Uber is finding out that in regulated markets, even when new technology and business models are pioneered, regulators use a simple test, not much more complicated than captured by the phrase “If it looks like a duck, swims like a duck, and quacks like a duck, it’s a duck.”

|

| source: TeleGeography |

Aereo found itself facing the same problem when courts ruled that Aereo essentially is a cable TV business, and must pay licensing fees to redistribute off-air TV signals.

VoIP providers found that to be true after they started to take significant market share from legacy providers.

In other words, even new technology and clever business models will long survive regulatory scrutiny and compliance when the new approaches are applied in competition with legacy businesses.

So now Uber is slowly conceding to demands that its drivers and services be subject to the same rules as apply to licensed taxicab firms, Aereo has been ruled illegal and connected VoIP services pay the same taxes and fees as do legacy voice services.

Sometimes the Internet has other impact on legacy businesses, especially when applied to non-regulated industries.

Publishing and music already have seen a profound change in industry revenue potential, as well as changes in the way content is created, presented and distributed to consumers and customers.

In other cases, the Internet can transform an industry by making the market smaller.

In other words, it has now become a fact of business life that the Internet not only brings efficiencies to any market it touches, but actually can destroy legacy markets.

And that might be the fate of the wide area network capacity business. In 2003, the global private line business generated about $36 billion in annual revenue. By about 2016, private line revenue might hit $42 billion.

But there is an unmistakable trend: legacy voice and capacity revenues are declining, at least in in developed markets.

Between 1997 and 2007, for example, long distance, which represented nearly half of all U.S. telecommunications revenue, was displaced by mobile voice services.

The point is that such revenue declines put unrelenting pressure on the capacity business, as wholesale services are sold to customers who must not only attack their own operating and capital costs, but also can build and operate their own facilities in an effort to do so, creating the opportunity for converting transit payments into network infrastructure investments, instead.

That has the effect of putting pressure on transit revenue opportunities and capacity sales, as service providers build their own captive networks.

For example, consider that the IP transit market generated $2.1 billion in revenues in 2013. Sales of circuits connecting customers to Internet hubs contributed an additional $2.5 billion, for a total of $4.6 billion in revenues, according to TeleGeography.

But consider that other new segments, such as content delivery networks , already by 2013 had grown to be a business generating perhaps $2.5 billion in global revenues, headed for perhaps $4.5 billion by 2017.

By way of comparison, U.S. local access revenues generated from business segment Ethernet access services passed $4 billion worth of revenue in 2011, and is projected to reach $11 billion by 2016.

And though global wholesale revenues might total $142 billion in 2019, that is driven largely by mobile service wholesale, not wide area network transport.

The point is that, all revenue sources considered, the long-haul capacity markets continually face the reality of customers building their own long-haul networks, trading operating expense for capital investment.

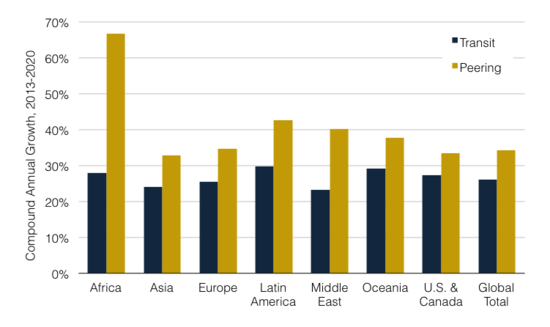

TeleGeography analysts say that the fate of the IP transit business rests on the growth of peering relationships that obviate the need for IP transit purchases.

“As Internet service providers worldwide have gradually migrated from purchasing transit to establishing mostly free peering arrangements, the share of global Internet traffic connected via transit agreements declined from 47 percent in 2010 to 41 percent in 2014,” TeleGrography says.

|

| source: TeleGeography |

In other words, undersea and long haul capacity, which once was a significant revenue stream, is gradually becoming a matter of private networks interconnecting without charge.

As long as this relative decline of transit continues, TeleGeography forecasts that IP transit-related revenues will fall from $4.6 billion in 2013 to $4.1 billion in 2020. If the ratios of traffic routed via transit and peering were to stabilize at current levels, IP transit revenues would increase to $5.5 billion by 2020.

So far, you might argue the effects have been somewhat subtle. While African Internet traffic is forecast to grow 36 percent annually over the next seven years, transit volumes will increase by only 28 percent compounded annually, while peering volumes will grow 67 percent—driving down the share of traffic routed via transit from 90 percent in 2014 to 61 percent in 2020, TeleGeography says.

Ignore for the moment the tendency of capacity services to decline in price every year. At least for the moment, peering economics seem to be strong enough to make investment in one’s own infrastructure a reasonable alternative to transit services.

Might that change in the future? TeleGeography says that could happen, if transit prices were to fall low enough.