Similarly, some observers decried, or sometimes continue to decry, lagging U.S. Internet access speeds, prices or both. Ignore for the moment conflicting evidence about whether that remains the case, or to what extent there are differences.

Still, European observers now worry that “Europe is falling behind” in next generation fixed broadband or mobile Long Term Evolution.

European service providers lead the deployment of a succession of technologies, from GSM to early deployments of LTE in the nordic countries, for example. And then there was the leadership of firms such as Nokia. Nokia’s fall is part of the present worry.

With the advent of the smart phone era, innovation and perceptions have changed. the success of Apple and Android's devices, operating systems and apps moved the center of innovation to the United States, while Asian companies are more relevant than ever, according to Analysys Mason.

As once too much attention was paid to European leadership and U.S. “gaps,” now too much is made of U.S. leadership and European lagging.

It might be reasonable to say that since U.S. firms tend to lead with software, a shift to a software-driven mobile Internet would potentially shift fortunes. One might also argue regulatory regimes in North American and Europe have had direct impact on both the level of competition and investment.

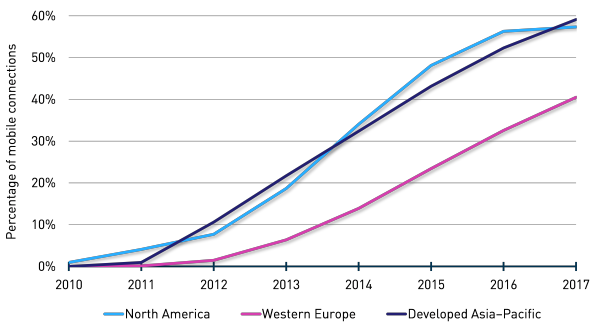

LTE connections as a percentage of mobile connections, selected regions, 2010–2017 [Analysys Mason, 2013]

One might also note that European operators adopted faster versions of 3G networks at level that matched customer demand for speed, resulting in less need to upgrade to 4G.

The point is that investment, consumer demand, software and hardware supply will shift, from time to time. Over time, adoption, supply and impact tends to equalize, from one developed region to the next.

Also, at some point, the issue is what value a given nation or region can wring out of its investments, not the mere fact that investment in faster networks has been made. That always will be tough to measure.

Though the hand wringing about Europe “falling behind” is real, it has to be kept in perspective. Many would have noted U.S. “lags” in broadband and mobile adoption as well. Sustainable “advantage” seems to be as elusive in communications technology as it is in the life of firms.