Mobile penetration in Myanmar has roughly doubled in about a year, after the awarding of new mobile licenses, according to government sources.

Noting that in Thailand and Vietnam mobile adoption rates grew from 10 perent to 50 perent in about three to four years, Myanmar possibly can get there in a year, a government official says.

According to International Telecommunications Union data, mobile penetration in mobile penetration in Africa hit an inflection point at five percent. Roughly five years later, adoption reached about 35 percent.

That is a relatively normal adoption curve. According to Market Intelligence Center, developing nation mobile penetration rates grew from about 10 percent to 45 percent in about five years.

Thursday, July 17, 2014

Will Myanmar Mobile Penetration Grow from 10% to 50% in 4 Years?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, July 16, 2014

Content Business Now is "in Play"

When does a rejected acquisition bid nevertheless have consequences? When a big rejected bid means a target company is “in play.” So it is with the rejected $80 billion bid by 21st Century Fox to buy Time Warner.

Despite the rejection, other potential bidders now will have to evaluate whether their own bids to acquire Time Warner might now be on the agenda.

But one might also argue that lots of companies could likewise be candidates for acquisition, using the same deal logic that drove the 21st Century Fox bid for Time Warner.

If Time Warner is seen to be worth $80 billion, what other assets could be acquired for less?

Disney is big enough it is unlikely to be an acquisition candidate. But it could be a buyer.

Other content firms are more likely targets than buyers. Viacom’s market capitalization is around $36 billion, while CBS has a market cap of about $34 billion.

And though the list of potential bidders would include other big media concerns, it sometimes happens that friendly overtures, if rebuffed, develop into hostile takeovers. So 21st Century Fox might craft another offer.

Time Warner might not be the only major content firm that gets acquired.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

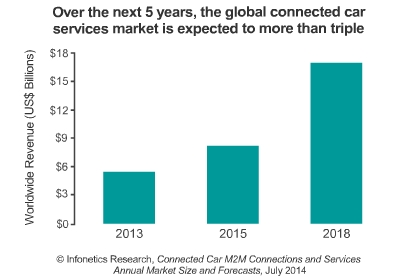

LTE the Big Winner for Connected Car?

Not every machine-to-machine or "Internet of Things" requires lots of bandwidth, or continual connection. But the connected car market likely includes a wide enough range of app requirements that Long Term Evolution, the highest-capacity mobile network, will lead growth.

Not every machine-to-machine or "Internet of Things" requires lots of bandwidth, or continual connection. But the connected car market likely includes a wide enough range of app requirements that Long Term Evolution, the highest-capacity mobile network, will lead growth.

“LTE will be the fastest-growing cellular technology in cars, expanding 135 percent annually between 2014 and 2018,” says Godfrey Chua, directing analyst for M2M and The Internet of Things at Infonetics Research. “A major boon will come from AT&T’s agreement with GM to deploy LTE for the OnStar service.”

Some service providers are seeing as much as 90 percent of their machine-to-machine (M2M) revenue generated from the connected car segment, Chua notes, and much of that opportuntity is, at present, centered in the United States.

North America accounted for 37 percent of global connected car service revenue in 2013.

Infonetics also expects revenue derived by service providers for the connectivity and other basic value-added services they provide to the automotive, transport, and logistics segment to more than triple from 2013 to 2018, to $16.9 billion worldwide.

The connected car services market additionally is growing at a compound annual growth rate of 25 percent, nearly 21 times the growth rate expected for traditional mobile voice and data services between 2013 and 2018.

Whatever one believes about the size of the connected car market, and how big revenue opportunities might be for app providers, automakers and connectivity providers, it is clear that not every “Internet of Things” application and market segment has the same requirements for bandwidth.

Energy meters, for example, generally do not require persistent connections, and feature small uploads quite reasonably handled by 2G networks.

Video surveillance apps, on the other hand, generally require higher bandwidth.

Bandwidth required to support connected car apps will vary. Some diagnostic apps might well only require episodic, bursty, low-bandwidth connectivity. In-vehicle content apps, on the other hand, might well be required to support video, which means Long Term Evolution 4G is almost mandatory.

Real-time navigation apps might do fine with 3G access. Over time, of course, 2G networks will be phased out of service, so all apps ultimately will be available only on 3G or 4G networks.

For the moment, though, the differential app requirements mean “just about any communications service provider, whether they have 2G, 3G, 4G, LTE or a combination of technologies, can find a niche in the connected car space,” says Godfrey Chua,

Of course, since lower-bandwidth apps easily are handled by higher-bandwidth networks, LTE is likely to be a big winner.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thailand 4G Auction Postponement Could Affect Mobile Market Share

Communications spectrum, politics, money, market share and firm fortunes almost always are intimately connected. In Thailand, for example, a delay in holding of fourth generation network spectrum auctions might help the smallest service provider, and harm the biggest provider.

AIS, the largest service provider in terms of subscribers, does not have any present rights to any 4G spectrum. So spectrum scarcity could slow growth, as AIS could find it does not have enough capacity to provide reasonable levels of service to its customers, a problem other mobile service providers have, from time to time, also encountered.

Advanced Info Service, for example, is the biggest mobile company, in terms of subscribers, but has the least amount of spectrum. True, the smallest of the three national carriers, recently got an investment from China Mobile, and the spectrum auction delay could slow AIS growth.

Planned fourth generation mobile network spectrum auctions originally planned for August 2014 have been postponed.

The planned auctions for 25 MHz in the 1.8 GHz spectrum band was due to be held in August 2014, with another 17.5 MHz in the 900 MHz band also expected to be awarded sometime later in 2014.

Some have suggested the auction delay could help one contestant, True, and limit gains by AIS, an expected bidder. So China Mobile gain,s while Telenor might lose, given the potential impact on their Thailand partners.

AIS, the largest service provider in terms of subscribers, does not have any present rights to any 4G spectrum. So spectrum scarcity could slow growth, as AIS could find it does not have enough capacity to provide reasonable levels of service to its customers, a problem other mobile service providers have, from time to time, also encountered.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, July 15, 2014

45% of Mobile Service Providers Offer At Least One Zero-Rated App

Some 45 percent of mobile service providers operators offer at least one zero-rated app, and 65 percent of those zero-rate Facebook, according to a study by Allot Communications.

Some will see the partnerships between mobile Internet service providers and application providers as the key element. Others might focus on the notion of “zero rating” use of a few applications viewed as having high end user value.

That, in turn, is important because it illustrates the downside of “treating all apps equally.” Sometimes, especially in developing nations, app discrimination--providing one app at no charge--provides clear value for people.

Application “non-discrimination” and “no blocking” tends to be the language used by network neutrality supporters. Most people likely have no issue whatsoever with the notion that lawful apps cannot be blocked, in the U.S. market.

As useful as “no blocking” is as a political slogan or principle, new legislation to prevent such blocking arguably is unnecessary, as the Federal Communications Commission already enforces such principles.

The original concern was use of quality of service mechanisms, especially packet prioritization, as opposed to the present “best effort only” level of service available to U.S. consumer Internet access customers.

The concern was that Internet service providers would create new tiers of service that offered better end user experience at times of network congestion, but that such services would lead to additional costs for application providers who wanted such access, as they now pay firms such as Akamai for content delivery services that provide similar benefits over the network backbones.

Recently, the rubric of network neutrality has been extended into other areas--including network interconnection--that similarly have “cost of doing business” implications for app providers.

Of course, extending an analogy too far can backfire. The concept of “treating all apps equally” is attractive, and sounds eminently fair.

But mobile service providers in many developing markets find that treating apps quite unequally provides value for end users and creates demand for mobile Internet access.

In fact, about 85 percent of mobile service providers promote certain over the top apps--and not all apps--according to Allot Communications.

Quite often, mobile service providers also zero-rate Facebook, Twitter or WhatsApp, as a way of illustrating the value of mobile Internet access.

Social apps, in other words, have proven to be attractive “gateway” apps for consumers. Actual policies differ. Some service providers offer free Facebook access only for newsfeed text and

text postings.

Others offer free Facebook messenger use, while others zero rate all Facebook traffic, with no need for a mobile data plan.

In 2012, 27 percent of operators sampled offered application-centric plans to their customers.

In 2014 these partnerships are up to 55 globally, according to Allot. And some 40 percent of application-centric charging plans focus on zero rating. The rest are premium services that do carry a retail price tag.

Application-centric plans often provide TV streaming, on-demand video streaming, music streaming and music storage. But GPS location services, parental control and tracking features often are offered for an additional fee.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"Customer Surly" and "Customer Friendly" Service: 2 Anecdotes

It's only one anecdote, but one does wonder whether incentives for "saving" an account could have something to do with what many could say is an overly-aggressive effort by one Comcast CSR to save an account, when the customer wanted to halt service.

Few might consider the call a pleasant experience.

I had the diametrical opposite experience recently when changing service levels for my mom's Verizon FioS video account. I needed to downgrade one premium video service and also end purchase of a backup and security service for the Internet access account.

The former downgrade was because she doesn't watch so much TV, and certainly was not watching the premium service. The latter downgrade was because, after moving mom to a Chromebook, the online backup and security package simply was unnecessary.

I got everything done, right away, on the Verizon website, with no need to make a call, talk to a customer service representative and endure the "save the revenue" script I suspect I'd otherwise have encountered.

To be sure, Verizon's customer-friendly approach to online downgrades meant Verizon did not have one more shot at avoiding the two downgrades.

On the other hand, I appreciated the chance to quickly and easily accomplish a service level change without grief.

Perhaps one should not conclude too much from just a couple of customer interactions with a major service provider.

But it also is hard not to wonder whether a different approach is at work in these two instances.

I probably am not the only potential customer, or existing customer, who has encountered what appears to be a deliberate effort by a service provider to make dropping or downgrading more difficult.

Few might consider the call a pleasant experience.

I had the diametrical opposite experience recently when changing service levels for my mom's Verizon FioS video account. I needed to downgrade one premium video service and also end purchase of a backup and security service for the Internet access account.

The former downgrade was because she doesn't watch so much TV, and certainly was not watching the premium service. The latter downgrade was because, after moving mom to a Chromebook, the online backup and security package simply was unnecessary.

I got everything done, right away, on the Verizon website, with no need to make a call, talk to a customer service representative and endure the "save the revenue" script I suspect I'd otherwise have encountered.

To be sure, Verizon's customer-friendly approach to online downgrades meant Verizon did not have one more shot at avoiding the two downgrades.

On the other hand, I appreciated the chance to quickly and easily accomplish a service level change without grief.

Perhaps one should not conclude too much from just a couple of customer interactions with a major service provider.

But it also is hard not to wonder whether a different approach is at work in these two instances.

I probably am not the only potential customer, or existing customer, who has encountered what appears to be a deliberate effort by a service provider to make dropping or downgrading more difficult.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Can 5G Erase Difference Between Mobile and Fixed?

Though it is early to specify what characteristics future fifth generation (5G) mobile networks will feature, at least some think 5G will be the first next-generation mobile network with a specific applications focus and the first mobile platform that erases performance differences with the fixed networks.

Those are among some of the conclusions one might draw from the 5G “Public Private Partnership,” a new European 5G initiative.

Ironically, given the amount of present argument advanced about the need for maintaining “best effort only” access (no packet prioritization), the 5G PPP document also notes the “future challenge will be to guarantee and continuously improve customer experience offered by cloud-based services.”

“Such experience relies on the end-to-end QoS, and more generally on respective SLAs in place for a given service,” the document notes.

So there, once again, you have the inherent tension between “best effort only” access and “quality of service,” which in the 5G PPP document explicitly indicates that QoS mechanisms are necessary to ensure good end user experience.

There are, to be sure, many ways to enhance experience at the end user level. But “admission control” always has been a feature of public networks that must share key resources, and can become congested at peak hours of use.

Among other key 5G objectives is a mobile network with three orders of magnitude more capacity than was typical in 2010.

Another angle is that the 5G PPP envisions devices connecting with multiple networks over time, and possibly more than one network at any moment, meaning there will be more orchestration of access.

Whether that enhances, degrades or is neutral with respect to the “value” of networks, and how such orchestration affects the “commodity access” or “dumb pipe” position of access networks also is unclear.

Though 5G would not be the first next-generation mobile network to enable new apps, 5G arguably will be the first such network built with a specific category of applications in mind.

In some ways more dramatic, at least some observers predict 5G also will erase the distinction between “fixed” and “mobile” networks, with “capabilities and performances of mobile networks becoming similar to those of fixed networks in terms of capacity and services diversity,” argues the 5G “Public Private Partnership” a new European 5G initiative.

That might sound fanciful, were it not the case that small cells, carrier and other Wi-Fi resources, ideally, will allow devices to interwork seamlessly, erasing, from a user standpoint, the difference between “using a fixed network and using a mobile network.”

Essentially, all those techniques shift bandwidth demand from “mobile” to “fixed” access.

The other change is the deliberate architecting of network standards to support both machine-to-machine apps (Internet of Things) and person-to-person communications.

5G will be about the Internet of Things, argues Neelie Kroes, European Commission VP. If that prediction turns out to be correct, 5G will be the first next-generation mobile network defined by applications, not just air interfaces and bandwidth.

“It will also offer totally new possibilities to connect people, and also things, being cars,

houses, energy infrastructures,” Kroes argues. “All of them at once, wherever you and they are."

One might argue those sorts of comments also are part of a political agenda. Perhaps oddly, the mobile infrastructure business now is lead by European and Chinese firms. So initiatives related to 5G arguably are part of an effort to keep Europe at the forefront of mobile infrastructure businesses in the future.

On the other hand, initiatives such as the 5G “Public Private Partnership” also speaks to a fear that Europe fell behind in 4G device and application innovation and leadership.

And, as always, the positive impact on economic growth and jobs are part of the rationale for pushing ahead in 5G.

The document also notes why mobile data is at the heart of the proposed 5G architecture.

Within Europe, “revenue from mobile data services compensates for the declines in total spending for both the fixed and mobile voice services markets,” the group says.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

Maybe an AI Bubble Exists for Training, Not Inference

Not all compute is the same, where it comes to artificial intelligence models , argues entrepreneur Dion Lim , especially where it comes to...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...