It is official: private equity firm KKR is making a bid to take Telecom Italia private. Said to be the biggest-ever private equity bid for a public telecom service operator in Europe, the $12 billion deal seems to be opposed by Vivendi, which owns 24 percent of Telecom Italia.

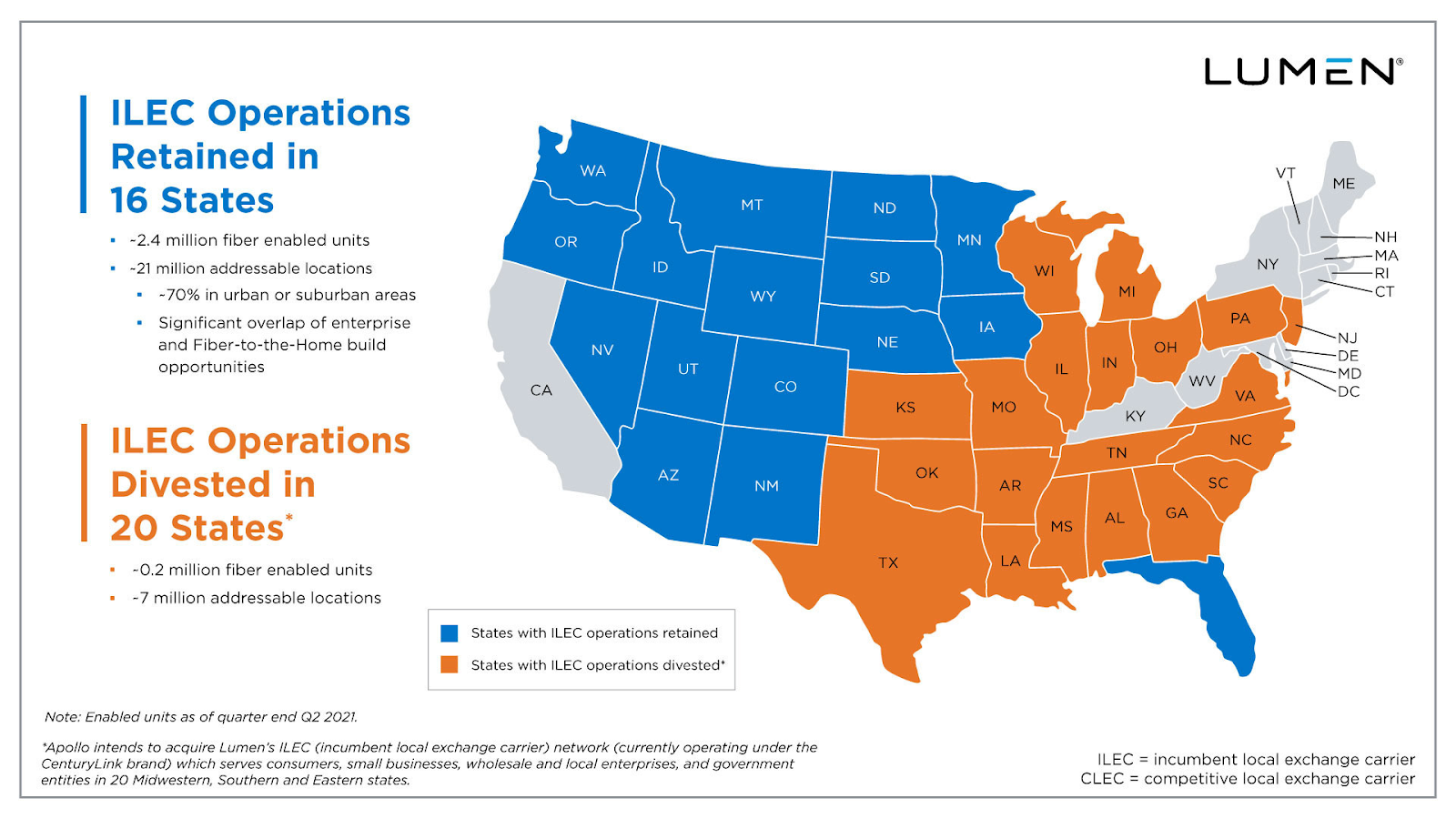

The KKR playbook would normally involve an effort to streamline, rationalize and reposition the assets. KKR is believed to be interested in separating Telecom Italia’s network assets from the retail operations, turning part of TI into a wholesaler of capacity, likely with a heightened optical fiber position, while retail operations are conducted separately, using the wholesale network.

At first glance, the proposed deal looks like a standard private equity deal: buy an underperforming asset, make changes and then sell. But the deal might also reflect another private equity focus: buying infrastructure assets to hold longer term, as an alternative asset.

Perhaps a likely scenario is that KKR hopes to dramatically improve financial performance before selling the asset to an investor that wants the long-term cash flow.

Telecom Italia, for its part, also fits the “go private” scenario: it has high debt and shrinking recurring revenues and profits, arguably impairing its ability to invest in digital infrastructure including fiber to home facilities.

Among the key drivers for telecom privatizations is the perception by asset owners that public markets will not positively reward the firms, in terms of equity valuations, commensurate with their revenues, cash flow or potential growth prospects.

Another key driver is private equity firms with lots of private capital to invest, and assets that offer long-term and predictable cash flows to institutional investors such as pension funds and other entities with long time horizons that view infrastructure assets as equivalents to other long-duration fixed-income assets such as bonds.

Also, asset diversification is another motivation for investors.

There is a good reason why any number of public telecom firms have been taken private, and why others are considering similar moves: high debt, low growth and poor operational performance. And connectivity providers are not the only type of firms facing investment issues.

That is a fairly-common prescription for any public company to be taken out of the public markets by private equity, and many public telco assets fit the bill.

One defining characteristic of infrastructure assets is their monopolistic position. We tend to forget that for most of the history of the industrialized world, much of the funding for large scale public infrastructure such as roads, canals and railroads has come from private sources of capital. And that includes telecommunications in the United States.

The function of private equity also has included the rehabilitation of firms that are not performing financially. Private equity buys a public asset, restructures and then sells the asset, often within about a five-year period.