The number of U.S. telco video subscribers will rise from 8.8 million in 2011 to 18.6 million in 2017, according to Parks Associates now forecasts. That gain by telcos will come from share presently held by cable TV customers and satellite providers.

Satellite's share of the subscription video market will drop to 30 percent by 2017, while cable's share will fall to 52 percent, while telco IPTV share will rise to 18 percent.

Cable video subscribers will decline from 60.7 million in 2011 to 56.1 million in 2017.

Those figures show the difference between incumbent and attacking providers in a mature market. Under those conditions, “harvesting” is a typical business strategy for leading contestants in declining markets.

When executives believer there is no real opportunity to reverse a product slide into the declining side of its product life cycle, it makes sense to harvest cash, but not to invest too much to “save” the business, or turn it around, as the judgment simply is that the business is mature and inevitably will decline.

It does make sense to invest only enough to slow the rate of decline, of course. Attackers, on the other hand, can do nicely for a while simply by taking market share.

Video is largely becoming a harvesting exercise for cable operators, just as long distance calling and legacy voice are examples of “harvesting” by telcos.

As the attacker in voice and business services, cable operators still can grow revenue in the near term, as telcos can grow revenue in video. Over the longer term, though, even attackers can only achieve so much, in a maturing market.

For cable, consumer voice revenues have ceased to be much of a growth business, which explains the shift to business customers. Telcos and satellite video providers still have room to continue taking video share, though. Sooner or later, that might run into resistance, especially if over the top video, featuring the same content now part of video subscriptions, takes off.

A new ABI Research study suggests that nearly 20 percent of online video consumers consider online video as a replacement for entertainment video subscriptions. That obviously represents “significant risk” to the traditional video entertainment business.

ABI Research suggests the magnitude of potential revenue loss could range as high as $16.8 billion in the U.S. market, for example. Telcos won’t face those issues, as they are predicted by virtually every study to continue taking market share, as cable TV operators and satellite providers continue to lose market share over time.

But at least one analysis has satellite providers overtaking cable TV providers in revenue in 2017.

So the near term trends might not be “linear,” as some forecasters still project cable TV operator and satellite provider video revenues growing for a period, Digital TV Research forecasts.

But a change that shaves as much as $17 billion from U.S. providers would seem to be a longer-term danger, as ABI Research also suggests U.S. video entertainment penetration is dropping at a rate of about 0.5 percent per year through 2017.

That arguably is an optimistic scenario for cable TV providers. Ignoring changes of market share between the contestants, a loss of perhaps half a percent a year of subscribers won’t make a large dent in a revenue stream that collectively represents more than $90 billion in annual revenue.

If the number of subscribers were directly related to the amount of revenue, then a half percent a year decline would represent perhaps $450 million in lost revenue each year. At such rates, it would take decades before service providers lost $17 billion.

Whatever share shift one expects, the game now for video service providers is to “take or protect” market share.

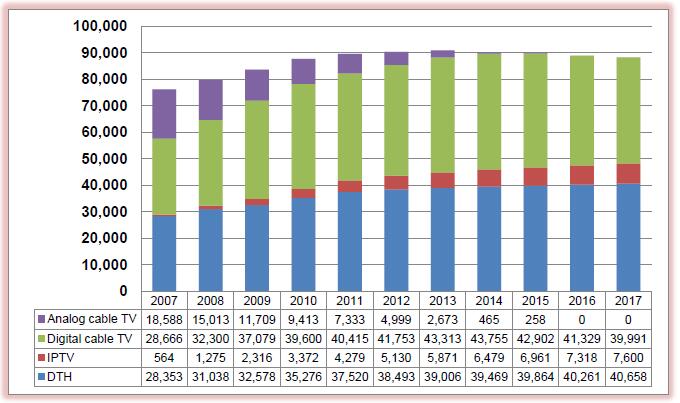

North America pay TV revenues ($ mil.)

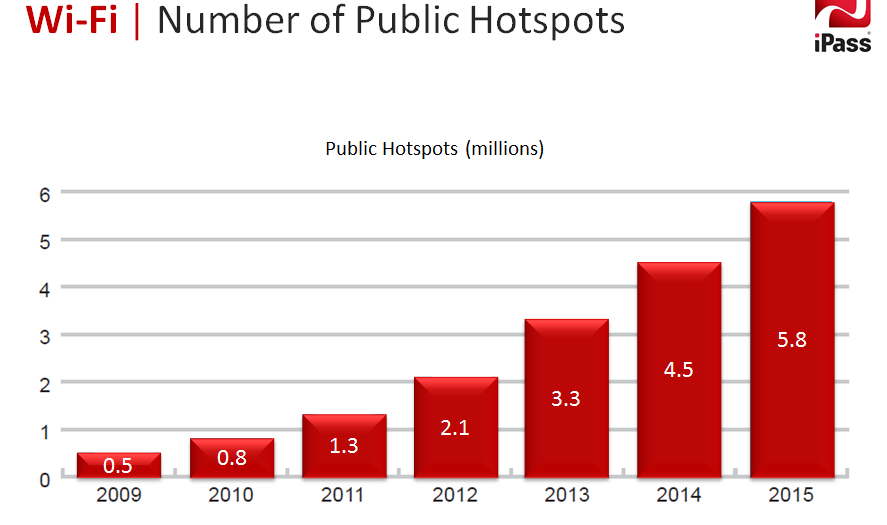

According to some estimates, 90 percent of the tablets sold in the United States use Wi-Fi connections rather than cellular.

According to some estimates, 90 percent of the tablets sold in the United States use Wi-Fi connections rather than cellular.