Constant and significant increases in bandwidth consumption are among the fateful implications of switching from linear TV broadcasting to multicast video streaming. Consider that video now constitutes 52 percent to 88 percent of all internet traffic.

Not all that increase is the direct result of video streaming services. Video now is an important part of social media interactions and advertising on web sites supporting consumer applications, though some studies suggest social media sites overall represent only seven percent to about 15 percent of video traffic consumed by end users.

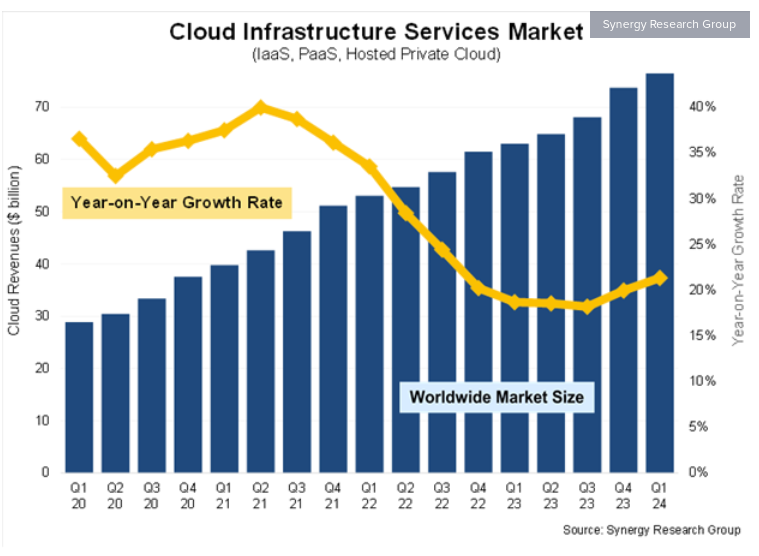

Also, there is some amount of internet video traffic between data centers, not intended directly for end users, possibly representing five percent of global internet traffic.

Study | Date | Video Traffic Share (%) |

Cisco Annual Internet Report (2023) | Dec 2022 | 88% |

Sandvine Global Internet Phenomena Report (Q3 2023) | Sep 2023 | 83% |

Limelight Networks State of the Real-Time Web Report (Q3 2023) | Oct 2023 | 76% |

Ericsson Mobility Report (Nov 2023) | Nov 2023 | 72% |

ITU Global Video Traffic Forecasts | Feb 2023 | 70% (2022) |

Ookla Global Video Report (Q2 2023) | Aug 2023 | 65% |

Akamai State of the Internet / Security Report (Q3 2023) | Oct 2023 | 60% |

Statista: Global Internet Traffic Distribution by Content Type (2023) | Oct 2023 | 58% |

GlobalWebIndex Social Video Trends Report (Q3 2023) | Sep 2023 | 55% |

Juniper Networks Visual Networking Index (2023) | Feb 2023 | 52% (2022) |

Ignoring for the moment the impact of video resolution on bandwidth consumption (higher resolution requires more bandwidth), the key change is that broadcasting essentially uses a “one-to-many” architecture, while streaming uses a unicast architecture.

The best example is that a scheduled broadcast TV show, for example, can essentially send one copy of the content to every viewer (multicast or broadcast delivery). The same number of views, using internet delivery, essentially requires sending the same copy to each viewer separately (unicast delivery).

In other words, 10 homes watching one multicast or broadcast program, on one channel, at one time consumes X amount of network bandwidth. If 10 homes watch a program of the same file size as the broadcast content, whether simultaneously or not, then bandwidth consumption is 10X.

There are some nuances for real-world data consumption, such as the fact that consumption of linear video is declining or the fact that broadcasting uses a constant amount of bandwidth, no matter how many viewers in an area might be watching or not watching.

Study | Comparison | Bandwidth Ratio (Streaming/Broadcasting) |

"A Comparative Analysis of Video Streaming and Broadcasting for Live Sports Events" (2023) | Live sports streaming vs. multicast | 10x - 15x |

"Bandwidth Efficiency of IPTV vs. Traditional Broadcasting" (2022) | IPTV unicasting vs. terrestrial broadcasting | 2x - 4x |

"The Impact of Unicast Video Delivery on Network Traffic" (2021) | Unicasting video vs. multicast video | 1.5x - 3x |

"Comparing the Bandwidth Consumption of Live Streaming and P2P Delivery" (2020) | Live streaming vs. P2P for live events | 3x - 6x |

"The Bandwidth Efficiency of Video Streaming Protocols" (2019) | HTTP streaming vs. RTMP streaming | 1.2x - 2x |

"A Study of User-Generated Video Delivery on Social Media Platforms" (2018) | User-generated video streaming vs. traditional video streaming | 2x - 4x |

"The Bandwidth Implications of 4K and 8K Video Streaming" (2017) | Higher resolution streaming vs. standard definition | 4x - 8x |

"The Impact of Mobile Video Streaming on Network Congestion" (2016) | Mobile video streaming vs. fixed-line streaming | 1.5x - 3x |

"The Future of Video Delivery: A Cost Comparison of Streaming and Broadcasting" (2015) | Streaming vs. broadcasting for future content delivery | 2x - 4x |

"The Bandwidth Efficiency of Video-on-Demand Services" (2014) | Video-on-demand streaming vs. linear broadcasting | 1.5x - 2.5x |

There are other nuances as well. Since a broadcast video stream often is viewed on a television set, it is possible that multiple viewers “share” viewing of the same content. If one TV is receiving a program, and five people are watching, the “single delivery” supports five views.

On a “per viewer” basis, X amount of delivery bandwidth is X/5 for each viewer of the same program.

If five people watch a program of equivalent file size at the same time, data consumption is 5X.

Study | Year | Methodology | Streaming Bandwidth (Mbps) | Linear Broadcasting Bandwidth (Mbps) |

Nielsen | 2022 | Network traffic analysis | 3.1-4.7 (average) | 0.1-0.2 (average) |

OpenVault | 2023 | ISP data analysis | 1.8-2.5 (average) | 0.05-0.15 (average) |

Pew Research Center | 2021 | Survey and network analysis | 2.3-3.8 (average) | 0.1-0.2 (average) |

University of Zurich | 2019 | Network monitoring and simulation | 2.0-3.5 (average) | 0.08-0.18 (average) |

Akamai | 2020 | Global traffic analysis | 1.6-2.8 (average) | 0.04-0.12 (average) |

Sandvine | 2022 | Network traffic analysis report | 3.5-5.0 (peak) | 0.15-0.25 (peak) |

Netflix | 2021 | Open Connect content delivery platform report | 0.5-1.5 (average) | N/A |

BBC Research & Development | 2018 | HbbTV hybrid broadcasting analysis | 1.0-2.0 (combined) | 0.03-0.08 (combined) |

Bitmovin | 2023 | Video encoding and delivery technology report | 0.8-1.8 (efficient encoding) | N/A |

Ericsson | 2022 | Mobile network video traffic report | 0.5-2.0 (mobile average) | N/A |

The point is that the shift from broadcasting (multicasting) to unicast entertainment video was destined to dramatically increase internet data consumption.