Inevitably, aside from claims that the “wheels are coming off” the linear video business, there will be renewed criticism that AT&T should instead have spent the capital used to acquire DirecTV, and then (if approved by regulators) Time Warner, to upgrade its consumer access networks.

The critics are wrong; simply wrong, even if it sounds reasonable that AT&T could have launched a massive upgrade of its fixed networks, instead of buying DirecTV or Time Warner (assuming the acquisition is approved).

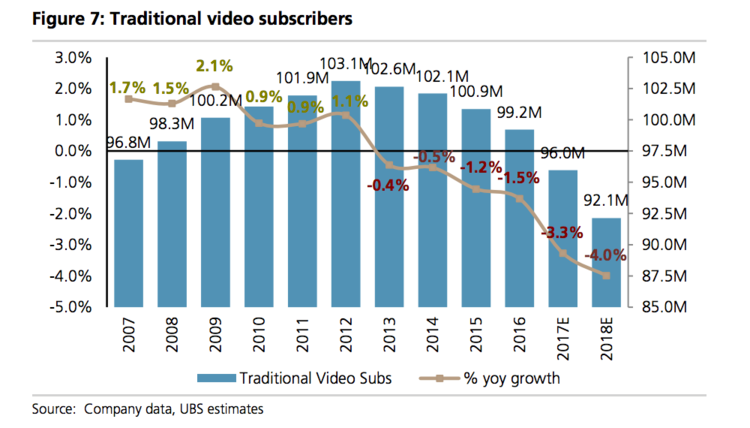

AT&T already has said it had linear video subscriber losses of about 90,000 net accounts in the third quarter. In its second quarter, net losses from U-verse and DirecTV amounted to about 351,000 accounts.

Keep in mind that, as the largest U.S. linear video provider, AT&T will lose the most customers, all other things being equal, when the market shrinks.

Such criticisms about AT&T video strategy might seem reasonable enough upon first glance.

Sure, if AT&T is losing internet access customers to cable operators because it only can offer slower digital subscriber line service, then investing more in internet access speeds will help AT&T stem some of those losses.

What such criticisms miss is that that advice essentially is an admonition to move further in the direction of becoming a “dumb pipe” access provider, and increasingly, a “one-service” provider in the fixed business.

That key implication might not be immediately obvious.

But with voice revenues also dropping, and without a role in linear or streaming subscription businesses, AT&T would increasingly be reliant on access revenues for its revenue.

Here is the fundamental problem: in the competitive era, it has become impossible for a scale provider (cable or telco) to build a sustainable business case on a single anchor service: not video entertainment, not voice, not internet access.

In fact, it no longer is possible to sustain profits without both consumer and business customers, something the cable industry is finding.

So the argument that AT&T “should have” invested in upgraded access networks--instead of moving up the stack with Time Warner and amassing more accounts in linear video with the DirecTV buy--is functionally a call to become a single-service dumb pipe provider.

That will not work, and the problem is simple math. In the fiercely-competitive U.S. fixed services market, any competent scale player is going to build a full network and strand between 40 percent and 60 percent of the assets. In other words, no revenue will be earned on up to 60 percent of the deployed access assets.

No single service (voice, video, internet access) is big enough to support a cabled fixed network. Period.

That is why all scale providers sell at least three consumer services. The strategy is to sell more units to fewer customers. Selling three services per account is one way to compensate for all the stranded assets.

Assume revenue per unit is $33. If one provider had 100-percent adoption, 100 homes produce $3,000 in gross revenue per month. At 50 percent penetration (half of all homes passed are customers), just $1650 in gross revenue is generated.

At 40-percent take rates, gross revenue from 100 passed locations is $1320.

But consider a scenario where--on average--each account buys 2.5 services. Then, at 50-percent take rates, monthly gross revenue is $4125 per month. At 40-percent adoption, monthly revenue is $3300. You get the point: selling more products (units) to a smaller number of customers still can produce more revenue than selling one product to all locations passed.

The point is that it is not clear at all that AT&T could have spent capital to shore up its business model any more directly than by buying DirecTV and its accounts and cash flow.

That the linear model is past its peak is undeniable. But linear assets are the foundation of the streaming business, and still throw off important cash flow that buys time to make a bigger pivot.

One might argue AT&T could have purchased other assets, though it is not clear any other assets would have boosted the bottom and top lines as much as did DirecTV.

What is relatively clear is that spending money to become a dumb pipe internet access provider will not work for AT&T, even if all the DirecTV capital had been invested in gigabit networks. At best, AT&T might have eventually slowed the erosion of its dumb pipe internet access business. It would not have grown its business (revenue, profits, cash flow) enough to justify the diversion of capital.

Would AT&T be better off today, had it not bought DirecTV, and invested that capital in gigabit internet access? It is hard to see how that math would play. Just a bit after two years since the deal, AT&T would not even have finished upgrading most of the older DSL lines, much less have added enough new internet access accounts to justify the investment.

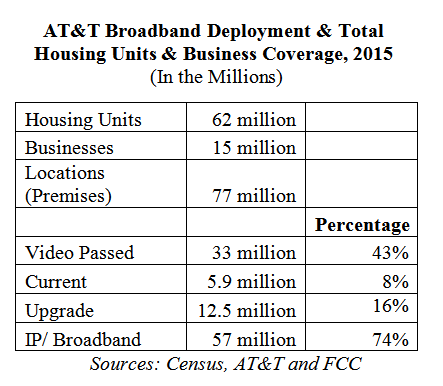

AT&T passes perhaps 62 million housing units. In 2015, it was able to deliver video to perhaps 33 million of those locations. Upgrading just those 33 million locations would take many years. A general rule of thumb is that a complete rebuild of a metro network takes at least three years, assuming capital is available to do so.

Even if AT&T was to attempt a rebuild of those 33 million locations, and assuming it could build three million units every year, it would still take a decade to finish the nationwide upgrade.

In other words, a massive gigabit upgrade, nationwide, would not have generated enough revenue or cash flow to justify the effort, one might well argue.

Assume AT&T has 40 percent share of internet access accounts in its former DSL markets. Assume that by activating that network, it can half the erosion of its internet access accounts. AT&T in recent quarters has lost perhaps 9,000 accounts per quarter. Assuming AT&T saves 10 percent of those accounts, that amounts to only about 900 accounts, nationwide.

That is not enough revenue to justify the effort, whatever the results might be after a decade, when all 33 million locations might be upgraded.

The simple point is that AT&T really did not have a choice to launch a massive broadband upgrade program, instead of buying DirecTV, and instead of buying Time Warner. The financial returns simply would not have been there.