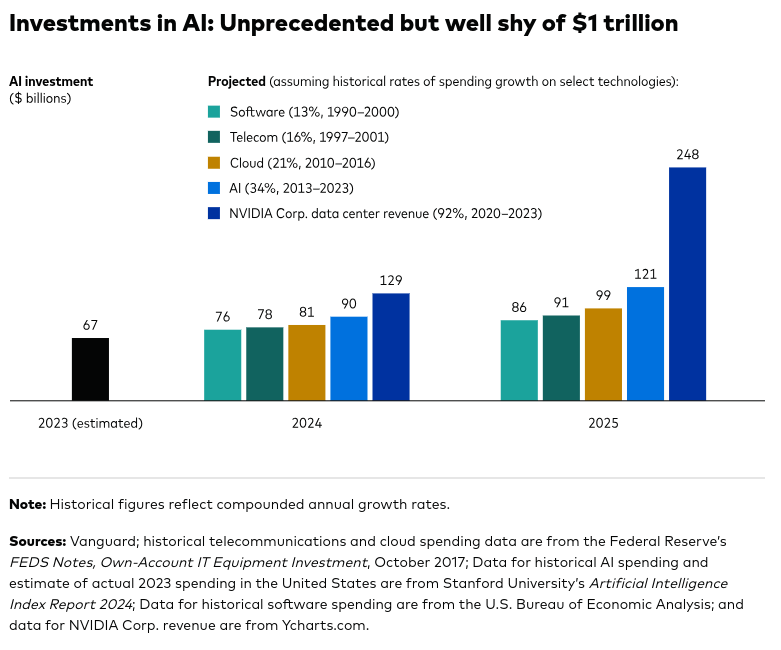

Is it possible some estimates of capital investment in artificial intelligence are inflated? Yes. According to Stanford University’s Human Centered AI institute, about $67 million was invested in AI in 2023.

“To project such spending in the near term, we grossed up last year’s investments in AI by various annualized rates of growth ranging from 13 percent to 34 percent,” says Joe Davis, Vanguard global chief economist. “Those rates of growth would leave AI spending this year and next in the $76 billion to $121 billion range.”

That’s significant, but nowhere near the “$1 trillion” some have estimated will be spent on AI capex over the next few years.

Or consider estimates of AI capex spending by a few of the big hyperscalers. To be sure, those firms are only some of the firms expected to make AI capex investments.

Also, a significant portion of the AI capex is likely to be shifted from existing information technology budgets, and might not represent incrementally-higher spending. That is virtually certain to be the case for most enterprises making AI capex investments, as most enterprise or smaller business IT budgets do not change all that much annually, with increases, if any, normally in single digits.

Providers of “AI as a service” will have to make unusual investments, to be sure. But business users of AI will not do so.

So the big change in AI capex is likely to be driven by a relatively few hyperscalers.