Whenever the next U.S. recession happens, we will see whether the many changes in the telecom, cable TV and video streaming markets will change the historic view of how telecom and video entertainment stocks behave during downturns.

Traditionally, both telecom and cable TV equities have been viewed as resistant to customer defections in recessions as both are “essential” or “important” recurring services.

But the markets and consumer tastes have been evolving: reliance on mobile phone services and abandonment of fixed network services; substitution or addition of video streaming services and reduced linear video subscription buying; increased importance of internet access and a decrease in importance of voice and linear video services.

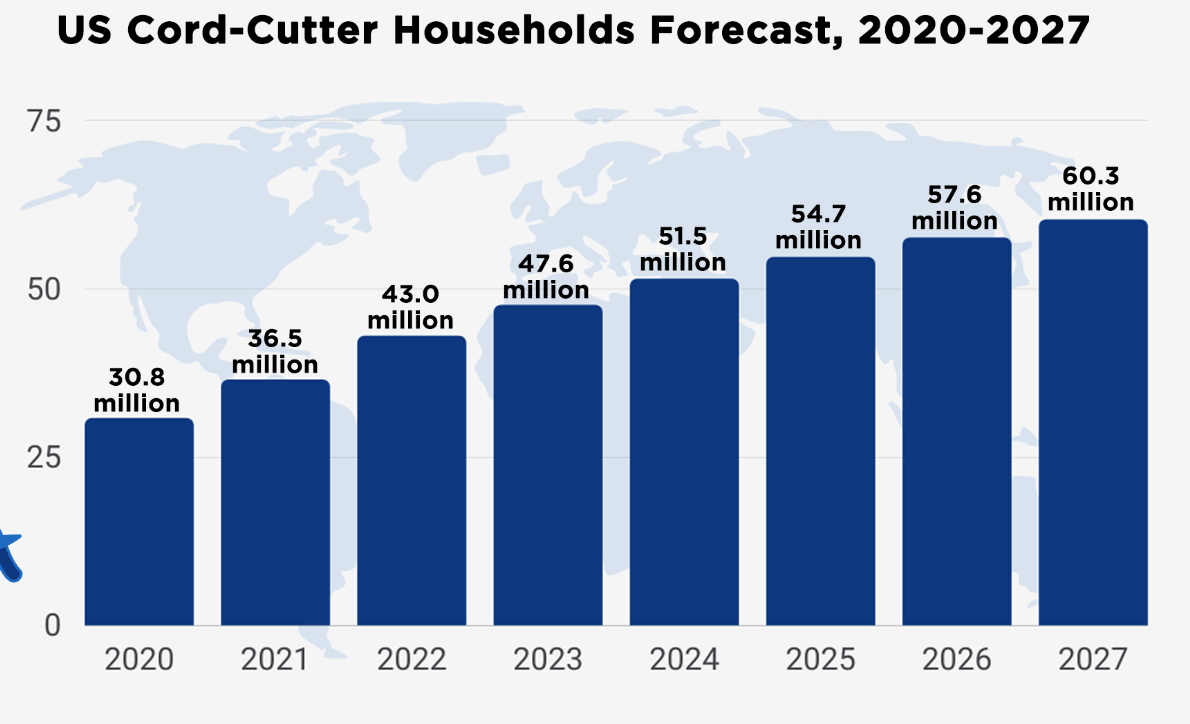

source: Broadband Search, Seeking Alpha

All of which raises new questions, including the issue of whether streaming services will prove more resistant to customer churn during recessions, compared to linear video.

Study Title/Author | Findings |

"Do Consumers Cut the Cord in a Recession?" by John Beggs and Patrick/2010 | Found a slight decrease in cable TV subscriptions, but not a significant decline. |

"Telecom Stocks and Economic Downturns" by JPMorgan Chase (Investment Report) /2020 | Indicated telecom stocks generally outperform the broader market during downturns. |

"The Recession Resilience of Defensive Sectors" by Fidelity Investments (Market Commentary) /2023 | Listed telecom as a sector with potential resilience, but noted the importance of specific company financials. |

The Recession and Telecom, Deloitte (2009) | Revenue for telecom service providers remained relatively stable during the 2008 recession, but capital expenditures declined. |

The U.S. Telecommunications Industry During Economic Downturns, The Brattle Group (2010) | While telecom revenue growth may slow during recessions, it generally holds up better than the broader economy. |

Cord Cutting: What Do Past Recessions Tell Us? MoffettNathanson (2020)

| Previous recessions saw limited cord-cutting, suggesting cable TV might retain some stability during downturns. However, the study acknowledges the changing media landscape. |

Fama & French (1989) | Defensive sectors like telecom and utilities tend to outperform cyclical sectors. |

Ang & Timmermann (1993) | Telecom and utilities exhibit lower volatility and higher risk-adjusted returns during recessions. |

Blitz & Reichlin (2001) | Telecom and utility stocks are less affected by credit downgrades compared to cyclical sectors. |

A recession might accelerate the secular trend of fixed network voice service abandonment, as consumers prefer mobile phone service. Likewise, a recession might also accelerate linear video abandonment rates, considering the relative expense, compared to streaming alternatives.

To be sure, live sports will be a key issue for a portion of the buying public. Though most observers see a continuing shift of live sports to streaming services, that trend is not as developed, yet. So sports fans might still conclude they have no choice but to keep their linear video subscriptions.

And that should continue to prop up demand during recessionary periods.

On the other hand, perhaps a majority of consumers who are not sports fans can buy multiple streaming subscriptions at lower (or near equivalent) prices than they can buy a linear subscription, suggesting the possibility that streaming services could prove more attractive during a recession.

Also, streaming arguably still is a growth business, while linear video is in decline. Any recession might accelerate such trends.

source: Ryan Ang, Seeking Alpha

The most recent recession, caused by the imposition of Covid shutdowns on the economy, might not provide much insight. With the “in person” economy largely shut down in many countries, demand for work from home or learn from home internet access was quite high.

Take rates and usage of mobility services arguably rose for the same reason. And the value of streaming and even linear TV services arguably was boosted by the lack of other entertainment options.

So the most-recent major downturns for which we arguably have data would be the 2008 global financial crisis and the 2000 to 2001 dotcom crash, when video streaming was not a mainstream business at scale.