necessarily translate to lower energy costs for consumers 2.

I find that energy prices for consumers will fall as the transition to non-fossil fuels is made to be questionable.

Even granting some short-term price increases to create new infrastructure, the theory that long-term prices will drop seems questionable. Serious people used to argue that nuclear power would create such plentiful supplies that it would be “too cheap to meter,” and that never happened.

One might note that many of the claims about future benefits come from studies conducted or sponsored by the IEA, hardly a disinterested industry source.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...