Some important types of statistics and data are not collected because governments do not force firms or industries to collect it. For example, many governments think it is important to track data on where home broadband exists, where it does not, how fast it operates, who buys and who does not.

Private firms often have important incentives to track and measure their own revenues, sales, profit margins and growth rates. Financial markets and accounting rules often require measurement of this sort.

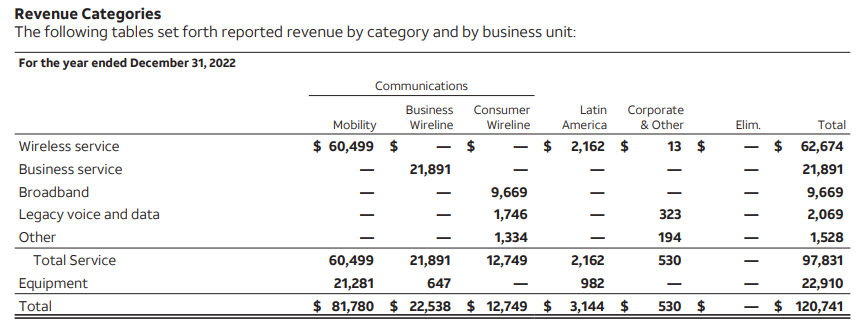

AT&T, for example, reports revenues for mobility, fixed network business revenues and consumer fixed network revenues from internet access, voice and other sources. But those are traditional financial metrics, not operating indices such as penetration or take rates, churn rates and new account gains.

Nobody seemingly believes the same effort should be made to measure the number of home broadband provider locations or dwellings reached by various networks. Better mapping, yes. Metrics on locations passed? No.

And yet “locations passed” is a basic and essential input to accurately determine take rates (percent of potential customers who actually buy). That input matters quite a lot to observers when evaluating the growth prospects of competitors, even if that figure does not matter much for policymakers, who mainly care about the total degree of home broadband take rates, on an aggregate basis.

The U.S. Census Bureau, for example, reported some 140.5 million housing units housing units as part of the 2020 census. The estimate for 2021 units is 142.2 million units. Assume 1.5 million additional units added each year, for a 2022 total of about 143.6 million dwelling units.

Assume vacancy rates of about six percent. That implies about 8.6 million unoccupied units that would not be assumed to be candidates for active home broadband subscriptions. The U.S. Census Bureau, though, estimates there are about 11 million unoccupied units when looking at full-time occupied status. That figure presumably includes vacation homes.

Deducting the unoccupied dwellings gives us a potential home broadband buyer base of about 132.6 million locations.

More difficult is the degree to which access networks operated by any single contestant actually pass those locations, as firms generally do not report such numbers in quarterly financial or annual reports (they do not have to do so).

And that is where estimations must be made. AT&T’s 2022 10-K report cites 14.2 million customer locations connected. Assume AT&T has about 20 percent take rates for its home broadband services where it operates. That implies a housing unit coverage of about 71 million dwellings.

Assume AT&T has a higher take rate of about 39 percent where it operates fixed networks. That implies housing coverage of about 36 million dwellings.

The estimate of 71 million home passings strikes me as too high, but the estimate of 36 million seems too low. In the past I have used the figure of 62 million homes passed for AT&T.

Assume Verizon has about 10 million home broadband accounts, with a take rate of 40 percent (a bit high, probably, if we include copper access). That implies housing coverage of some 25.3 million dwellings.

Leichtman Research Group has estimates of home broadband accounts that vary from company reports. LRG estimates that AT&T has some 15.4 million internet access accounts. The variance might come from business accounts not enumerated.

Verizon’s consumer accounts might be overstated, as LRG estimates Verizon has about 7.5 million home broadband accounts, not 10 million. Using the LRG account figures, we might estimate Verizon home coverage of about 18.8 million homes, on the high side.

source: Leichtman Research Group

Assume Comcast has 31.2 million accounts, with take rates for home broadband of about 52 percent. That implies something on the order of 60 million households.

Assume Charter Communications has a take rate of about 45.5 percent where it operates fixed networks. Assume Charter has approximately 30.8 million home broadband accounts. That implies a homes-passed figure of about 67.7 million homes.

If there are 132.6 million U.S. occupied home locations, then Comcast and Charter can reach about 127.7 million of those locations, or about 96 percent of total, as Comcast and Charter essentially have unduplicated networks, not competing in the same geographies.

That strikes me as unlikely, on the high side. An older rule of thumb is that Comcast and Charter reach about a third of total U.S. locations, each, for a possible reach of up to 66 percent of total U.S. home locations.

Using different methodologies, I have in the past estimated that Comcast has (can actually sell service to ) about 57 million homes passed, while the Charter Communications network passes about 50 million homes, the number of potential customer locations it can sell to.

Verizon homes passed might number 18.6 to 20 million. To be generous, use the 20 million figure.

AT&T’s fixed network represents perhaps 62 million U.S. homes passed. CenturyLink never reports its homes passed figures, but likely has 20-million or so consumer locations it can market services to.

Ignoring the variance in potential customer locations passed, AT&T would seem to have the greatest opportunity in the home broadband space, if it can build optical access connections faster, as has the biggest home footprint and low home broadband market share.

On the other hand, AT&T revenue is driven by mobility, not the consumer fixed network. So then the question has to be posed as "how much to invest in the consumer fixed network?" compared to other oportunities. A rational person might argue that answer is "not so much."

Capital availability--and financial returns--are always the issue. Even if it dramatically escalated fiber-to-home capital investment, it is not clear AT&T would gain as much new revenue, compared to investing in mobility or business services, for example.

The point of the wider exercise is that we are forced to guess about how many homes each of the major fixed network contestants actually can reach. That, in turn, affects our ability to estimate adoption rates and potential growth opportunities.

The key point is that the estimates are imprecise. Pinning down the “homes passed” figure, essential as the denominator in any calculation of take rates, requires estimations with variable degrees of uncertainty, especially for the larger networks.