Beyond that, it remains unclear what revenue contributions might in the future be made by entirely new lines of business. But Comcast’s second quarter 2012 earnings report suggests the upside potential and downside risks.

Also, the latest Solon Survey of European cable operators illustrates a couple salient points about the near term growth drivers for North American and European cable operators. Wireless appears to be a bigger factor for European cable operators, while Comcast’s approach now suggests content will be a bigger source of revenue for the larger U.S. cable providers.

In the near term, European cable operator growth now comes from broadband access, mobile services and business-to-business services.

The key trends are the importance of mobility and services aimed at business customers, which In the 2009 survey were not firmly embraced by cable operators in Europe.

By 2011, sentiment had changed, with operators across Europe highlighting the importance of

commercial and mobile segments in driving near term revenue growth.

On average, cable operators expect to double the share of revenues generated through mobile offerings, while the revenue contribution from business and wholesale activities is forecast to increase by approximately 33 percent. For a business historically serving the consumer segment, the expansion of services to business and enterprise customers is significant.

By 2014, a typical European cable operator will be earning 12 percent of its revenues from business customers. Some cable operators, though, already earn more than 30 percent of total revenues from B2B services.

European cable operators surveyed expect revenue growth of over five percent per year until 2014 and further EBITDA margin expansion by two percentage points up to 48 percent, on average, to 2014.

In large part, that is due to gains in broadband access revenue, which remains the main source of revenue growth for European cable operators, the report suggests. In fact, Solon attributes broadband access revenue for a rebound in operator average revenue per user, which had been dropping.

Revenue earned by offering or higher access speeds, at an average broadband access ARPU of approximately 20€ per month, is the primary reason ARPU now is stable, the Solon report indicates.

Comcast’s revenue, on the other hand, now has tipped towards content. Comcast video revenues have shrunk to about 52 percent of total Comcast revenue, while other access network services now contribute 48 percent, and are growing.

At some point, Comcast will earn less than half its revenue from its legacy video entertainment business. And that is to focus only on Comcast’s “local access” business.

In fact, including the NBC Universal contributions, it already is true that Comcast earns less than half its total revenue from cable TV distribution. In fact, cable TV video distribution operations now account for only 33 percent of total Comcast revenue.

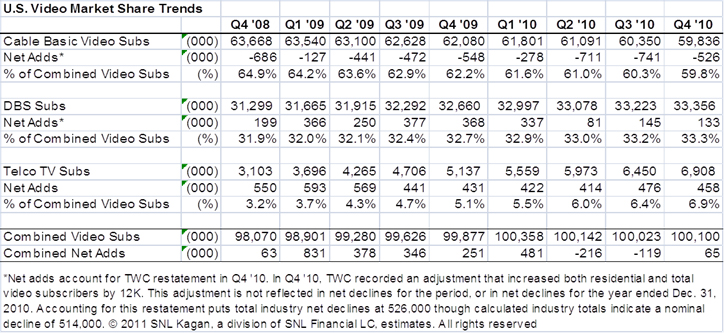

For anybody who has followed the U.S. video entertainment market for some decades, that U.S. cable operator video penetration is as low as 44 percent of TV homes is a shocking statistic. There was a time when penetration was as high as 70 to 80 percent of homes in some areas.

Competition from satellite and telco competitors is the reason for the sharp reversal.

Some 97 percent of U.S. homes own a TV, and about 90 percent of all U.S. homes buy a subscription TV service.

Telco IPTV penetration on a global basis, measured agains the installed base of worldwide broadband subscribers, reached 15 percent in the first quarter of 2012, representing 67 million subscribers and eight percent of the world’s 812 million video entertainment service subscribers, according to TeleGeography.

North American telcos, led by Verizon and AT&T, have succeeded in selling IPTV service to almost 40 percent of their broadband subscriber base. That is not to say telco TV now reaches 40 percent of homes. That statistic means the tier one telcos are selling video entertainment to 40 percent of their customers who buy broadband access.

Since telcos have almost half of all broadband customers, and since broadband is purchased by about 80 percent of U.S. households, you can roughly estimate that telcos now sell video services to perhaps 20 percent of U.S. households.

But keep in mind that telcos are not able to sell video to many locations, using their fixed networks, for technology reasons. Where they can do so, market share could be in the 30 percent range.

Generally speaking, getting a video customer means taking that customer away from a cable TV or satellite TV provider who already had the customer, as household penetration of subscription TV is over 80 percent. The market, in other words, is saturated.

There are some important implications. You might well argue that 40 percent video penetration of a service provider’s own customer base is “about as good as it is going to be,” when strong cable TV and satellite TV competitors own the rest of the customers, and when taking a customer therefore is tough.

In any market with three dominant and well-heeled contestants, you might expect an ultimate market share distribution that could easily be split three ways, with any single contestant getting 20 percent to 40 percent share.

If telcos have 20 percent share, could that share double? In principle, yes. If telcos get 30 percent share, could share then double again? Probably not, if the other two contestants (satellite and cable) continue to perform at a high level.

But there is one big change in potential market share structure that long has been speculated, namely a purchase of both U.S. satellite companies by one of the tier-one U.S. telcos. That, in principle, could mean telcos then would have as much as 60 percent share of video service customers.

For the moment, telcos are doing about as well as they can, using only their fixed networks.

{kind=link}

{kind=link}