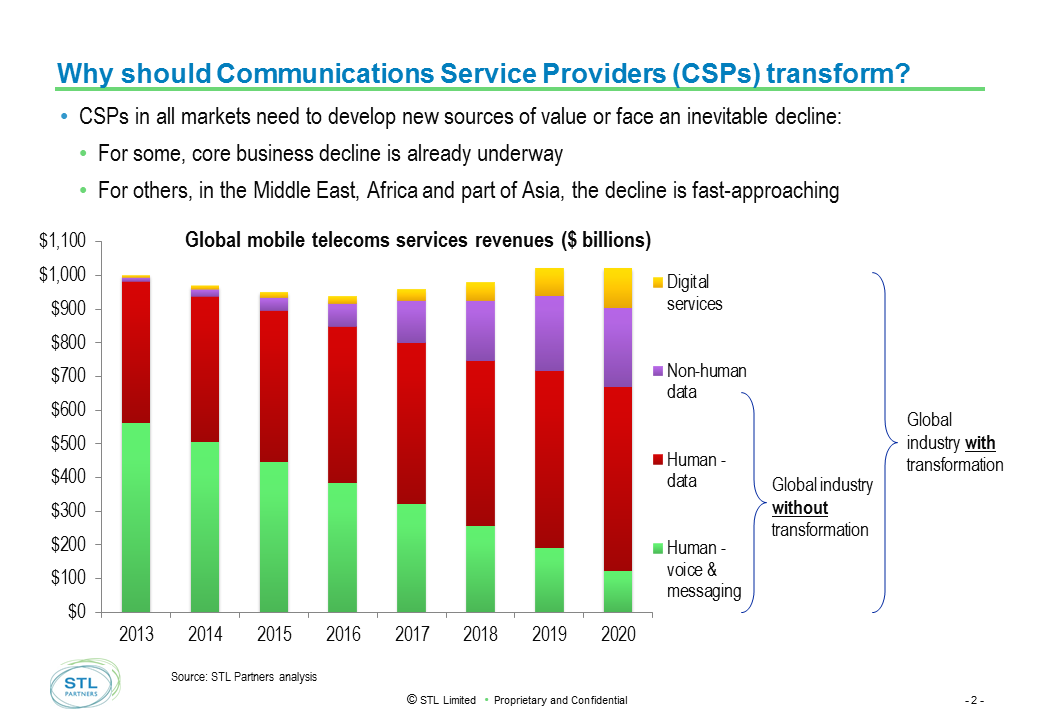

What happens with legacy services is arguably more important, near term, than what happens with new services created by 5G networks. The reasons are obvious: the new services represent smallish revenues while the legacy services represent most of the total revenue.

Small percentage declines in core legacy services have more revenue and profit margin impact than all the new services put together. The image of a hamster running on a wheel might not be appetizing, but that is the situation connectivity providers face.

Or, if you like, a leaky water bucket where new water is poured into the bucket as water continues to leak from holes.

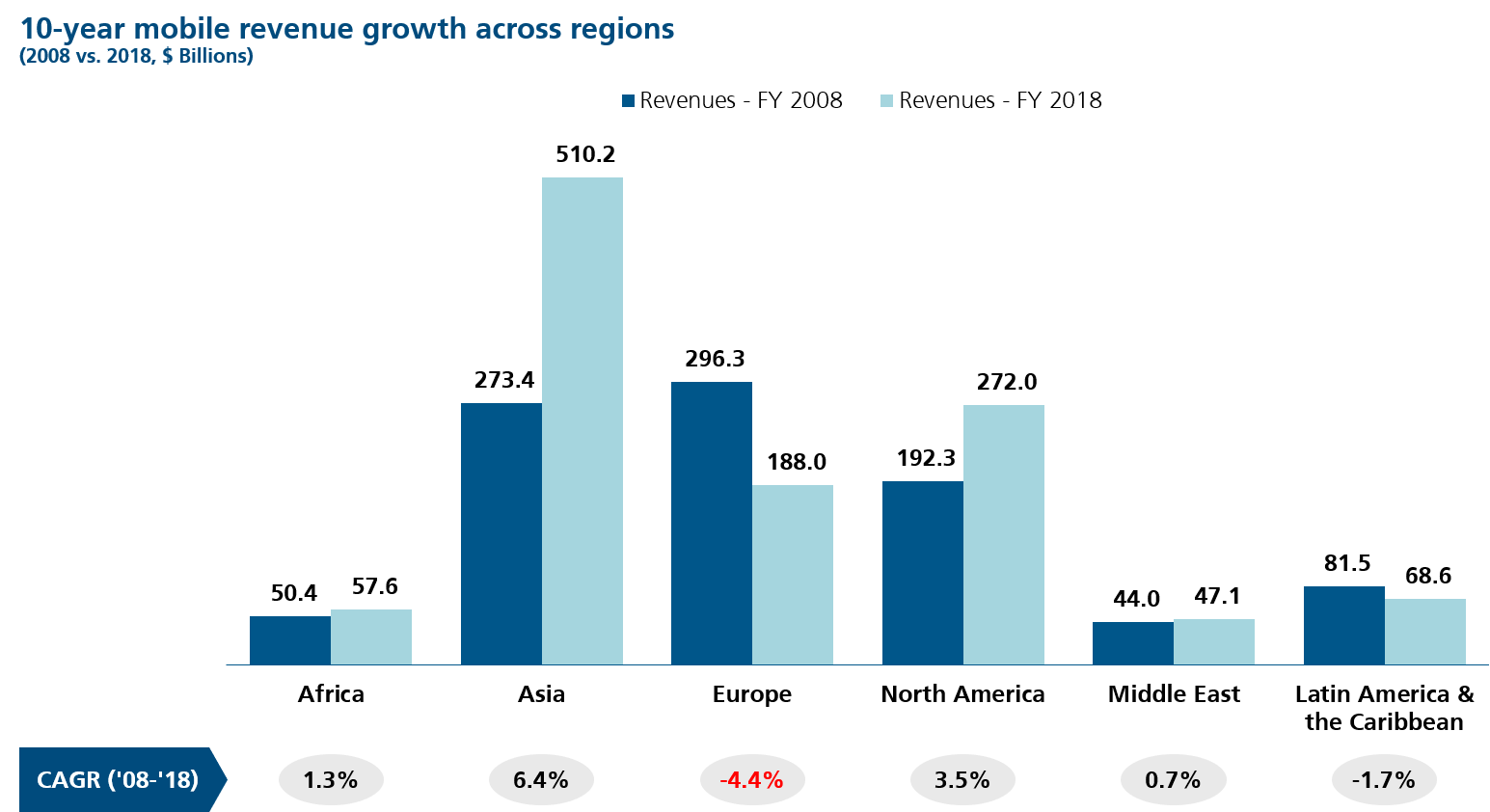

Most connectivity service providers serving well-served and nearly-saturated mass markets would be happy if annual revenue growth chugged along at about a two-percent rate. Service providers in some markets can expect higher growth rates, but the global average will probably be in the two-percent range.

Given some deterioration in legacy lines of business (negative growth rates), growth rates in one or more new areas might have to happen at higher-than-two-percent rates to maintain an overall growth rate of two percent.

And that is the problem for new 5G services in the edge computing, private networks or internet of things areas, for example. The new revenue streams will be small in magnitude, while even a modest decline in a legacy service can--because of the larger size of the existing revenue streams--can pose big problems.

Many service providers, for example, expect big opportunities in business services, which underpins hopes for private networks, edge computing and IoT. But revenue magnitudes matter.

Consumer revenue always drives the bulk of mobile operator service revenues. And revenue growth is the key issue.

But it will be hard for new 5G services for enterprises and business to move the revenue needle.

Edge computing possibly can grow to generate a minimum of $1 billion in annual new revenues for some tier-one service providers. The same might be said for service-provider-delivered and operated private networks, internet of things services or virtual private networks.

But none of those services seem capable of driving the next big wave of revenue growth for connectivity providers, as their total revenue contribution does not seem capable of driving 80 percent of total revenue growth or representing half of the total installed base of revenue.

In other words, it does not appear that edge computing, IoT, private networks or network slicing can rival the revenue magnitude of voice, texting, video subscriptions, home broadband or mobile subscription revenue.

It is not clear whether any of those new revenue streams will be as important as MPLS or SD-WAN, dedicated internet access or Ethernet transport services, for example. All of those can be created by enterprises directly, on a do-it-yourself basis, from the network edge.

In the forecast shown above, for example, services includes system integration and consulting, certain to be a bigger revenue opportunity than new sales of connectivity services.

And though it might seem far fetched, the lead service sold by at least some connectivity providers might not yet have been invented.

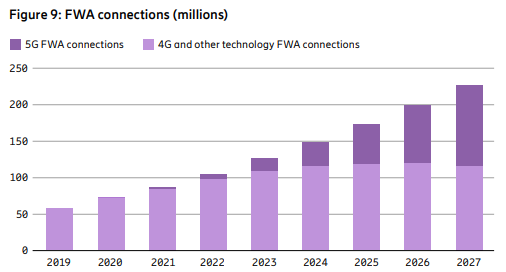

At least so far, 5G fixed wireless is the only new 5G service that is meaningful and material as a revenue source for at least some mobile operators. Even if network slicing, edge computing, private networks and sensor network support generate some incremental revenues, the volume of incremental revenue will not be as large as many hope to gain.

It is conceivable that mobile operators globally will make more money providing home broadband using fixed wireless than they will earn from the flashier, trendy new revenue sources such as private networks, edge computing and internet of things.

Wells Fargo telecom and media analysts Eric Luebchow and Steven Cahall predict fixed wireless access will grow from 7.1 million total subscribers at the end of 2021 to 17.6 million in 2027, growth that largely will come at the expense of cable operators.

source: Polaris Market Research

If 5G fixed wireless accounts and revenue grow as fast as some envision, $14 billion to $24 billion in fixed wireless home broadband revenue would be created in 2025.

The point is that the actual amount of new revenue mobile service providers can earn from new services sold to enterprises is more limited than many suspect.