Has the U.S. mobile marketing war finally begun to show in Verizon and AT&T financial performance? Not so much, at least not yet.

Operating results seem to be showing some pressure, but it is hard to distinguish background market maturation trends from the specific impact of T-Mobile US attacks.

AT&T first-quarter 2014 consolidated revenues of $32.5 billion represented growth of 3.6 percent.

Verizon total operating revenues in first-quarter 2014 were $30.8 billion, a 4.8 percent increase compared with first-quarter 2013 and the company’s highest quarterly growth rate in the past five quarters.

The mobile segments of AT&T and Verizon face market maturity, of course, so slowing growth rates would not be unexpected. The issue is whether higher levels of competition are affecting mobile segment gross revenue, profit margins or subscriber gains.

Total Verizon mobile segment revenues were $20.9 billion in first-quarter 2014, up 6.9 percent year over year. AT&T reported seven percent mobile segment revenue growth.

Clearly, at the top line, it is hard to see any clear negative impact from higher levels of competition.

But there is a significant nuance in terms of mobile segment revenue sources. Verizon mobile service revenues in the quarter totaled $18 billion, up 7.5 percent year over year.

Retail service revenues grew 6.7 percent year over year, to $17.2 billion. That means device revenue was less than $3 billion of quarterly mobile segment revenue.

At AT&T, mobile service revenue grew service revenues grew about 2.2 percent, compared to four percent, in the same quarter a year ago.

In other words, Verizon is growing mobile service revenue about 4.5 percentage points more than AT&T is growing its own service revenue.

Verizon retail postpaid average revenue per account increased 6.3 percent over first-quarter 2013, to $159.67 per month.

On the other hand, mounting price competition seems to be hitting Verizon mobile profit margins.

In first-quarter 2014, Verizon mobile operating income margin was 35 percent and segment EBITDA margin on service revenues was 52.1 percent, compared with 32.9 percent and 50.4 percent, respectively, in first-quarter 2013.

In other words, Verizon profit margins dropped, year over year.

AT&T added many more net mobile subscribers than did Verizon in the first quarter, though. AT&T net additions increased by 1,062,000 in the quarter, led by 625,000 postpaid net adds and 693,000 connected device net adds, the strongest postpaid

growth in five years.

Verizon Wireless added 549,000 retail net connections, including 539,000 retail postpaid net connections, in the first quarter.

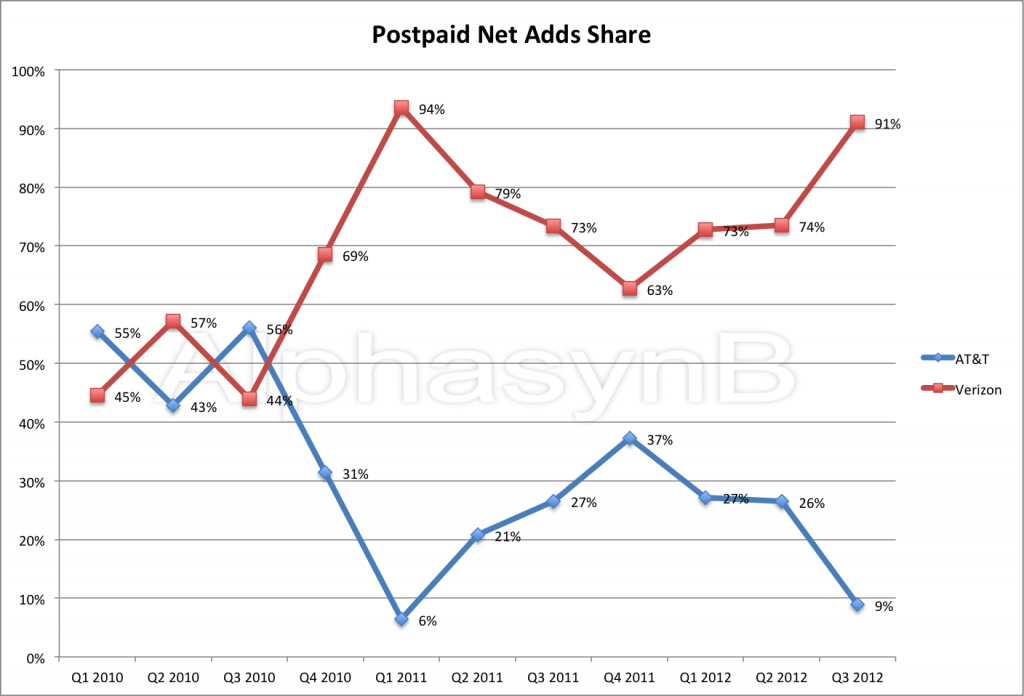

Those figures are significant because Verizon started to pull away from AT&T in the key net postpaid additions category about the fourth quarter of 2010.

And it appears that virtually all of Verizon’s first quarter net subscriber gains came from tablets, not phones.

Verizon added a net 539,000 retail postpaid connections, down from 720,000 net additions a year ago.

But Verizon signed up 634,000 net new tablet connections. In other words, Verizon lost net phone customers, though growing on the strength of tablet connections.

AT&T clearly is benefitting from tablet net additions as well.

Even after T-Mobile US reports its own quarterly earnings, we might not have a clear picture of what the marketing war is doing, both financially and operationally, in part because tablets now are fueling so much of the net subscriber growth at AT&T and T-Mobile US, in particular.

Even after T-Mobile US reports its own quarterly earnings, we might not have a clear picture of what the marketing war is doing, both financially and operationally, in part because tablets now are fueling so much of the net subscriber growth at AT&T and T-Mobile US, in particular.

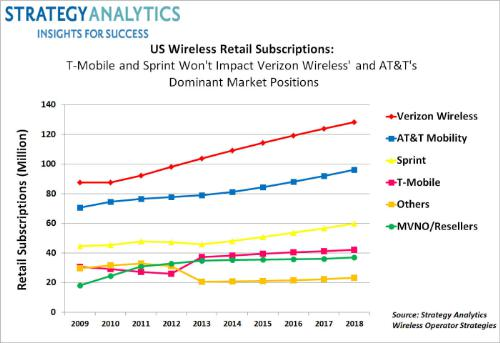

But the long term picture might not be so different from a scenario where T-Mobile US had not kicked off a marketing battle, Strategy Analytics has argued.

In fact, Strategy Analytics think the U.S. mobile market will remain stable through 2018, with little change in market share.

Among the top four carriers, Verizon Wireless stays on top and T-Mobile on the bottom, while only Sprint gains more than a percentage point in share, Strategy Analytics forecasts.