Dish Network, in what many consider a breakthrough deal, has gotten rights to eventually stream Disney content. DirecTV might be close to gaining similar streaming rights as well.

Those deals will not immediately lead to stand-alone, over the top streaming services that can be bought without also buying a linear video subscription service, for several reasons. For starters, even Disney will not allow such a service to be launched unless the provider also can offer other top-rated networks.

In other words, Disney does not want to be made available as a “Disney-only” service, but only as part of an attractive, broad service that includes much of the standard fare consumers expect to buy as part of a standard expanded basic service from any cable, satellite or telco video services supplier.

On the other hand, one might argue that with the one deal, Dish Network--and DirecTV--are about a quarter of the way to assembling an attractive programming lineup that delivers much of the value consumers expect from an “expanded basic” subscription (the tier of service most consumers buy, including bundles of ad-supported channels).

That’s important, if not the sign such a service will be made available soon.

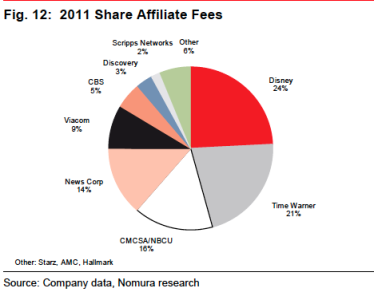

By itself, Disney might represent about 24 percent of all programming costs for a typical linear video entertainment distributor. Time Warner represents perhaps 21 percent of the program rights cost, NBC about 16 percent, Fox about 14 percent. Getting the three other top networks, in terms of programming cost, would allow Dish Network to provide roughly 75 percent of the value of a subscription, one might roughly argue.

In fact, those four networks account for 75 percent of programming rights fees, and if you assume costs are roughly in line with perceived value, then Dish Network has to reach deals with three more firms to deliver about 75 percent of the value of a traditional video subscription.

Disney distributes the ESPN and ABC family of channels. Time Warner owns TNT, TBS and CNN. Comcast, owns Bravo, USA Network and NBC. News Corp. owns Fox News and Fox broadcast channels.