Most “new source of revenue” growth opportunities available to fixed and mobile service providers are incrementally important. Very few are expected to produce huge amounts of revenue in the near term.

On the other hand, most of the revenue volume will come from tweaks to the existing revenue model (consumer phone service). Perhaps surprisingly, 5G fixed wireless could be one of the biggest near-term contributors to new service revenue.

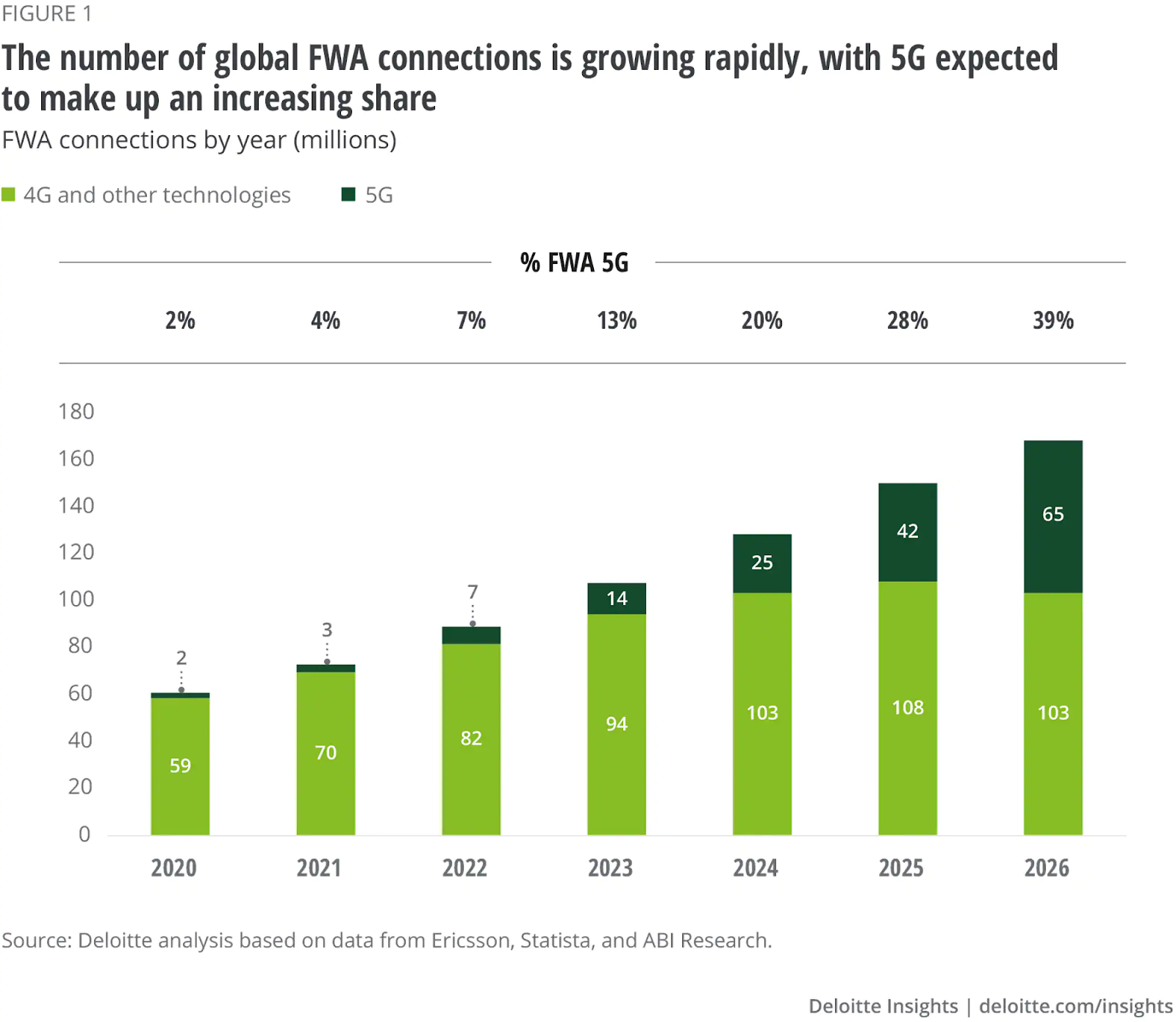

Deloitte Global predicts that the number of FWA connections will grow from about 60 million in 2020 to roughly 88 million in 2022, with 5G FWA representing almost seven percent of the total. Most of the installed base consists of 4G connections and it will take some time for 5G to overtake 4G.

By 2026 there could be 160 million FWA accounts in service. At an average monthly cost of $20, that generates perhaps $38.4 billion in service revenue. At $40 per month, FWA generates perhaps $76.8 billion in service revenue.

The total fixed network broadband installed base is expected to be about 1.75 billion accounts in 2027. So FWA will represent about nine percent of total fixed network broadband accounts.

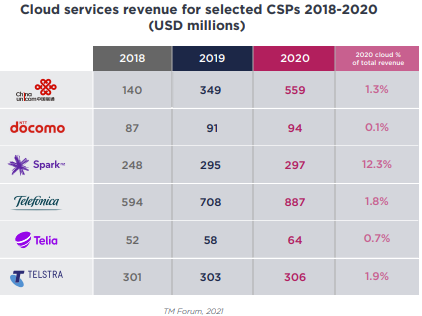

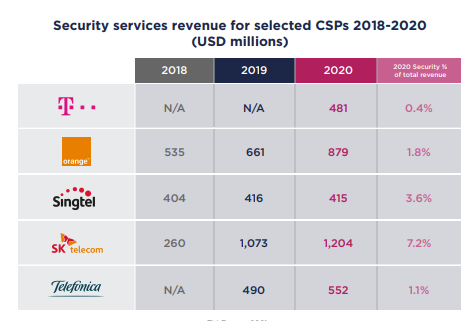

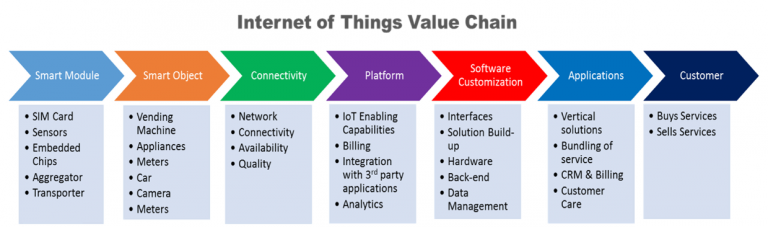

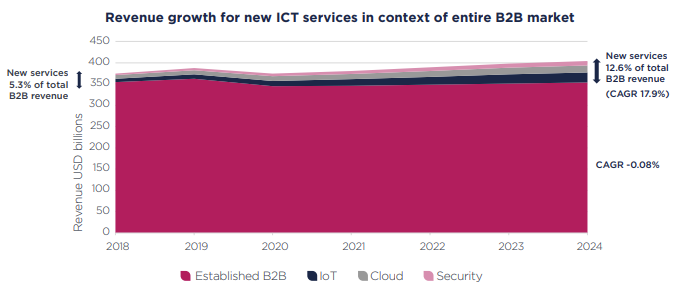

Compare that with projected revenues from other more-touted services such as internet of things, edge computing and security. Those three services will in 2024 amount to about 12.6 percent of total business service revenue of $400 billion globally.

So security services, IoT and edge computing combined will amount to about $50 billion in annual revenues by 2024. If cumulative growth rate for those services is 17.9 percent, then 2026 revenue might be about $70 billion globally.

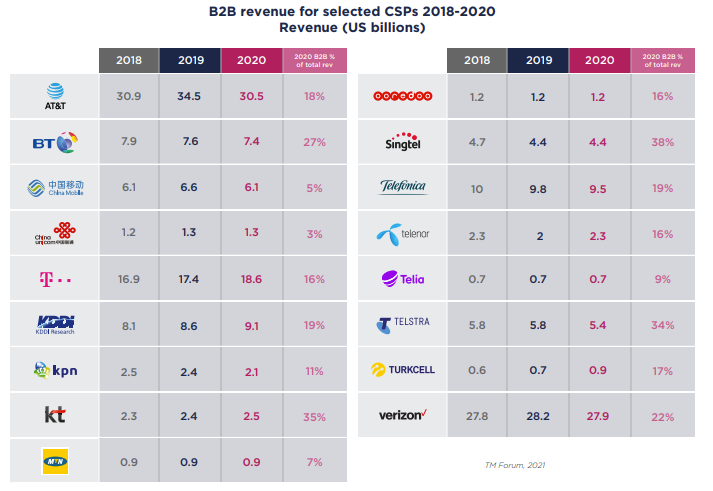

If global telecom service revenue is about $1.6 trillion in 2025, and consumer revenues are about 65 percent of total service provider revenues, then business revenues could hit $560 billion in about 2025 or 2026.

If you assume consumer services in 2025 or so will be about 60 percent of total revenues, then business revenues could be as high as $640 million.

How much of that could come from new sources such as edge computing, security and IoT is the issue. If those new sources are 12.6 percent of total business revenues, then existing business services will represent 87 percent of total revenue, or anywhere from $330 billion up to $556 billion.

In other words, improving revenue from existing services still drives most of the possible business revenue improvement.

It is possible that fixed wireless access is a bigger business than edge computing, security and IoT in 2026. At the low end of the FWA estimates, fixed wireless might still be bigger than any of the other new services individually.

The point is that we tend to overlook the new revenue impact of FWA, focusing on the more-touted areas of security, IoT or edge computing. But FWA is possibly going to be a bigger revenue contributor.

While fixed wireless will grow about 19 percent per year to 2026, 5G FWA connections will grow at an annual cumulative growth rate of nearly 88 percent, over the same period, Deloitte Global says.