Asset flipping in any business is not unheard of, but Verizon’s history with Frontier still seems instructive. In 2010, for example, Frontier Communications purchased rural operations in 27 states from Verizon, including more than seven million local access lines and 4.8 million customer lines.

Those assets were located in Arizona, California, Idaho, Illinois, Indiana, Michigan, Nevada, North Carolina, Ohio, Oregon, South Carolina, Washington, Wisconsin and West Virginia, shown in the map below as brown areas.

Then in 2015, Verizon sold additional assets in three states (California, Texas, Florida) to Frontier. Those assets included 3.7 million voice connections; 2.2 million broadband internet access customers, including about 1.6 million fiber optic access accounts and approximately 1.2 million video entertainment customers.

source: Verizon, Tampa Bay Business Journal

Now Verizon is buying back the bulk of those assets. There are a couple of notable angles. First, Verizon back in the first decade of the 21st century was raising cash and shedding rural assets that did not fit well with its FiOS fiber-to-home strategy. In the intervening years, Frontier has rebuilt millions of those lines with FTTH platforms.

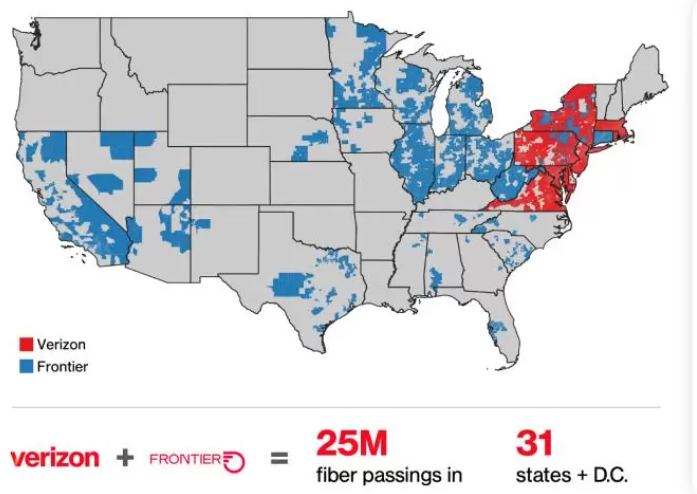

Also, with fixed network growth stagnant, acquiring Frontier now provides a way to boost Verizon’s own revenue growth. The acquisition means Verizon’s FTTH connections will jump from approximately 7.4 million to 9.6 million, a gain of about 23 percent in one fell swoop. And since home broadband is the primary revenue growth driver for fixed networks these days, that matters.

source: Verizon

There are other takeaways. As in the mobile communications business, where Verizon and AT&T, for example, had been focusing on urban footprints and customers, market saturation has forced both firms to plumb rural areas and customers as well as the mobile virtual network operator business and prepaid accounts, where the main focus had been postpaid branded accounts, market saturation has forced the major providers to search in new areas for growth.

As a byproduct, Verizon might, in some cases, be able to leverage its new fixed network assets to support its mobile network as well (fiber backhaul, for example).

It is possible there are other strategic considerations as well. T-Mobile, which started out with zero share of the fixed network home broadband market, now is growing based on its use of fixed wireless services provided by its mobile platform.

But T-Mobile is making its first steps towards adding some amount of fixed network access provided by cabled networks as well. For example, T-Mobile has partnered with EQT, a global investment firm, to acquire Lumos, a fiber-to-the-home platform.

T-Mobile also formed a joint venture with KKR, another global investment firm, to acquire Metronet, a leading fiber-to-the-home provider. That acquisition also will expand T-Mobile’s fixed network home broadband market share.

And while it has seemed unlikely that T-Mobile would contemplate moves such as acquiring Frontier Communications or other firms such as Brightspeed itself, that outcome--at least regarding Frontier--is closed.

On the other hand, the pressure to grow footprint to grow market share remains intact. Brightspeed does appear to have substantial overlap with Verizon’s new fixed network footprint, but duplicated assets might be sold.

And Verizon appears to face little danger of antitrust action were it to acquire additional fixed network assets, given its modest coverage of U.S. homes. By some estimates, prior to the Frontier acquisition,

Verizon homes might have numbered less than 25 million, possibly as low as 20 million.

That is far fewer than top Verizon competitors might claim.

Comcast has (can actually sell service to ) about 57 million homes passed. AT&T’s fixed network represents perhaps 62 million U.S. homes passed.

Charter already passes more than 32 million locations, including homes and businesses.

CenturyLink never reports its homes passed figures, but likely has 20-million or so consumer locations it can market services to.

The point is that additional Verizon acquisitions of fixed network assets, to reach more U.S. homes, might not pose antitrust issues. The Frontier acquisition adds between five million to 10 million potential new fixed network locations (not all upgraded for FTTH, yet, and including business locations). That potentially increases Verizon’s “locations passed” footprint by as much as a third.

Using Verizon’s recent assertion that, after the Frontier acquisition, Verizon will reach 25 million homes, Verizon would still have some ways to go before it passes as many homes as AT&T, Comcast or Charter, its larger fixed network competitors.

Frontier is said to have a network reaching 15 million locations, including homes and businesses. A reasonable guess is that at least 10 million of those locations are homes.

Most of those locations are arguably not good candidates for FTTH investment, which is why firms such as Verizon and Lumen sold off rural footprints in the past.

If Verizon’s “homes passed” footprint, after the acquisition, is only 25 million, there remains room to add more homes by acquisition.

Brightspeed’s network seems to pass about 6.5 million locations. Most are homes, but not all. Assuming 90 percent are residential, that implies less than six million locations are homes. So even adding Brightspeed assets would only bring Verizon up to perhaps 31 million or so homes, still far less than reached by AT&T, Comcast and Charter.

The point is that the strategy of selling off rural assets and re-acquiring them later, once a critical mass of FTTH passings and accounts have been created, seems a logical strategy. Verizon’s cost to acquire the Frontier footprint (not customers, but network passings) is north of $1,000 per location, and possibly in the $1500 per passing range.

Many observers expect that the former Frontier FTTH passings will double within a couple of years. At current take rates, that also implies a potential additional two million or more FTTH accounts being added.

Asset flipping remains part of the connectivity business. But it is rare to see a seller reacquire its sold assets.

{kind=link}